SME Innovation Networks and the European Scaling Constraint

Distributed Energy, Local Compute, Cost, Control, and Industrial Learning

Keynote

Europe’s economic structure is often described as fragmented and difficult to scale.

This interpretation is incomplete.

As energy systems become electrified and distributed, and as computation becomes central to production, Europe’s structure begins to align with a different model of industrial organisation.

This model is not based on concentration.

It is based on coordination across distributed systems.

These systems include:

local energy availability

digitally coordinated production

ecosystem-based innovation

The strategic question is no longer whether Europe can scale like the United States or China.

The strategic question is whether Europe can scale through a different system architecture.

This alternative architecture would convert:

distributed energy into a cost advantage

localised computation into a control advantage

SME networks into coordinated industrial ecosystems

SMEs are central to this transition.

I. The Structure Europe Already Has

Europe’s economic system is built around SMEs.

These firms are:

regionally distributed

highly specialised

embedded in local economies

This structure has traditionally been interpreted as a limitation.

Scaling requires coordination across many firms.

Markets and regulatory systems remain fragmented.

Access to capital is uneven.

As a result, Europe often generates innovation but struggles to industrialise that innovation at scale.

This interpretation reflects an industrial model based on centralisation.

Under conditions of structural transformation, this same structure may represent a latent system advantage.

II. Industrial Ecosystems and Learning Dynamics

European SMEs do not operate as isolated units.

They operate within industrial ecosystems.

Within these ecosystems, innovation emerges through continuous interaction between design, suppliers, manufacturing, and engineering feedback.

This interaction can be understood as a learning loop.

Design decisions influence production processes.

Suppliers specialise and improve their capabilities.

Manufacturing generates process knowledge.

Engineering feedback improves products and systems.

System capability accumulates over time.

This process creates distributed industrial intelligence.

Innovation is not concentrated within a single firm.

It is embedded within the ecosystem.

This mechanism explains how industrial capability scales in practice.

III. Global Value Chains as Learning Systems

During the globalisation period, this learning process operated at a global scale.

Global value chains were not only systems of cost optimisation.

They were also systems of capability diffusion and industrial learning.

Production networks linking firms across regions enabled:

supplier upgrading

engineering knowledge transfer

process innovation through scale

rapid iteration cycles

Over time, these dynamics transformed manufacturing regions into dense innovation ecosystems.

Industrial systems evolved through a sequence:

assembly

→ capability accumulation

→ integrated technological ecosystems

This process explains the development of industrial capacity in sectors such as:

electronics

batteries

electric vehicles

renewable energy technologies

IV. Europe’s Structural Gap: Loss of Ecosystem Density

Europe did not lose only manufacturing volume.

Europe also lost ecosystem density.

The weakening of industrial feedback loops reduced the ability of SMEs to:

scale innovation

coordinate production

accumulate system-level capability

This condition produces a structural imbalance.

Innovation exists, but scaling fails.

This is not primarily a technological constraint.

It is a system coordination constraint.

