Semiconductor Control and Compute Sovereignty

Why Compute Has Become Infrastructure Power

System Navigation

This article connects semiconductor sovereignty, AI infrastructure, energy systems, industrial ecosystems, digital sovereignty, ecosystem concentration, and geopolitical system architecture under AI–energy conditions.

It should be read together with:

I. The End of Abstract Compute

For several decades, much of the digital economy appeared increasingly detached from physical systems.

Software scaled globally across networked infrastructures. Financial markets rewarded platform expansion over industrial depth. Cloud architectures abstracted geography from everyday digital experience. Technological growth increasingly appeared capable of expanding independently from manufacturing concentration, energy systems, logistics infrastructure, and material extraction.

This period encouraged the belief that computation had become progressively weightless.

Digital systems appeared increasingly detached from the industrial foundations that had historically constrained economic power.

Artificial intelligence initially appeared to accelerate this perception further.

AI was frequently presented as a software phenomenon driven primarily by:

algorithms,

data accumulation,

cloud coordination,

and computational abstraction.

Under this interpretation, intelligence itself appeared increasingly scalable independently from geography, infrastructure, and industrial concentration.

However, the rapid expansion of AI infrastructure increasingly reveals the opposite reality.

The AI era is not reducing dependence upon physical systems.

It is restoring physical systems to the centre of technological power.

As AI systems scale, the computational intensity required to train, deploy, and coordinate advanced models expands simultaneously across:

semiconductor throughput,

electrical demand,

cooling infrastructure,

networking architecture,

hyperscale deployment systems,

and industrial manufacturing ecosystems.

This reconnects the expansion of digital intelligence directly to the physical systems capable of sustaining computational density at scale.

Under AI–energy conditions, computational expansion increasingly depends upon:

fabrication capacity,

grid continuity,

infrastructure deployment,

industrial coordination,

and energy availability.

The era of abstract computation therefore begins to give way to an era of infrastructural computation.

This transition fundamentally alters the geopolitical meaning of semiconductors.

Semiconductors are no longer merely industrial components embedded within consumer electronics supply chains.

They increasingly function as foundational infrastructure inputs into computational civilisation itself.

II. Compute Has Become Strategic Infrastructure

Under AI–energy conditions, computation increasingly functions as strategic infrastructure.

This is one of the defining structural transitions of the emerging technological era.

In earlier digital phases, computational capacity often appeared secondary to:

platforms,

applications,

software ecosystems,

and internet-scale coordination.

Today, this hierarchy increasingly reverses.

Without sufficient computational capacity:

advanced AI systems cannot scale effectively,

industrial automation weakens,

scientific acceleration slows,

military AI capability deteriorates,

cloud concentration intensifies externally,

and domestic digital ecosystems become progressively dependent upon foreign infrastructure providers.

Compute therefore increasingly resembles:

electricity infrastructure,

energy systems,

maritime corridors,

telecommunications networks,

and monetary infrastructure.

This transition matters because infrastructure systems produce long-duration asymmetries.

Infrastructure does not merely support economic activity.

It shapes:

dependency,

scaling capacity,

ecosystem concentration,

pricing leverage,

industrial coordination,

and geopolitical hierarchy over time.

As computational infrastructure scales, it increasingly compounds recursively across the wider system.

Control over compute influences:

AI capability,

industrial productivity,

financial concentration,

platform power,

military modernisation,

scientific competitiveness,

and ecosystem development simultaneously.

Computation therefore increasingly functions as an infrastructure multiplier capable of reorganising wider systems of power.

Under these conditions, semiconductor systems increasingly become sovereignty systems.

The control of compute increasingly determines:

who scales,

who compounds,

who coordinates ecosystems,

and who remains structurally dependent within externally governed technological architectures.

III. Semiconductor Fabrication and the Return of Industrial Geography

The semiconductor industry was frequently interpreted through the logic of globalisation.

Production became internationally distributed. Supply chains specialised geographically. Industrial concentration was justified primarily through efficiency optimisation and comparative advantage.

This model assumed that technological interdependence would stabilise geopolitical fragmentation.

Under AI–energy conditions, this assumption weakens considerably.

Advanced semiconductor fabrication depends upon extraordinarily concentrated industrial ecosystems requiring simultaneous coordination across:

advanced lithography,

ultra-pure materials,

precision tooling,

chemical engineering,

clean-room environments,

highly specialised labour,

electricity continuity,

infrastructure stability,

and industrial manufacturing depth.

