Monetary Sovereignty in an Energy-Bound System

Currency, Capital, and Control Under Structural Constraint

Introductory framing paragraph

Recent analysis in Asymmetry Under Stress described how imbalance, leverage, and strategic exposure are now surfacing simultaneously across alliances, markets, and institutions. That paper focused on where pressure is appearing and how it is being felt politically and psychologically. The present analysis addresses a different question: why monetary and financial systems are now transmitting that pressure so rapidly and so unevenly.

The argument advanced here is that monetary instability is not an independent shock, nor primarily a failure of policy coordination. It is a downstream consequence of a deeper shift in material conditions — specifically, the transition to an energy-bound system in which currency credibility, capital stability, and policy autonomy are increasingly conditioned by physical capacity rather than institutional design alone.

This analysis treats monetary sovereignty as a system property rather than a regional condition, though its implications are particularly acute for energy-importing economies such as Europe.

Preface: Monetary power under material constraint

For much of the post–Cold War period, monetary sovereignty was treated as a function of institutional credibility, market depth, and financial architecture. Advanced economies assumed that energy supply would remain sufficiently abundant, elastic, and politically neutral for monetary policy to operate largely through demand management and confidence signalling.

That operating environment has changed.

This paper proceeds from the premise that monetary sovereignty is now structurally conditioned by energy and industrial systems. In an energy-bound world, currencies, capital flows, and balance sheets are increasingly exposed to physical constraints that do not adjust on financial or diplomatic timelines.

Inflation persistence, capital volatility, and unconventional monetary behaviour are therefore not anomalies, but rational system responses to tightening material limits.

In the current system, finance follows physics.

1. From monetary autonomy to monetary exposure

In conditions of abundance, monetary systems are buffered. Energy is cheap, supply chains are elastic, and inflation can be managed primarily through demand-side tools.

In an energy-bound system, that buffering disappears.

When energy becomes structurally constrained rather than episodically scarce, its price and availability transmit directly into:

inflation dynamics

trade balances

fiscal sustainability

political stability

For energy-importing economies operating on marginal LNG pricing rather than long-term pipeline stability, energy cost becomes structurally external. Risk premiums embedded in maritime chokepoints and global spot markets transmit directly into domestic price levels and policy space.

Monetary policy does not cease to function, but it loses primacy.

2. Energy as a monetary variable

Energy is not merely an input into production. It is a systemic price anchor.

In an electrified, industrially dense economy:

energy costs set the floor for industrial competitiveness

energy volatility feeds directly into core inflation

energy imports determine external balances

In an AI-intensive industrial environment, electricity demand accelerates precisely where digital scale expands. As digital intensity rises, monetary systems become more tightly coupled to energy infrastructure performance.

Where energy must be imported, priced externally, or financed in foreign currency, monetary exposure increases sharply.

As a result:

inflation becomes more persistent

policy trade-offs become harsher

credibility erodes faster under stress

Energy resilience becomes a prerequisite for monetary resilience.

3. Capital flight and the search for real anchors

Capital increasingly seeks:

hard assets

energy-linked infrastructure

industrial capacity

materially resilient jurisdictions

When energy volatility is structural:

long-dated financial assets become riskier

sovereign debt sustainability is questioned

currencies tied to fragile energy systems lose appeal

Where marginal energy costs remain structurally higher than peer economies, currency strength cannot be permanently sustained by institutional credibility alone.

Finance is repricing material exposure, not merely policy risk.

4. Energy Abundance, Digital Liquidity, and Hierarchy Reinforcement

Energy constraint does not produce symmetric outcomes.

Monetary sovereignty is reinforced where physical energy scale converges with capital depth.

The United States now combines:

large-scale domestic energy production

deep and liquid Treasury markets

reserve currency centrality

security primacy in key trade routes

expanding digital asset and crypto-denominated liquidity infrastructure

Under geopolitical stress, this configuration produces asymmetric monetary effects.

Higher energy prices do not automatically weaken the dollar. They can reinforce it.

Energy rents recycle into dollar assets.

Safe-haven flows increase demand for U.S. collateral.

Treasury markets absorb global risk reallocation.

If digital settlement rails remain dollar-adjacent — stablecoin-linked, Treasury-collateralised, or embedded within U.S. financial architecture — they extend dollar liquidity rather than displace it.

Energy scale supports monetary depth.

Monetary depth stabilises debt elasticity.

In a dominant reserve system, debt expansion can be absorbed through structural global demand for safe collateral. Liquidity depth allows refinancing and rollover to occur within a framework of continuous absorption capacity.

This creates monetary elasticity unavailable to energy-importing systems without comparable capital depth.

Debt growth in a dominant monetary system does not immediately undermine currency stability. Under stress, it can be stabilised by hierarchy.

For energy-importing monetary unions, the same shock produces the opposite dynamic:

Energy import cost increases

→ Industrial margin compression

→ Productivity divergence

→ Capital allocation preference shift

If global portfolios remain concentrated in dollar assets, capital preference compounds.

This is not crisis transmission.

It is hierarchy reinforcement.