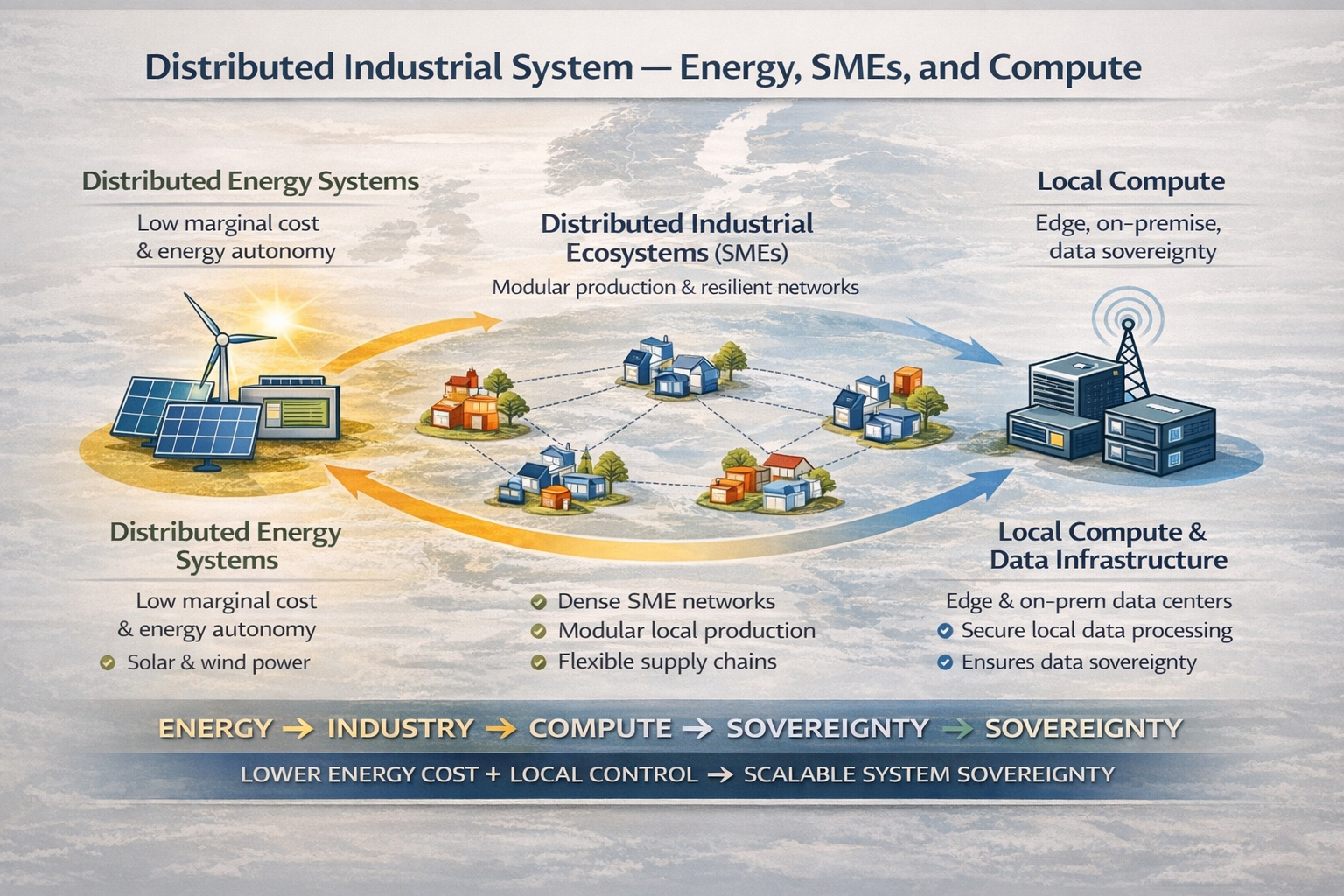

V. Distributed Energy as a Cost Foundation

The energy transition changes the structure of production costs.

Traditional energy systems are based on:

imported fuels

continuous variable costs

exposure to global price volatility

Renewable energy systems are characterised by:

high initial capital investment

very low marginal cost after deployment

This creates a structural shift.

When energy can be produced locally at low marginal cost, production can also become more local and cost-competitive.

For SMEs, this shift is significant.

Energy is a primary input cost.

Lower marginal energy costs improve long-term viability.

Local energy generation reduces exposure to external shocks.

However, the transition remains incomplete.

Infrastructure is uneven.

Upfront costs are high.

Short-term price volatility persists.

The cost advantage exists, but it is not yet fully realised at the system level.

VI. Localised Compute as a Control Layer

Production processes are increasingly dependent on computation.

These processes include:

automation

AI-assisted production

digital coordination across firms

At present, much of this computation is:

centralised

externally controlled

dependent on global platforms

This creates structural vulnerabilities for SMEs.

First, SMEs face a control constraint.

They depend on infrastructure that they do not control.

Second, SMEs face a data constraint.

Industrial data is transferred outside local systems, reducing value

capture.

Localised or regionally embedded compute changes this dynamic.

Data can remain within European systems.

Coordination can occur without external dependency.

SMEs can participate without surrendering control.

If energy defines cost, compute location defines control.

VII. The Missing Link: System Coordination

Distributed energy and localised compute do not automatically generate scale.

They require system coordination.

SMEs already operate within networks.

However, these networks are not fully integrated at the system level.

