System Fragmentation: Europe, Eurasia, and the Future of Global Value Chains

This article is part of the “European Sovereignty & System Constraint Series” series examining how layered pressures reshape sovereignty and strategic autonomy.

The global economy is no longer organised primarily around efficiency. It is reorganising around security, resilience, and control. This shift is neither temporary nor cyclical. It reflects a deeper transformation in how power is exercised in the international system — away from integrated globalisation and toward fragmented, securitised architectures composed of interlocking systems.

Eurasia is the central geography of this transition.

While debates often focus on tariffs, industrial policy, or trade agreements in isolation, the more consequential change is structural. Energy systems, financial infrastructure, logistics corridors, industrial capacity, and security architectures are increasingly layered into strategic stacks. Control over these stacks — and position within them — now matters more than participation in any single market.

Europe’s strategic dilemma must be understood within this context.

From globalisation to system competition

For three decades, global value chains were optimised for cost minimisation, scale, and speed. Production was distributed globally, capital moved freely, and geopolitical risk was treated as an externality. That model is breaking down.

Today, supply chains are being shortened, duplicated, and politically conditioned. Strategic sectors — energy, semiconductors, defence, critical minerals, digital infrastructure — are no longer governed primarily by price signals, but by security considerations. Interdependence, once seen as stabilising, is increasingly treated as vulnerability.

This is not deglobalisation. It is system competition.

The world is reorganising into overlapping but partially incompatible economic and technological systems, anchored by the United States and China. Global value chains are fragmenting accordingly.

