Monetary Power

Energy, industry, infrastructure, geopolitics

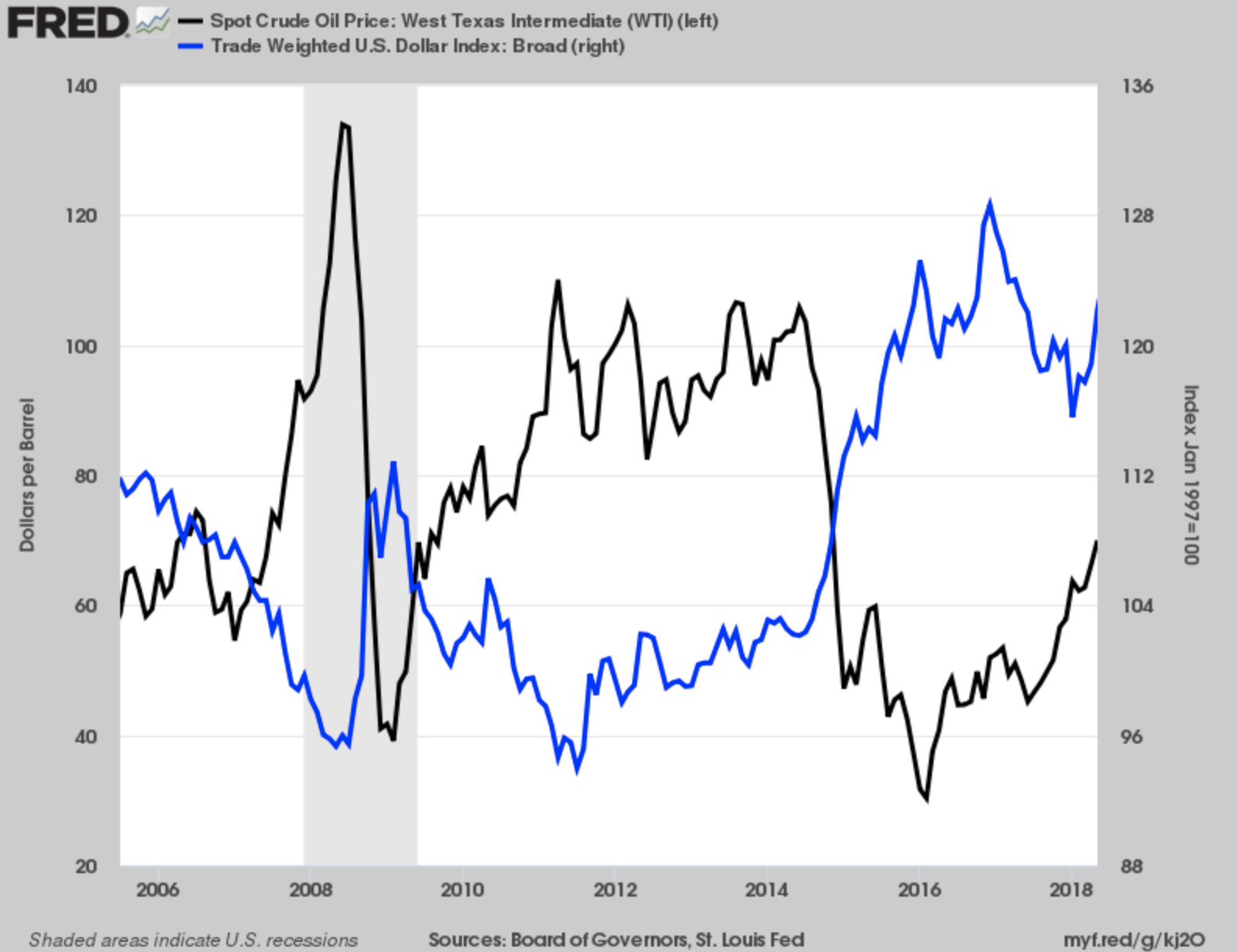

Source: EIA as of 12/31/2024

The effectiveness of monetary leverage is conditioned by control over energy and technology, which form the material foundations of financial power.

Keynote

Monetary power is no longer exercised primarily through institutions, rules, or credibility alone. In an Energy-Bound System, it rests on the ability to absorb energy-price shocks, stabilise industrial input costs, and finance infrastructure at scale without external dependence.