These ecosystems cannot be reproduced rapidly.

Their complexity emerges through decades of accumulated industrial coordination, engineering concentration, infrastructure investment, and ecosystem scaling.

As a result, fabrication concentration increasingly produces structural geopolitical leverage.

The ability to manufacture advanced semiconductors increasingly determines:

AI scaling capacity,

cloud infrastructure expansion,

industrial automation capability,

military modernisation,

advanced research capacity,

and digital ecosystem control.

The semiconductor industry therefore increasingly functions less like a conventional manufacturing sector and more like a strategic infrastructure layer embedded within wider sovereignty architecture.

This transition restores industrial geography to the centre of geopolitical power.

The geography of fabrication increasingly becomes inseparable from:

the geography of energy,

the geography of infrastructure,

the geography of industrial ecosystems,

and the geography of computational sovereignty.

Under AI–energy conditions, technological power increasingly reconnects to physical concentration.

IV. AI Scaling and the Fabrication Bottleneck

The expansion of artificial intelligence increasingly reveals that computational scaling is constrained not primarily by software ambition, but by physical throughput.

This is one of the defining structural realities of the AI era.

Early digital expansion often created the perception that software could scale almost independently from industrial limitation. Cloud systems reinforced this abstraction by concealing much of the underlying infrastructure beneath increasingly seamless digital environments.

However, large-scale AI systems increasingly expose the physical foundations beneath computational expansion.

As models scale, the infrastructure required to sustain training, inference, coordination, and deployment expands simultaneously across:

advanced semiconductor fabrication,

high-bandwidth memory systems,

networking architecture,

electricity generation,

transmission infrastructure,

cooling systems,

and hyperscale data-centre deployment.

This transformation reconnects algorithmic ambition directly to industrial capacity.

Under these conditions, AI competition increasingly becomes competition over physical scaling capability.

The bottleneck therefore shifts downward into the foundational layers of the technological stack.

The critical constraint increasingly becomes whether a system possesses sufficient:

fabrication throughput,

infrastructure continuity,

electrical capacity,

industrial coordination,

and ecosystem concentration

to sustain computational density at scale.

This transition fundamentally alters the meaning of technological leadership.

The decisive question is no longer simply whether a society can produce advanced software.

The decisive question increasingly becomes whether it can sustain the industrial and infrastructural systems required to scale intelligence continuously over time.

This is why semiconductor fabrication increasingly occupies a central position within geopolitical competition.

AI systems may appear digital at the application layer.

Yet beneath the software layer, intelligence increasingly depends upon:

fabrication ecosystems,

electrical systems,

industrial manufacturing,

mineral supply chains,

and infrastructure continuity.

The AI race therefore simultaneously becomes:

an energy race,

an infrastructure race,

an industrial race,

a fabrication race,

and an ecosystem coordination race.

This dynamic increasingly favours systems capable of integrating:

energy, infrastructure, industry, compute, logistics, and capital

within coherent scaling architectures.

The ability to sustain computational expansion increasingly determines the ability to sustain technological sovereignty itself.

V. Semiconductor Ecosystems Rather Than Semiconductor Firms

Semiconductor capability is often interpreted through the lens of individual corporations.

This increasingly obscures the true structure of technological power.

Advanced semiconductor systems do not emerge from isolated firms operating independently within open markets.

They emerge from deeply integrated ecosystems requiring continuous coordination across multiple interdependent layers simultaneously.

These layers increasingly include:

fabrication plants,

lithography suppliers,

precision tooling manufacturers,

advanced chemical processing,

electrical infrastructure,

logistics systems,

university research networks,

software environments,

developer ecosystems,

industrial policy structures,

and capital allocation systems.

Under AI–energy conditions, the strategic unit of competition increasingly becomes the ecosystem rather than the firm.

This distinction is fundamental.

A fabrication facility alone does not create sovereignty.

Sovereignty increasingly depends upon whether the wider system possesses:

ecosystem continuity,

industrial depth,

infrastructure resilience,

engineering concentration,

energy stability,

and long-term scaling capacity.

The semiconductor industry therefore increasingly demonstrates a wider principle of computational civilisation:

ecosystems compound more powerfully than isolated technological assets.

This explains why technological leadership increasingly concentrates geographically.