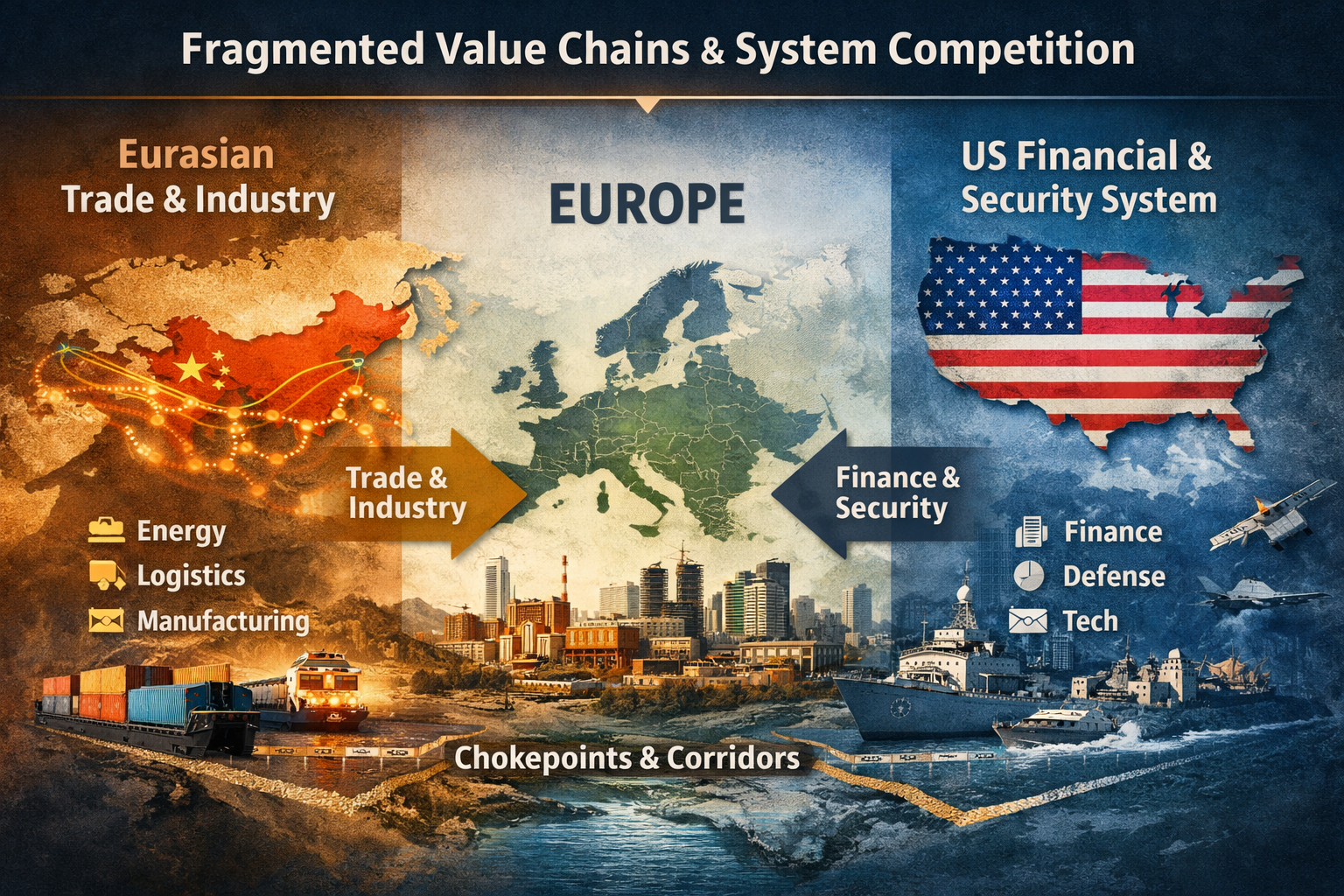

Eurasia as the organising geography

Eurasia is not a neutral backdrop to this transformation. It is the landmass through which the majority of global trade, energy flows, industrial capacity, and population are concentrated — and where competing system architectures intersect.

China’s long-term strategy has been to embed itself at the centre of Eurasian production, logistics, and infrastructure. Through trade, manufacturing scale, industrial policy, and connectivity corridors, it has sought to reduce exposure to maritime chokepoints while deepening continental integration.

The United States, by contrast, remains structurally oriented toward maritime dominance, financial primacy, and alliance-based security architectures. Its leverage is strongest in the upper layers of the global stack: finance, technology standards, defence systems, and security guarantees.

Europe sits between these systems — geographically, economically, and strategically.

Stacks, not sectors: the new architecture of power

Understanding Europe’s position requires moving beyond sector-by-sector analysis. Power today is exercised through stacked systems, where dominance in one layer reinforces leverage in others.

At a minimum, these stacks include:

- Energy (supply, pricing, transport, and volatility transmission)

- Finance (currency, capital markets, payment systems, sanctions)

- Security (defence platforms, alliances, ISR, command architectures)

- Logistics and corridors (ports, rail, shipping lanes, chokepoints)

- Industry and technology (manufacturing scale, standards, supply chains)

Control over interfaces between these layers increasingly substitutes for multilateral governance. Rules give way to leverage; institutions to bargaining power.

Europe is exposed across all five layers.

Fragmented GVCs and Europe’s structural constraint

Europe’s economic model depends on:

- imported energy,

- access to external markets,

- stable trade corridors,

- and predictable regulatory environments.

As global value chains fragment, these dependencies become constraints.

Europe remains deeply embedded in US-centred financial, technological, and security systems. At the same time, its trade, industrial inputs, and growth prospects are increasingly tied to Eurasian connectivity — including Asia, the Middle East, and the corridors linking them.

This is not a question of political alignment. It is a question of system position.

Fragmentation increases the strategic importance of corridors and chokepoints. Rail links, ports, maritime routes, and energy transit infrastructure regain geopolitical significance. Disruption risk becomes a form of leverage, and resilience replaces efficiency as the organising principle of trade.

For Europe, diversification alone is insufficient. Diversification without energy security, industrial depth, and corridor resilience merely redistributes vulnerability.

Industrial capacity and the limits of autonomy

Debates about European strategic autonomy often assume that regulatory power, fiscal capacity, or trade policy can compensate for structural exposure. In a fragmented GVC environment, this assumption no longer holds.

Industrial capacity becomes decisive.

Energy-intensive sectors — chemicals, metals, fertilisers, cement, glass — are already under pressure. Increasingly, so are industries framed as strategic: batteries, EV supply chains, semiconductors, data centres, and defence manufacturing. These sectors cannot scale or remain competitive under persistent energy volatility and corridor insecurity.

Without industrial depth, autonomy in defence, technology, or trade becomes illusory. Rearmament without a resilient industrial and energy base risks entrenching dependence rather than overcoming it.

Multilateralism and the geography of leverage

The fragmentation of global value chains also reveals the limits of contemporary multilateralism. Institutions designed for an integrated global economy struggle to function in a world organised around stacked systems and regional leverage.