What is required includes:

interoperable digital infrastructure

shared compute systems

integrated energy networks

coordinated industrial platforms

Without coordination:

energy advantages remain localised

compute remains externally controlled

scaling remains limited

With coordination:

distributed production becomes a system

SMEs operate as coordinated ecosystems

scale emerges from connection rather than concentration

VIII. Strategic and Geopolitical Implications

Technological competition is not defined only by innovation.

It is defined by system architecture.

Different system configurations are emerging.

The United States is characterised by:

hyperscale compute infrastructure

capital concentration

platform dominance

China is characterised by:

dense industrial ecosystems

integrated supply chains

coordinated industrial scaling

Europe is characterised by:

distributed SME networks

emerging distributed energy systems

potential for localised compute

Europe’s position is not structurally weak.

It is structurally incomplete.

If these elements are aligned, Europe could develop a distinct system architecture.

This architecture would consist of:

distributed industrial ecosystems

local energy-based cost structures

sovereign or regional compute systems

This would represent a third model of system power.

Without alignment, Europe risks:

persistent fragmentation

capital outflows

technological dependency

declining industrial relevance

IX. Preconditions for European System Formation

For this system to function, several conditions must be met.

Energy system alignment

accelerated renewable deployment

expansion and integration of grids

development of storage systems

reform of energy pricing structures

Compute system alignment

development of local and regional compute infrastructure

establishment of interoperability standards

implementation of data governance frameworks

Ecosystem coordination

development of SME coordination platforms

strengthening of supplier networks

support for industrial clustering

Capital alignment

alignment of investment with system architecture

development of long-term infrastructure financing

reduction of fragmentation in capital markets

Without alignment across these layers, system formation cannot occur.

X. Implication

Europe does not need to replicate centralised industrial models.

Its structure already corresponds to a different configuration.

This configuration includes:

distributed firms

emerging distributed energy systems

potential for localised computation

The constraint is not the absence of capability.

The constraint is the absence of system alignment under conditions of energy constraint.

Strategic Insight

Industrial power is not determined by individual firms alone.

Industrial power is determined by the density and coordination of ecosystems through which learning, production, and innovation occur.

Global value chains demonstrated this principle at a global scale.

The European challenge is to reconstruct this dynamic at a regional and system level.

The European challenge is not only to rebuild industrial capacity, but to align ecosystems, energy systems, and technological stacks into a coherent system architecture capable of scaling under constraint.

System Logic and Constraint

Beyond Ideology

This article explains why ideological frameworks delay structural adjustment under conditions of structural constraint.The Legitimacy Boundary

This article defines the limits within which economic and social systems remain politically and economically sustainable.Legitimacy, Labour, and System Durability

This article examines how labour structures and income distribution shape long-term system stability.

Industrial Ecosystems and Capability Formation

Global Value Chains as Innovation Systems

This article explains how global production networks function as systems of industrial learning and capability diffusion.Global Value Chains in an Energy-Bound World

This article situates global value chains within the constraints of energy systems and evolving cost structures.SME Innovation Networks and the European Scaling Constraint

This article explains how SME-based industrial ecosystems can function as distributed systems of production and innovation.

Technology Stacks and System Architecture

Energy–Industry–Compute Stack

This article defines the structural hierarchy through which energy systems propagate into industrial capability, compute infrastructure, and economic power.System Stack Architecture

This article explains how technological systems are organised across layers from infrastructure to applications.Stacks, Systems, and Sovereignty

This article examines how control over technological stacks determines sovereignty and strategic autonomy.

Control Layers — Compute, Standards, and Platforms

Operating Systems and System Control

This article explains how operating systems function as control layers between hardware, software, and users.Standards, Protocols, and System Control

This article analyses how rules of interaction shape technological ecosystems and determine control over systems.Developer Ecosystems and Scaling

This article explains how coordination at the software and developer level enables scaling across distributed systems.

Digital and Compute Infrastructure

AI, Energy, and the Future of Sovereignty

This article explains how compute infrastructure is constrained by energy systems and shapes geopolitical power.AI–Energy–Cost Chasm

This article examines the structural gap between rising compute demand and constrained energy supply.Cloud and Edge AI

This article analyses the distribution of computation between centralised and decentralised systems.

Technology, IP, and Geopolitical Competition

- Intellectual

Property and Future Technologies

This article analyses how intellectual property regimes interact with technological competition and capability formation.