As semiconductor ecosystems deepen, they reinforce themselves recursively through:

infrastructure concentration,

labour specialisation,

capital attraction,

supply-chain integration,

research coordination,

and ecosystem gravity.

Over time, this produces asymmetrical scaling advantages.

Systems with ecosystem depth attract:

more investment,

more engineering capability,

more infrastructure deployment,

more industrial coordination,

and more computational concentration.

Systems lacking ecosystem depth increasingly struggle to scale competitively even when they possess:

scientific expertise,

advanced firms,

or industrial fragments.

Under these conditions, semiconductor sovereignty increasingly becomes ecosystem sovereignty.

The strategic question is no longer simply:

who manufactures chips?

The deeper question increasingly becomes:

which systems can sustain the entire industrial architecture required for computational civilisation?

This transition is central to the wider AI–energy framework because AI infrastructure does not scale through isolated innovation alone.

It scales through the recursive integration of:

energy systems,

industrial systems,

compute systems,

infrastructure systems,

logistics systems,

and capital systems.

Semiconductor ecosystems therefore increasingly function as strategic coordination architectures embedded within wider sovereignty structures.

VI. Energy and Semiconductors Are Converging

The semiconductor question can no longer be separated from the energy question.

Under AI–energy conditions, these systems increasingly converge structurally within the same infrastructure architecture.

This convergence accelerates because computational expansion is becoming progressively more electricity-intensive.

As AI systems scale, the energy required to sustain:

training,

inference,

networking,

cooling,

and hyperscale deployment

expands simultaneously across the wider computational ecosystem.

This transformation increasingly links semiconductor competitiveness directly to:

grid stability,

electricity pricing,

transmission infrastructure,

cooling availability,

industrial energy continuity,

and infrastructure resilience.

Under earlier digital conditions, software platforms often appeared relatively detached from energy geography.

Under AI–energy conditions, this abstraction weakens rapidly.

The geography of compute increasingly becomes the geography of electricity.

This transition is fundamental.

Advanced semiconductor ecosystems increasingly require:

stable baseload electricity,

large-scale infrastructure continuity,

resilient transmission systems,

industrial cooling capacity,

and long-duration investment coordination.

As computational density expands, electricity systems increasingly become embedded within technological competitiveness itself.

This changes the logic of semiconductor geography.

Regions capable of aligning:

low-cost energy,

infrastructure continuity,

industrial concentration,

and compute deployment

acquire progressively greater advantages in AI scaling capacity.

Under these conditions, semiconductor ecosystems increasingly converge with:

energy systems,

industrial corridors,

logistics architecture,

infrastructure geography,

and sovereignty systems.

This convergence also explains why AI has become physical.

The expansion of intelligence infrastructure increasingly reconnects computational systems to:

power grids,

mineral extraction,

transmission corridors,

industrial manufacturing,

cooling systems,

and physical infrastructure deployment.

The technological stack therefore increasingly reconnects to the material systems beneath it.

Semiconductor systems no longer operate merely inside the digital economy.

They increasingly function inside a wider energy–industrial civilisation architecture in which computational power depends directly upon the physical systems capable of sustaining it.

Under these conditions, semiconductor sovereignty increasingly becomes inseparable from:

energy sovereignty,

infrastructure sovereignty,

industrial sovereignty,

and ecosystem sovereignty simultaneously.

VII. Compute Sovereignty and the New Infrastructure Hierarchy

Compute sovereignty is increasingly emerging as one of the foundational layers of geopolitical power.

This reflects a wider structural reorganisation of the global system under AI–energy conditions.

Earlier geopolitical eras were shaped primarily through control over:

maritime systems,

industrial manufacturing,

hydrocarbon energy,

trade corridors,

and monetary infrastructure.

These systems determined:

economic scale,

military reach,

industrial productivity,

financial leverage,

and geopolitical hierarchy.

The AI era does not replace these systems.

It increasingly integrates computational infrastructure into them.

As a result, compute increasingly functions as a sovereignty multiplier across the wider architecture of power.

Control over computational infrastructure increasingly influences:

scientific acceleration,

military modernisation,

industrial productivity,

financial concentration,

ecosystem scaling,

platform dominance,

automation capability,

and strategic coordination capacity simultaneously.

This transformation changes the hierarchy of infrastructure itself.

Computation no longer functions merely as a support layer for economic activity.

It increasingly becomes one of the systems through which economic power is organised, scaled, and governed.