Currency strength, liquidity access, and financial leverage increasingly reflect:

energy depth and pricing architecture (imported marginal pricing vs domestically anchored cost floors),

industrial resilience (capacity to convert capital into output under stress),

and system coordination (infrastructure duration, permitting capacity, grid buildout, supply-chain continuity).

This article explains how monetary power has become a derivative of physical capacity—and why states that lack energy, industrial, and infrastructure foundations find their monetary tools narrowing, not expanding.

Executive Summary

Monetary power remains one of the primary instruments through which the United States structures the global order. The central role of the dollar in trade, finance, and reserves grants the U.S. exceptional leverage—allowing it to absorb global shocks, externalise adjustment costs, and project financial constraints far beyond its borders.

But this dominance is increasingly coupled to material foundations:

the U.S. role as a major oil and gas producer/exporter,

the growing dependence of global liquidity on U.S. financial inflows,

and the extension of dollar usage into digital rails via dollar-denominated stablecoins.

This article argues that monetary power detached from productive capacity and system legitimacy becomes self-limiting. The system is not moving toward symmetry, but toward a more brittle hierarchy—where monetary leverage hardens into strategy, alternatives proliferate, and volatility increases.

Ultimately, monetary leverage is conditioned by control over energy systems and technology infrastructure, which form the material foundations of financial power.

I. Monetary Power as Systemic Leverage

The international monetary system is not neutral infrastructure. It is a hierarchy structured around access to liquidity, settlement systems, and reserve assets. At its core sits the U.S. dollar, functioning simultaneously as unit of account, medium of exchange, and store of value for global trade and finance.

This position grants the United States extraordinary advantages. Dollar demand allows the U.S. to finance persistent deficits at low cost, absorb global savings, and shift adjustment burdens outward during periods of stress. In moments of crisis, capital flows toward U.S. assets rather than away from them, reinforcing dollar centrality even when shocks originate within the U.S. economy itself.

Monetary power therefore operates less through overt control than through structured dependency. States, firms, and financial institutions organise behaviour around dollar liquidity because alternatives are costly, fragmented, or politically constrained. This asymmetry is not accidental; it is the defining feature of the system.

The foundation of U.S. monetary power lies in the dollar’s role as the dominant reserve currency—a position that has weakened gradually over time but remains structurally intact.

U.S. Dollar Share of Global Foreign Exchange Reserves

The dollar’s share of global reserves has declined from its post-Bretton Woods peak, reaching a multi-decade low, yet it remains the dominant reserve currency by a wide margin. This gradual erosion reflects diversification at the margins rather than a wholesale displacement of the dollar’s central role in global finance.

Source: IMF COFER data; Bloomberg.

This decline should not be interpreted as a loss of monetary primacy, but as evidence of slow and uneven diversification. No alternative currency currently combines the liquidity, market depth, legal certainty, and institutional backing required to function as a global reserve at scale.

Because the dollar remains dominant despite gradual erosion, adjustment pressures are displaced outward—onto deficit countries, commodity exporters, and emerging markets operating within a dollar-centric system.

Dollar dominance is sustained not only by reserve holdings, but by persistent capital inflows that finance U.S. external deficits across market cycles. The composition of these inflows matters: portfolio and other financial flows dominate, while net foreign direct investment is comparatively limited. This reflects a system in which surplus-economy savings are recycled into U.S. financial markets, reinforcing dollar liquidity while deepening financialisation.

For surplus and developing economies, this arrangement translates into constrained domestic investment, exposure to dollar cycles, and limited monetary autonomy. As a result, U.S. monetary tightening propagates globally through capital flows and exchange rates—transmitting volatility to economies least able to absorb it.

II. Monetary Dominance and Industrial Fragility

Monetary dominance is not sustained by reserve status alone. It is sustained by the capacity of U.S. financial markets to absorb global savings across cycles.

But dollar dominance carries structural trade-offs. Persistent capital inflows and reserve demand can contribute to chronic currency overvaluation, weakening export competitiveness and encouraging financial returns over productive investment. Monetary strength can mask industrial erosion.

This tension is not new. Historical reserve currencies—from sterling to the post-war dollar—faced similar contradictions between financial centrality and industrial vitality. What distinguishes the current era is the scale of global capital mobility and the speed at which financial signals transmit into real-economy constraints.

For the United States, monetary power has increasingly substituted for industrial competitiveness rather than reinforcing it. High returns in financial markets can pull capital away from long-cycle investment in infrastructure, manufacturing, grid capacity, and energy systems. The result is a paradox: the currency appears strong, while the productive base becomes more brittle.

