Financial–Physical Asymmetry in an Energy-Bound System

Why Value, Capital, AI Infrastructure, and Strategic Minerals Diverge Under Constraint

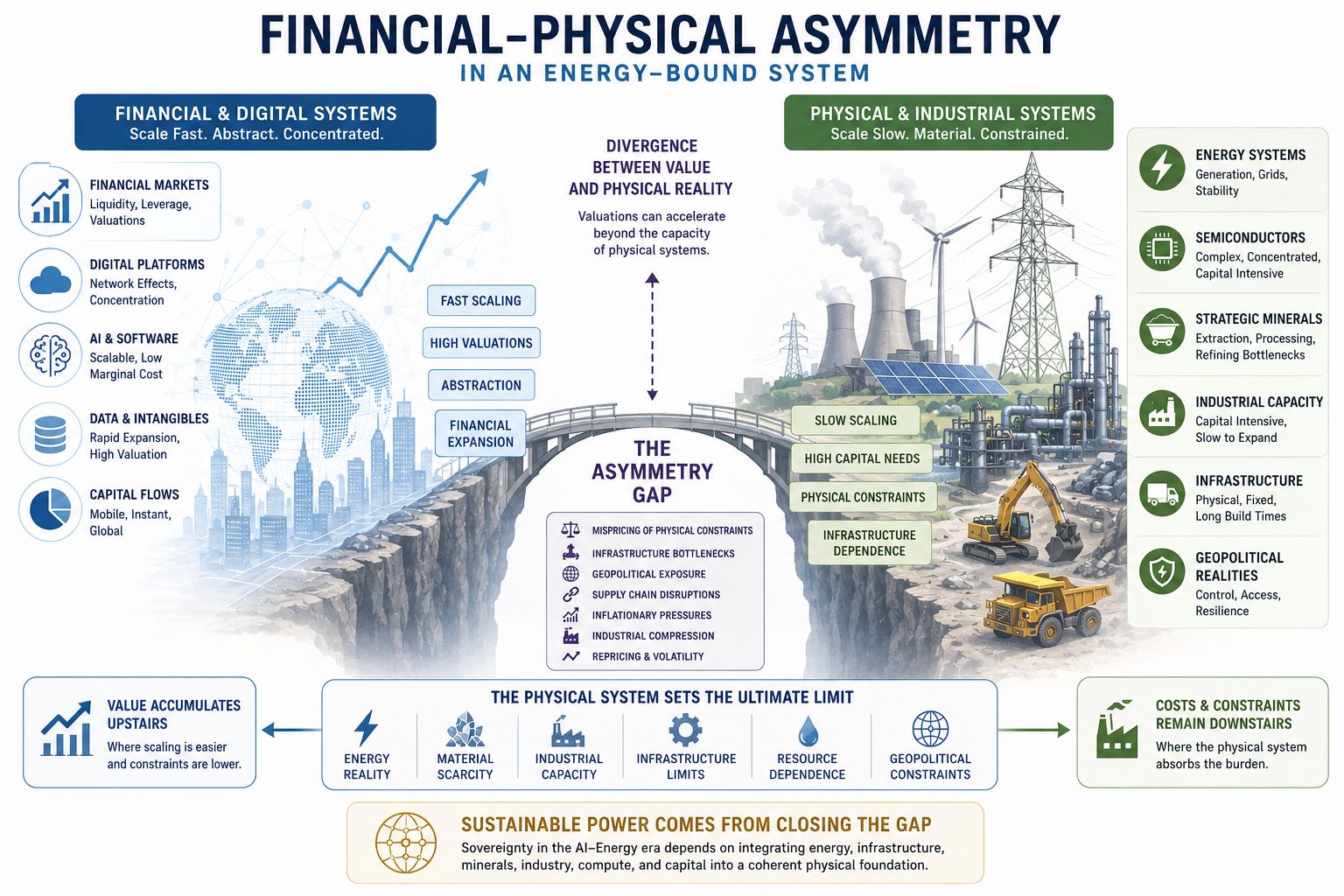

Doctrine Statement

Modern financial and digital systems increasingly create the impression that economic expansion can detach itself from physical reality.