Under these conditions, the control of compute increasingly shapes:

who captures technological rents,

who governs digital ecosystems,

who concentrates capital,

who scales AI capability,

and who remains dependent upon externally governed infrastructure.

This produces a new hierarchy of dependency inside computational civilisation.

A state or region may retain:

formal political sovereignty,

industrial capacity,

regulatory authority,

and financial sophistication,

while still remaining structurally dependent if:

advanced semiconductors,

cloud infrastructure,

operating systems,

AI deployment environments,

or hyperscale compute capacity

are governed externally.

This dependency increasingly propagates upward through the wider stack.

Weakness at the compute layer gradually affects:

platform development,

industrial competitiveness,

developer ecosystems,

AI scaling capability,

capital retention,

and strategic autonomy.

This is why compute sovereignty increasingly becomes inseparable from:

industrial sovereignty,

energy sovereignty,

digital sovereignty,

platform sovereignty,

and infrastructure sovereignty.

The AI era increasingly reorganises power around the systems capable of integrating these layers coherently.

Under these conditions, semiconductor control increasingly becomes part of a wider struggle over the governance architecture of computational civilisation itself.

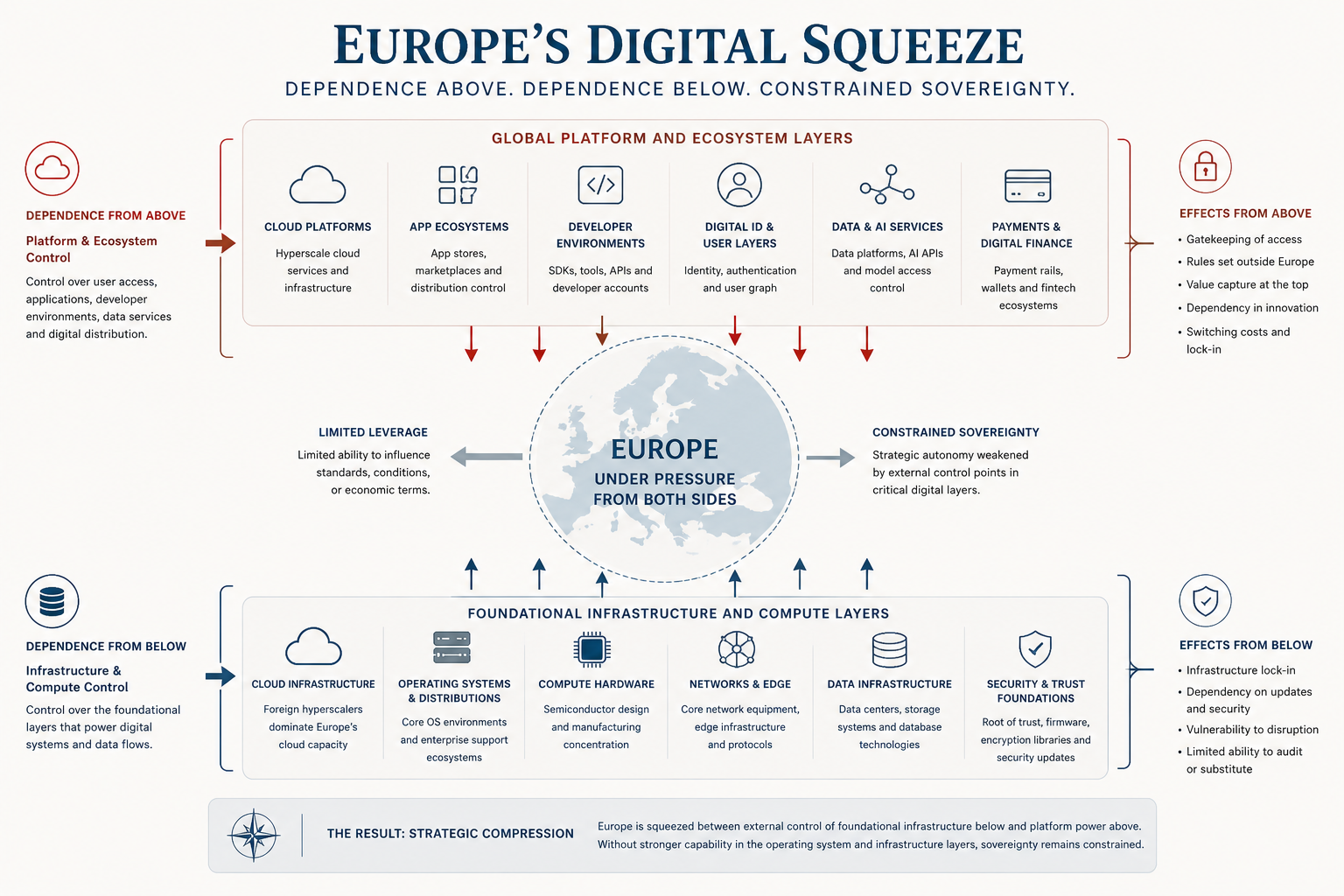

VIII. Europe and Structural Dependency

Europe’s semiconductor challenge is not fundamentally a technological problem in isolation.

It is a systemic conversion problem.

The continent retains substantial:

scientific capability,

industrial sophistication,

infrastructure density,

engineering capacity,

manufacturing depth,

and regulatory influence.

However, under AI–energy conditions, these capabilities do not automatically translate into sovereign computational power.

The central issue increasingly becomes whether Europe can convert:

industrial capability, infrastructure capacity, energy systems, scientific research, and capital

into coherent computational ecosystems capable of scaling autonomously.

This is where Europe increasingly encounters structural difficulty.

The continent remains highly exposed across multiple layers simultaneously:

advanced semiconductor fabrication,

hyperscale cloud infrastructure,

GPU concentration,

operating systems,

AI deployment environments,

developer ecosystems,

and platform governance.

This exposure is intensified by:

fragmented capital allocation,

uneven infrastructure integration,

higher industrial energy costs,

incomplete digital scaling,

and weaker ecosystem concentration relative to the United States and East Asia.

Under earlier economic conditions, Europe could often compensate for these weaknesses through:

industrial exports,

regulatory influence,

manufacturing quality,

and integration into global trade systems.

Under AI–energy conditions, these compensatory mechanisms become progressively less sufficient.