5. Currency experimentation as system behaviour

Alternative settlement systems, digital currency initiatives, and bilateral trade arrangements should be understood as adaptation under constraint, not disorder.

As energy and industrial inputs become strategic variables:

states reduce external pricing exposure

firms shorten value chains

monetary systems fragment and layer

Monetary order becomes more tightly coupled to physical capacity.

Experiments in diversification are responses to structural asymmetry — not necessarily precursors to systemic collapse.

For a schematic overview of the macroeconomic propagation

mechanism,

see Energy

Shock Transmission Chain

6. Monetary sovereignty redefined

Monetary sovereignty can no longer be defined solely by:

central bank independence

reserve status

financial market depth

It must be understood as the capacity to absorb energy and industrial shocks without losing policy control.

A monetarily sovereign system can:

stabilise prices despite energy volatility

finance reindustrialisation domestically

sustain defence and social commitments under prolonged stress

retain investor confidence over duration

Monetary sovereignty expresses itself not in short-term exchange-rate performance, but in endurance under material constraint.

Monetary sovereignty is downstream of energy sovereignty.

![]() Transmission Chain of Monetary Pressure — Energy volatility propagates

through industrial margins, capital formation, and ultimately currency

resilience.

Transmission Chain of Monetary Pressure — Energy volatility propagates

through industrial margins, capital formation, and ultimately currency

resilience.

7. Europe’s exposure

Europe illustrates this dynamic clearly.

Despite credible monetary governance, Europe faces:

structurally high marginal energy costs

external energy pricing exposure

competitiveness pressure

Where energy marginal costs remain structurally higher than those of major peers, long-term currency stability becomes more difficult to anchor.

Persistent energy pricing differentials influence:

capital allocation

productivity expectations

growth trajectories

external valuation

If energy stress reinforces dollar liquidity while compressing European industrial margins, divergence compounds gradually.

This is not institutional weakness.

It is structural exposure within the transmission chain described below.