Digital systems scale rapidly.

Financial systems expand through liquidity creation, leverage, valuation

expansion, and increasingly abstract forms of capital

coordination.

Artificial intelligence intensifies this perception because software

outputs can appear to scale at near-zero marginal cost.

Yet the underlying physical system does not disappear.

Energy systems, electrical grids, semiconductors, cooling systems, industrial supply chains, strategic mineral ecosystems, and infrastructure networks continue to determine the material limits of computational expansion.

This produces a growing structural asymmetry.

Financial, digital, and intangible layers can scale faster than physical systems because they require lower direct material input per unit of apparent value creation.

Physical systems remain constrained by:

energy availability,

infrastructure buildout,

industrial capacity,

geography,

material extraction,

mineral processing,

and transmission systems.

As a result:

value increasingly accumulates within financial, digital, and platform layers, while cost, constraint, extraction burden, and infrastructural dependency remain concentrated within the physical layer.

This divergence can persist for extended periods.

It does not eliminate the physical constraint.

It postpones recognition of the constraint while allowing valuation expansion to continue beyond underlying infrastructural capacity.

The Structural Mechanism of Asymmetry

The asymmetry emerges because financial and digital systems scale according to fundamentally different dynamics than physical and industrial systems.

Financial and Digital Scaling

Financial and digital systems benefit from:

low marginal replication cost,

rapid scalability,

high liquidity absorption,

platform effects,

network concentration,

and valuation expansion that can become partially detached from physical production cost.

Under these conditions, capital naturally gravitates toward sectors capable of generating faster apparent returns with lower immediate infrastructural friction.

This favours:

financial systems,

digital platforms,

software ecosystems,

and AI-enabled computational layers.

Physical and Industrial Scaling

Physical systems operate differently.

Energy infrastructure, industrial production, grids, semiconductor fabrication, strategic mineral ecosystems, logistics systems, and transportation networks require:

large fixed capital expenditure,

long construction timelines,

material extraction,

refining capacity,

industrial coordination,

physical maintenance,

and continuous energy input.

These systems cannot scale at the same velocity as financial abstractions or software-based valuation systems.

Physical infrastructure therefore absorbs:

capital intensity,

commodity volatility,

energy price exposure,

geopolitical risk,

industrial dependency,

and infrastructure bottlenecks.

The Resulting Divergence

The result is a structural divergence between:

where value is priced and accumulated,

andwhere physical capacity must actually be built.

Capital increasingly concentrates inside scalable financial and digital systems.

Meanwhile, physical systems continue carrying the burden of:

production,

infrastructure expansion,

energy transmission,

industrial maintenance,

mineral processing,

semiconductor fabrication,

and material constraint resolution.

This divergence creates the appearance that economic expansion can continue independently from physical limitation.

In reality, the physical system remains the foundation upon which all higher-order financial and computational systems ultimately depend.

AI and the Return of Physical Constraint

Earlier phases of digitalisation appeared to weaken the relationship between economic scaling and physical infrastructure.

Software platforms could expand globally with relatively limited additional physical input.

Artificial intelligence increasingly alters this assumption.

Although AI outputs may appear digitally scalable, advanced computational systems are becoming progressively more dependent upon physical infrastructure constraints.

Large-scale AI systems increasingly require:

vast electrical capacity,

grid continuity,

semiconductor concentration,

cooling infrastructure,

data centre construction,

water availability,

transmission systems,

industrial-scale capital deployment,

and strategic mineral ecosystems.

Under these conditions, computational scaling increasingly becomes an infrastructure question rather than purely a software question.

This marks a major structural transition.

AI has not eliminated physical constraint.

AI increasingly exposes the physical foundations upon which digital systems depend.

As AI systems scale, the apparent distinction between digital and physical systems progressively weakens.