This is because AI infrastructure increasingly compounds recursively.

Systems capable of concentrating:

compute,

capital,

energy,

infrastructure,

and ecosystems

gain progressively stronger scaling advantages over time.

Meanwhile, fragmented systems increasingly struggle to sustain competitive computational expansion.

Europe therefore risks participating in the AI economy primarily through externally governed infrastructure architectures.

This creates structural asymmetries across:

cloud dependency,

platform dependence,

capital leakage,

AI deployment,

ecosystem concentration,

and technological governance.

The problem is therefore not simply innovation.

Nor is it simply industrial decline.

The deeper issue is that Europe increasingly lacks a fully integrated conversion architecture capable of transforming:

industrial depth,

scientific capability,

energy infrastructure,

and capital resources

into sovereign computational ecosystems.

This is why the semiconductor question increasingly intersects directly with:

energy systems,

infrastructure integration,

industrial policy,

digital sovereignty,

and ecosystem coordination.

The challenge is no longer merely technological catch-up.

The challenge increasingly concerns whether Europe can sustain sufficient system integration to remain an autonomous actor within computational civilisation.

IX. The Mediterranean and the Geography of AI Infrastructure

Under AI–energy conditions, the Mediterranean increasingly emerges as a strategic infrastructure interface within the future geography of European computational power.

This transition is fundamental to understanding the wider architecture of semiconductor sovereignty.

The AI era increasingly depends upon the large-scale integration of:

electricity systems,

subsea cable infrastructure,

logistics corridors,

distributed compute architectures,

cooling geography,

industrial reshoring,

transmission networks,

and hyperscale infrastructure deployment.

The Mediterranean sits directly at the intersection of these systems.

This geography increasingly connects:

North African energy systems,

Southern European industrial corridors,

LNG infrastructure,

subsea digital connectivity,

renewable energy expansion,

electricity interconnection,

maritime logistics,

and emerging distributed compute networks.

Under earlier geopolitical frameworks, Southern Europe was frequently interpreted primarily through the language of peripheral weakness and structural dependency.

Under AI–energy conditions, this interpretation increasingly becomes incomplete.

As computational infrastructure expands, AI deployment increasingly follows:

electricity stability,

infrastructure continuity,

cooling availability,

transmission capacity,

and physical deployment geography.

This transition gradually increases the strategic importance of:

energy corridors,

port systems,

interconnectors,

distributed infrastructure networks,

and Mediterranean logistical positioning.