Cumulative Net Capital Inflows into the United States by Balance of Payments Category

Persistent net capital inflows—dominated by portfolio debt and other financial flows—have financed large and sustained U.S. current account deficits over multiple decades. This structure underpins U.S. monetary power by allowing external adjustment costs to be absorbed by surplus economies rather than domestically.

The IMF’s recent work on dominant-currency pricing and export windfalls reinforces a key structural point: exchange rates are not neutral adjustment tools, and “flexibility” often transmits power asymmetrically through pricing, profitability, and savings capture.

Composition of Global Foreign Exchange Reserves by Currency: Despite gradual diversification, the US dollar continues to dominate global foreign exchange reserves in absolute terms. Other currencies—including the euro and the renminbi—remain secondary, limited by insufficient market depth, capital controls, and institutional fragmentation. The result is diversification without substitution. Source: IMF COFER data.

III. Energy, Commodities, and the Re-Materialisation of Monetary Power

In an Energy-Bound System, monetary power becomes more tightly coupled to energy pricing architecture and commodity cycles.

As the United States becomes a major exporter of oil and gas, dollar dynamics are increasingly entangled with:

energy export revenues,

commodity-cycle volatility,

and the geopolitics of chokepoints, sanctions, and corridor stability.

Energy exports can support external balances and reinforce strategic leverage over importers. But commodity-linked monetary power is structurally volatile: high prices strengthen leverage but compress demand; low prices reverse the effect. For a reserve-currency issuer, volatility is transmitted outward rather than absorbed domestically—amplifying instability across emerging and developing economies.

The result is a system in which monetary power increasingly rests on energy exports and financial inflows rather than industrial depth. This does not eliminate U.S. dominance, but it narrows the margin for error.

This coupling is consistent with the argument developed in Energy Leverage and in Energy as the Operating System of Power, energy is no longer a background input; it is a macroeconomic transmission channel.

IV. Monetary Transmission Under Constraint

(Energy → CPI → Fiscal → Currency)

In energy-importing systems operating on externally set marginal pricing (including LNG and global benchmark-linked contracts), energy becomes a first-order macroeconomic variable. That constraint transmits as a chain:

Energy cost shock

→ CPI persistence (direct energy bills + producer costs

+ expectations)

→ fiscal absorption (subsidies, compensation, emergency

stabilisers, higher debt service)

→ currency pressure (capital repricing of material

exposure, growth expectations, external valuation).

This mechanism formalises why monetary sovereignty is increasingly downstream of energy sovereignty and infrastructure duration.

(See your companion doctrine piece: Monetary Sovereignty in an Energy-Bound System.

V. Stablecoins and the Digital Extension of Dollar Power

Digital dollar rails introduce a new layer of monetary power.

Dollar-denominated stablecoins function as private extensions of dollar liquidity, operating outside traditional banking systems while remaining anchored—directly or indirectly—to U.S. monetary conditions. For users in emerging economies, they offer speed, accessibility, and protection against local currency instability. For the United States, they extend dollar usage without expanding formal institutional obligations.

Yet this extension intensifies asymmetry:

Stablecoins accelerate de facto dollarisation while eroding domestic monetary control in weaker economies.

They can bypass regulatory frameworks and weaken capital controls.

They transmit U.S. tightening and dollar strength directly into fragile financial systems.

In system terms, stablecoins are not merely a fintech innovation. They are an upper-layer settlement expansion that deepens dependency while increasing the political incentive to seek alternatives.

The asymmetry of dollar dominance becomes most visible in the uneven distribution of dollar-denominated debt exposure:

Dollar-Denominated Public Debt in Selected Asian Economies

Dollar exposure in public debt varies sharply across Asia, reflecting structural dependence rather than uniform dollarisation. While aggregate exposure has declined over time, several economies remain highly sensitive to dollar cycles, exchange-rate movements, and U.S. monetary policy—illustrating how reserve-currency power transmits uneven financial risk across the global system.

Source: Federal Reserve Bank of St. Louis (FRED).

VI. The Global South and Structural Asymmetry

For much of the Global South, the dollar-centred system imposes structural constraints rather than opportunities. Trade invoicing, debt servicing, and capital access remain overwhelmingly dollar-denominated, pushing countries to accumulate reserves, suppress domestic demand, and remain exposed to external shocks.

Commodity exporters are particularly vulnerable. Dollar appreciation raises debt burdens, depresses local currencies, and amplifies boom–bust cycles. Industrial upgrading becomes difficult when financial volatility overwhelms planning horizons.