As Eurasian connectivity deepens and system competition hardens, governance increasingly follows power rather than rules. Control over energy flows, logistics corridors, financial infrastructure, and security guarantees narrows the space for genuinely multilateral solutions.

Europe is particularly exposed to this shift. Its prosperity and stability were built in a rules-based, integrated system that is no longer the dominant organising principle of global order.

Europe’s strategic choice

Europe still has agency, but it is constrained. The window for shaping its position within the emerging Eurasian architecture is narrowing.

Strategic autonomy in this environment is not declarative. It is material. It depends on:

- secure and affordable energy,

- industrial capacity at scale,

- defence credibility rooted in production, not procurement,

- and resilient access to Eurasian trade corridors.

Absent these foundations, Europe risks becoming a rule-taker in a system increasingly shaped by others.

This article forms part of a broader research effort examining the global paradigm shift now underway — from integrated globalisation to fragmented, securitised systems. Together with earlier work on energy, leverage, and the Gulf, it points to a clear conclusion: European sovereignty is constrained not only by policy choices, but by system geography and position within the emerging architecture of global power.

Understanding Eurasia as the central arena of this transformation is not optional. It is the starting point for any serious European strategy in a G2 world.

Further Reading

Corridors, Chokepoints, and the Geography of Leverage Global

Finance, Sanctions, and the Upper Layers of System Control Global

External Limits of European Sovereignty (EU Challenge)

Suggested Reading

System Foundations of the Energy–AI–Industrial Economy On why energy, industry, compute, and finance now operate as a single system.

Energy Sovereignty as System Control Global / Doctrines)

On why control over energy systems underpins all downstream sovereignty.Global Value Chains in an Energy-Bound World(Global / Energy)

On how energy costs and infrastructure shape production geography.Europe’s Energy Paradigm Shift(EU Sovereignty)

On Europe’s specific exposure to energy cost and infrastructure constraint. ### Energy as Power ArchitectureEnergy as the Operating System of Power The foundational thesis: energy as the organising substrate of modern economic and geopolitical power.

AI Energy Stress Test (Eu Sovereignty) ### Foundational Context

Energy and the Base Layer of Constraint*(Systems under Constraint) Why energy re-emerged as the first binding constraint in the electrified economy.

Asymmetry Under Stress How constraint reveals differences in resilience, coordination capacity, and shock absorption. ### Transmission and Dependence

Decarbonisation as a Tech War Instrument (Tech War / Dynamics)

Downstream Implications

II. TECHWAR — Stack Fractures Under Constraint

These pieces show how energy constraint propagates upward into technology stacks and compute concentration.

Stack-Level Fractures in the Tech War How system dependencies fracture under pressure — and why energy stress cascades across layers.

Compute Locality in an Energy-Bound AI System Why AI infrastructure gravitates toward power stability and low marginal electricity cost.

III. EU SOVEREIGNTY — Constraint as Political Condition

These essays apply the Energy-Bound framework specifically to Europe’s structural position.

Energy as Europe’s Strategic Constraint Why energy marginal cost structure now defines Europe’s competitive ceiling.

Energy Sovereignty as System Control (EU) From fuel ownership to integration control: sovereignty as system design.

Europe’s Microprocessor and Energy Dependency Trap How compute dependency and energy cost structure interact as a failure mode.

Beyond Ideology — Foundational Doctrine

How Europe’s Political Lens Obscures Structural Realities in a Multipolar World

Sequencing, Deregulation, and the Political Economy of Exposure

IV. Boundaries — Social and Temporal Limits

Energy constraint is not only technical or geopolitical. It is social and institutional.

**The Legitimacy Boundary— Labour Markets and the Social Limits of Strategic Autonomy**

Democratic durability under transition stress.Legitimacy, Labour, and System Durability — Reference Index Consolidated essays on consent, affordability, and social absorption capacity.

EU Decisive Decade Time as constraint: irreversibility and strategic narrowing windows.

V. Doctrinal Extensions

These doctrine cards operationalise the Energy-Bound condition into actionable architectural principles.

- Mediterranean Decentralised Energy Doctrine Why fragmented geography and climate stress make decentralised electrification structurally optimal.