The strategic issue therefore shifts from software ownership alone toward control over:

energy systems,

compute infrastructure,

semiconductor ecosystems,

electrical stability,

strategic minerals,

industrial capacity,

refining systems,

and infrastructure geography.

Strategic Minerals and the Return of Industrial Sovereignty

The rapid expansion of AI infrastructure increasingly reconnects computational scaling to the underlying mineral architectures upon which advanced industrial systems depend.

Rare earth elements and strategic minerals can no longer be evaluated primarily through conventional commodity logic.

Under earlier industrial and financial frameworks, minerals were typically evaluated according to:

extraction cost,

cyclical commodity pricing,

short-term supply-demand dynamics,

and conventional mining profitability models.

Under AI-energy conditions, this framework becomes increasingly incomplete.

Strategic minerals increasingly function as:

foundational infrastructure inputs into computational civilisation itself.

Semiconductors, electrification systems, batteries, robotics, defence electronics, transmission systems, renewable infrastructure, and hyperscale compute architectures all depend upon increasingly concentrated mineral ecosystems.

The strategic issue therefore no longer concerns extraction alone.

It increasingly concerns:

refining dominance,

processing ecosystems,

industrial clustering,

manufacturing integration,

logistical resilience,

and downstream technological control.

Under these conditions, rare earth elements and strategic minerals increasingly behave less like conventional commodities and more like:

infrastructural chokepoints,

industrial leverage systems,

sovereignty assets,

and geopolitical control layers.

This creates another dimension of financial–physical asymmetry.

Financial markets often continue valuing these sectors through relatively narrow commodity frameworks while underestimating their systemic role inside the emerging AI-energy architecture.

As a result:

markets may increasingly undervalue physical constraint resolution during periods dominated by financial abstraction and digital valuation expansion.

Financial Expansion Under Physical Constraint

The return of physical infrastructure dependence does not eliminate financial asymmetry.

It restructures the asymmetry around infrastructure access.

Financial markets may continue valuing AI and digital systems according to assumptions inherited from the software era:

near-frictionless scalability,

rapid margin expansion,

low marginal replication cost,

and continuing platform concentration.

However, the underlying computational layer increasingly resembles industrial infrastructure rather than purely digital software.

This creates growing tension between:

financial valuation models,

andphysical infrastructure realities.

As computational systems become increasingly energy-intensive and infrastructure-dependent, financial markets may continue pricing future expansion faster than physical systems can realistically scale.

This divergence can persist for considerable periods.

However, over time, physical bottlenecks increasingly reassert themselves through:

electrical shortages,

infrastructure congestion,

semiconductor constraints,

mineral concentration,

refining bottlenecks,

energy price pressure,

geopolitical competition,

and rising capital intensity.

Global Expression — Core and Periphery

This asymmetry has long existed at the global level.

Historically, developing economies often carried the burden of physical production while higher-value financial and technological systems remained concentrated elsewhere.

Under such conditions:

production occurred under energy and capital constraint,

value-added goods were priced externally,

industrial upgrading remained capital-constrained,

and currency weakness amplified import dependence.

This produced persistent asymmetry between:

physical production,

andfinancial value capture.

Value could be generated locally while pricing power and capital accumulation remained externally concentrated.

Currency systems reinforced the divergence by increasing the real cost of accessing advanced technological and industrial systems.

Internalisation Within Advanced Economies

What previously appeared primarily as a global North–South asymmetry is increasingly emerging inside advanced economies themselves.

Capital increasingly concentrates in:

digital platforms,

financial systems,

AI ecosystems,

hyperscale compute infrastructure,

and software-based coordination systems.

Meanwhile, physical systems increasingly absorb:

rising energy costs,

industrial compression,

infrastructure expenditure,

mineral dependency,

grid expansion requirements,

and slower capital returns.

This produces widening internal asymmetry between:

sectors capable of rapid financial scaling,

andsectors responsible for sustaining physical continuity.

European Expression — Structural Compression Under AI-Energy Conditions

Europe is particularly exposed to this emerging asymmetry.