The Mediterranean therefore increasingly functions not as a peripheral zone external to European technological development, but as:

a conversion interface between energy systems and computational systems.

This transition is strategically significant because Europe’s future computational position may depend increasingly upon whether Mediterranean infrastructure can be integrated into a wider European conversion architecture.

The Mediterranean increasingly possesses structural advantages across:

renewable energy scaling,

maritime positioning,

subsea connectivity,

distributed infrastructure geography,

logistics integration,

and electricity interconnection potential.

Under AI–energy conditions, these systems increasingly become directly relevant to:

compute locality,

edge AI deployment,

infrastructure resilience,

industrial decentralisation,

and distributed computational scaling.

This transformation alters the geopolitical meaning of Southern Europe.

The Mediterranean increasingly shifts from:

perceived peripheral exposure

toward:

strategic infrastructural centrality within the future European compute system.

Semiconductor sovereignty therefore cannot be understood solely through fabrication facilities or chip design.

It must increasingly be understood through the wider geography of:

energy systems,

infrastructure corridors,

industrial ecosystems,

logistics integration,

and computational deployment architectures.

Under these conditions, the Mediterranean increasingly becomes one of the physical foundations through which European computational sovereignty may either consolidate or fragment.

X. Semiconductor Sovereignty as System Sovereignty

Semiconductors are no longer merely industrial components embedded within consumer technology systems.

Under AI–energy conditions, they increasingly function as foundational infrastructure layers within computational civilisation itself.

This transformation changes the meaning of technological power.

The expansion of artificial intelligence increasingly reconnects computational capability to:

semiconductor fabrication,

electrical systems,

industrial manufacturing,

strategic minerals,

logistics architecture,

cooling infrastructure,

transmission networks,

and ecosystem concentration.

As a result, digital power increasingly becomes inseparable from physical infrastructure capacity.

The AI era therefore does not diminish the importance of industrial systems.

It restores industrial systems to the centre of geopolitical hierarchy.

This transition is fundamental because computation increasingly operates as a recursive infrastructure layer across the wider global system.

Control over semiconductors increasingly influences:

AI scaling,

industrial productivity,

military modernisation,

scientific acceleration,

platform concentration,

ecosystem development,

and capital accumulation simultaneously.

Under these conditions, semiconductor sovereignty can no longer be understood narrowly as a sectoral industrial issue.

It increasingly becomes:

infrastructure policy,

energy policy,

industrial policy,

ecosystem policy,

digital policy,

and geopolitical strategy simultaneously.

This is why the semiconductor question increasingly intersects directly with:

energy sovereignty,

compute sovereignty,

platform sovereignty,

infrastructure sovereignty,

and ecosystem sovereignty.

The strategic issue is no longer merely whether a country can manufacture advanced chips.

The deeper question increasingly becomes whether a system can sustain the full architecture required for sovereign computational scaling.

This architecture increasingly includes:

energy continuity,

infrastructure resilience,

industrial concentration,

ecosystem coordination,

logistics integration,

software environments,

capital depth,

and long-duration scaling capacity.

Under AI–energy conditions, these layers increasingly compound recursively.

Systems capable of integrating:

energy, infrastructure, industry, compute, ecosystems, logistics, and capital

acquire progressively greater structural leverage over time.

Systems unable to sustain this integration increasingly risk dependency upon externally governed computational infrastructures.

This transition fundamentally reorganises the architecture of sovereignty itself.

Earlier eras of globalisation encouraged the perception that software, finance, and digital coordination could increasingly detach power from geography and industrial concentration.

The AI era increasingly reverses this abstraction.

As intelligence infrastructure scales, physical systems progressively return to the centre of economic and geopolitical power.

Industrial geography reasserts itself.

Infrastructure density regains strategic importance.

Energy systems become embedded within computational competitiveness.

Fabrication ecosystems become leverage systems.

And semiconductor control increasingly becomes one of the foundational determinants of long-term technological autonomy.

The semiconductor industry therefore increasingly represents far more than a technological sector.

It increasingly represents one of the critical infrastructure foundations through which computational civilisation will be organised, governed, and scaled.

Under these conditions, semiconductor sovereignty increasingly determines whether societies participate in the AI era:

as sovereign system-builders capable of shaping computational infrastructure,

or:

as dependent consumers operating inside externally governed technological architectures.

This is why semiconductor control increasingly becomes inseparable from the wider question of system sovereignty itself.