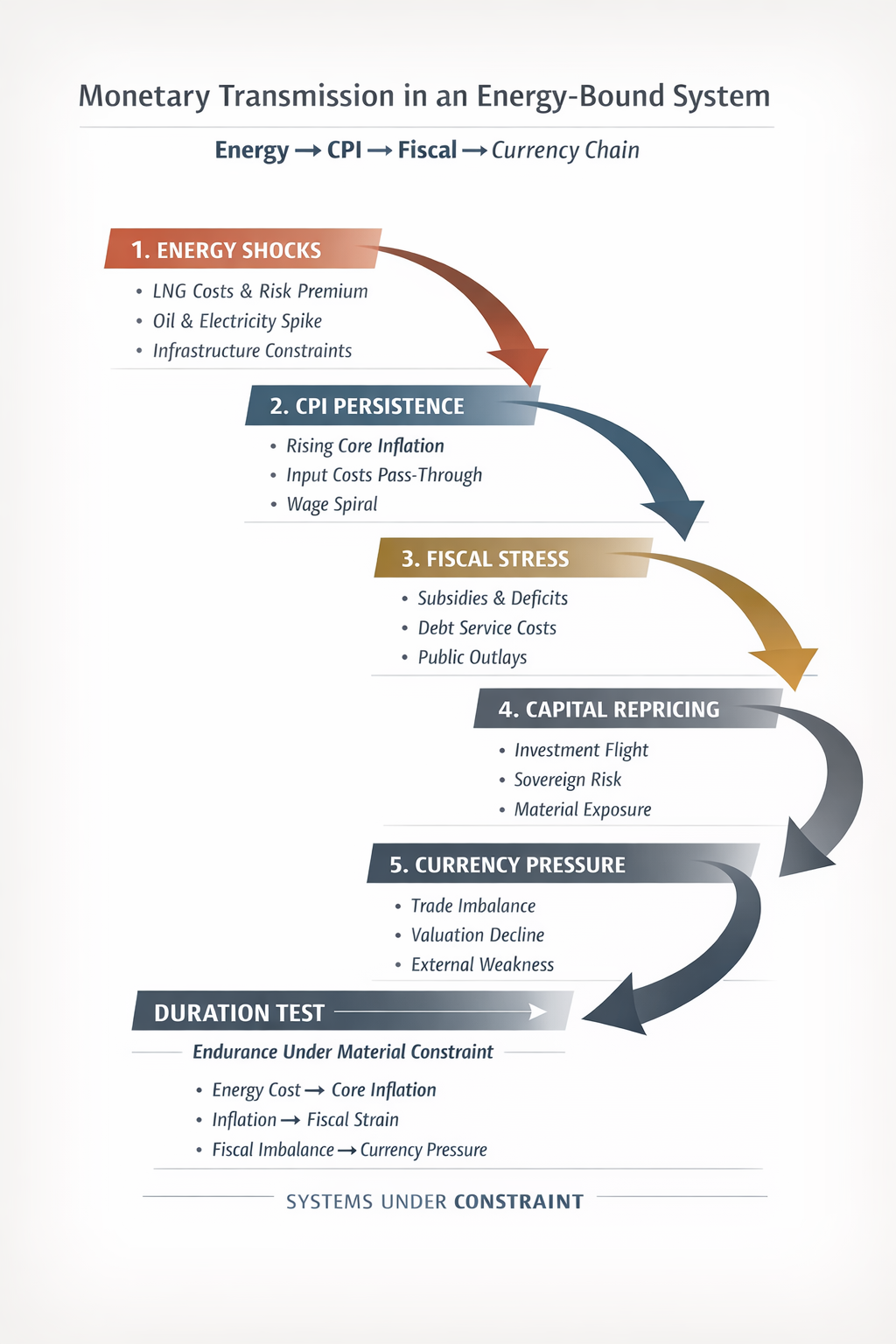

Monetary Transmission Chain

Energy → CPI → Fiscal → Capital → Currency

This formalises the propagation mechanism through which energy constraint transmits into monetary systems.

(Transmission chain sections remain unchanged — they already align perfectly with the above hierarchy reinforcement logic.)

Conclusion: Finance Follows Physics

Currencies do not float above material systems.

They transmit them.

In an energy-bound world:

energy policy is monetary precondition

industrial policy is fiscal stabilisation

infrastructure investment is currency defence

Monetary sovereignty is not disappearing.

It is being re-grounded in physical capacity.

Where energy scale aligns with capital depth and liquidity architecture, hierarchy reinforces itself.

Where energy exposure is structural and externalised, monetary space narrows gradually through allocation dynamics.

Energy precedes capital.

Capital precedes currency.

FURTHER READING

A system-level causal chain explaining how energy constraint propagates into inflation persistence, fiscal absorption, capital repricing, and euro valuation pressure.

POLICY BRIEF — Monetary Sovereignty in an Energy-Bound EuropePublic-facing condensed brief suitable for Brussels circulation.

Comparative diagnostic of EU vs US resilience in an Energy-Bound System (energy, capital markets, AI scaling, fiscal durability).

Energy-Bound System — defines the operating environment this article assumes

Energy-Bound SystemBeyond Ideology— why institutional frames break when constraints become binding

Beyond Ideology

Monetary stack coherence

Execution Under Compression— euro architecture, delay compounding, structural mismatch

(your Greek “Εκτέλεση υπό Συμπίεση” piece; keep the same local path you’re using in EU-SOV)Energy Constraint and the Monetary Ceiling — the ceiling logic this article feeds into

(your “energy_constraint_and_monetary_ceiling” node / panel anchor)Monetary Power — monetary leverage as derivative of physical capacity (energy/industry/infrastructure)

(your “Monetary Power” article in the monetary panel)Monetary Sovereignty and the New Monetary Cold War — upstream digital rails + payment/compute stack

(your “new monetary cold war” branch article)The relationship between energy systems, capital allocation, and currency hierarchy is illustrated in Greece: Energy–Capital–Currency Node and mapped globally in Global Energy–Capital–Currency System. ### Geopolitics + transmission

Chokepoints Under Compression — where risk premia enter the chain (shipping, LNG, maritime)

(your chokepoints essay in the systems/geopolitics layer)Asymmetry Under Stress — the “where pressure appears” diagnostic this piece extends

System Illustration

Historical arc / hierarchy logic

- Energy,

Financialisation, and Capital Hierarchy — Bretton Woods →

petrodollars → capital hierarchy → multipolar adjustment

(your “Energy, Financialisation, and Capital Hierarchy” essay)

Brief external reading list

1) Dominant-currency pricing and who captures windfalls

- IMF Working Paper (Jan 2026): exchange rates, export profitability, and national saving under dominant-currency pricing (useful for your “hierarchy reinforcement” logic).

2) Safe-asset hierarchy and “exorbitant privilege” mechanisms

NBER working paper: Exorbitant Privilege: a safe-asset view (formalizes flight-to-safety → stronger dollar dynamics).

Gourinchas & Rey: Exorbitant Privilege and Exorbitant Duty (classic framing of US external balance sheet advantage / return differential).

3) Energy shocks → inflation persistence in Europe

ECB Working Paper (2024): pass-through of gas price shocks to euro area inflation (directly supports the CPI layer of your transmission chain).

Euro-area energy price pass-through research note (2023): focuses on post-2021 energy shock transmission into headline/core components.

4) Digital rails, stablecoins, and whether they extend dollar liquidity

BIS Annual Report chapter (2025): stablecoins and the “next-generation monetary and financial system”(tests of singleness/elasticity/integrity; strong for your “rails extend hierarchy” claim).

IMF (Dec 2025): Understanding Stablecoins (IMF framing + BIS survey reference; good for policy-grade grounding).

FSB (Oct 2024): financial stability implications of tokenisation (bridges tokenised assets, settlement architecture, systemic risk).

5) Near-term stress validation (energy shock risk in 2026)

- Reuters / FT (Mar 3, 2026): ECB Chief Economist warning on Middle East conflict → euro-area inflation spike risk (supports your chokepoint-risk → CPI channel in real time).