Stablecoins risk entrenching this hierarchy by extending dollar rails into informal and cross-border systems—shifting adjustment costs downward while preserving liquidity privileges at the centre.

VII. Fragmentation, BRICS, and Monetary Alternatives

Alternative arrangements are proliferating. These do not yet constitute a coherent replacement for dollar dominance, but they signal a gradual erosion of exclusivity.

Local-currency trade agreements, bilateral swap lines, commodity-linked settlement mechanisms, and regional financial institutions are expanding in parallel. BRICS economies, in particular, are experimenting with payment systems and reserve diversification strategies designed to reduce exposure rather than overturn the system outright.

This is not the emergence of a new hegemon. It is the slow fragmentation of a system whose legitimacy increasingly rests on coercion rather than consent.

BRICS Expansion and Structural Weight in the Global Economy

The expansion of BRICS increases the bloc’s share of global population, energy production, and output, strengthening its capacity to coordinate alternative trade and settlement arrangements. However, aggregate scale alone does not translate into monetary leadership, which continues to depend on liquidity, trust, and institutional depth.

Source: Visual Capitalist; IMF, World Population Review, EI Statistical Review, WTO.

Conclusion: Monetary Power Without Stability

Monetary power remains one of the United States’ most potent strategic assets. But its effectiveness increasingly depends on foundations that are under strain: industrial capacity, energy stability, infrastructure duration, and global legitimacy.

As monetary leverage hardens into strategy, it generates resistance, fragmentation, and volatility rather than stability. Digital extensions of the dollar may prolong dominance, but they do so by deepening asymmetry and accelerating systemic stress.

In the emerging G2 order, monetary power cannot substitute indefinitely for productive strength. Without a credible material base and cooperative architecture, financial dominance becomes brittle. The future global system is therefore unlikely to be orderly or balanced—but more contested, fragmented, and unstable, with monetary power exercised under increasingly constrained conditions.

The effectiveness of monetary leverage ultimately depends on control over energy systems and technological infrastructure—the material foundations of financial power.

Monetary leverage ultimately rests on material foundations—energy systems and technological infrastructure—examined in Energy Leverage and the TechWar section.

Sources & External References

The Economic Benefits of Unleashing American Energy.

Why US Energy Independence Won’t Mean Greater US Energy Autonomy.

The Future of the Northern Sea Route - A “Golden Waterway” or a Niche Trade route

Further Reading

To place this analysis within the wider system architecture, readers may wish to consult:

System Foundations

Energy-Bound System On constraint as the operating condition of 21st-century power.

Energy as the Operating System of Power On how energy systems structure monetary stability and crisis absorption capacity.

The Global Energy Paradigm Shift On how the end of fossil-fuel abundance re-materialises inflation and narrows monetary space.

Energy, Inflation, and Control

Energy Sovereignty as System Control (Global / Doctrines)

On why control over energy infrastructure conditions fiscal and monetary autonomy.Energy Leverage(Global Order Under Stress)

On chokepoints, pricing power, and how energy risk transmits into macro stability.

Monetary Constraint and Sovereignty

Monetary Sovereignty in an Energy-Bound System On energy → CPI → fiscal → currency transmission under structural constraint.

Monetary & Financial Sovereignty Under Constraint] (EU Sovereignty)

On how energy exposure and infrastructure gaps narrow Europe’s monetary space.Capital Duration as System Power (Tech War / Dynamics)

On why long-cycle capital determines who can sustain monetary authority.

- The New Monetary Cold War: Power - Digital Money, and Europe’s Vanishing Middle Ground

-Digital Infrastructure and Monetary Sovereignty - Digital Infrastructure and Monetary Sovereignty

Energy, Infrastructure, and the Struggle for System Control

Geopolitics and Upper-Layer Control

Finance, Sanctions, and Upper-Layer Control (Systems under Constraint)

On how monetary power is exercised through access, exclusion, and conditional liquidity.[Industrial Policy Inside Constrained Systems ](Systems under Constraint](../../_systems_under_constraint/6_Industrial_Policy_Inside_Constrained_Systems/eng.md)

On why monetary capacity ultimately depends on energy–industry alignment.

How to Read This Article

This article should be read as a structural analysis of monetary power, not a discussion of central-bank tactics. It explains why monetary authority today depends less on discretion and more on the material systems that support price stability, capital mobilisation, and crisis resilience.