The European system combines:

relatively high marginal energy costs,

limited domestic energy abundance,

industrial dependence upon imported energy,

strategic mineral dependency,

strong manufacturing exposure,

fragmented capital markets,

and incomplete technological sovereignty across key computational layers.

At the same time, European capital increasingly follows valuation structures shaped by the American technology and hyperscaler model.

This creates structural tension.

The United States benefits simultaneously from:

large-scale energy production,

hyperscale platform concentration,

semiconductor leverage,

deep capital markets,

and global financial centrality.

China increasingly benefits from:

strategic mineral processing dominance,

industrial ecosystem integration,

refining concentration,

manufacturing scale,

and long-duration industrial coordination.

Europe does not possess equivalent structural advantages across the full stack.

As AI increasingly becomes physical infrastructure, this divergence becomes more strategically significant.

Europe therefore risks financing externally dominant computational systems while remaining dependent upon external infrastructure architectures, semiconductor ecosystems, and strategic mineral supply chains.

This is not merely a technological gap.

It is an emerging sovereignty gap.

The strategic challenge increasingly concerns whether Europe can successfully convert:

energy systems,

infrastructure,

industrial capacity,

strategic geography,

and regional manufacturing capability

into sovereign computational and industrial power.

This broader conversion problem increasingly defines the European strategic position under AI-energy conditions.

Interaction with the Physical Constraint

Financial and digital systems can expand faster than physical systems for extended periods.

Valuations may rise rapidly.

Capital may concentrate aggressively.

Expectations may accelerate beyond physical buildout capacity.

However:

the physical system ultimately determines the ceiling of sustainable expansion.

No financial architecture can permanently remove:

energy requirements,

industrial constraints,

infrastructure dependence,

mineral concentration,

refining bottlenecks,

material scarcity,

or geopolitical exposure.

When divergence between valuation and physical capacity becomes too extreme, adjustment increasingly occurs through:

repricing of assets,

capital reallocation,

infrastructure bottlenecks,

inflationary pressure,

industrial compression,

supply chain disruption,

or geopolitical stress.

Interaction with the Monetary System

Energy asymmetry increasingly feeds directly into monetary asymmetry.

Systems facing structurally higher energy costs increasingly experience:

industrial margin pressure,

external dependence,

current account stress,

capital flow asymmetry,

strategic import dependence,

and currency vulnerability.

Over time, this contributes to:

a monetary ceiling for systems unable to resolve their underlying physical, industrial, and energy constraints.

Financial systems can postpone recognition of the problem.

They cannot permanently eliminate it.

Investor Implication

For investors, financial–physical asymmetry creates both opportunity and systemic risk.

Digital and AI systems may continue generating powerful valuation expansion because scalable computational systems continue attracting global capital concentration.

However, rising computational intensity increasingly reconnects valuation to physical infrastructure availability.

The central distinction therefore becomes:

whether capital is merely capturing scalable valuation — or whether it is building durable physical capacity.

This increasingly includes:

energy systems,

compute infrastructure,

semiconductor ecosystems,

strategic minerals,

refining systems,

industrial manufacturing,

and logistics resilience.

Systems that successfully integrate these layers are more likely to sustain long-duration strategic advantage.

Systems that remain financially exposed while infrastructure-constrained may increasingly face:

valuation instability,

dependency risk,

industrial erosion,

and structural compression.

Strategic Implication

Long-term system stability depends increasingly upon reducing the divergence between:

financial expansion,

andphysical capacity formation.

Durable sovereignty increasingly depends upon the successful integration of:

energy systems,

industrial infrastructure,

strategic minerals,

computational capacity,

manufacturing ecosystems,

capital formation,

and strategic geography.

Under AI-energy conditions, sovereignty increasingly becomes infrastructural.

The systems most likely to maintain durable power are not necessarily those generating the highest short-term valuations.

They are the systems most capable of resolving physical constraints while sustaining computational, industrial, mineral, and infrastructural scaling simultaneously.

One-Line Summary

Capital scales where constraint is lowest — but durable power resides where physical constraint is successfully resolved.