Hyperscalers and Centralised Compute Power

How Compute Concentration, Cloud Scale, and Platform Ecosystems Consolidate Power in the AI Era

System Navigation

This article examines the ecosystem and operational dynamics of hyperscaler concentration under AI conditions.

For the broader sovereignty and infrastructure doctrine layer see:

→ Hyperscaler Infrastructure Sovereignty

This article should also be read alongside:

Central Thesis

The rise of hyperscalers represents one of the most important structural transformations of the AI era.

For much of the digital age, technological competition appeared relatively decentralised.

Software companies could emerge rapidly.

Startups could scale with comparatively limited capital.

Cloud systems reduced infrastructure burdens.

Open internet architectures appeared to lower barriers to participation.

The AI transition increasingly reverses these dynamics.

Large-scale artificial intelligence depends progressively on extraordinary concentrations of:

compute power,

semiconductor access,

cloud infrastructure,

training capacity,

orchestration systems,

engineering talent,

energy access,

developer ecosystems,

and capital.

This produces increasing structural advantages for firms capable of operating hyperscale infrastructure systems.

Hyperscalers therefore become progressively more than large technology firms.

They become integrated compute ecosystems capable of coordinating:

cloud infrastructure,

AI model deployment,

developer environments,

platform ecosystems,

enterprise integration,

edge deployment,

and global computational scaling.

The strategic significance of hyperscalers derives not merely from corporate size.

It derives increasingly from their ability to centralise computational capability across multiple layers of the digital stack.

Under AI conditions, compute concentration increasingly shapes:

ecosystem power,

platform dominance,

innovation pathways,

enterprise dependency,

developer behaviour,

and market structure itself.

The AI era therefore accelerates the transition from fragmented digital ecosystems toward increasingly centralised compute architectures.

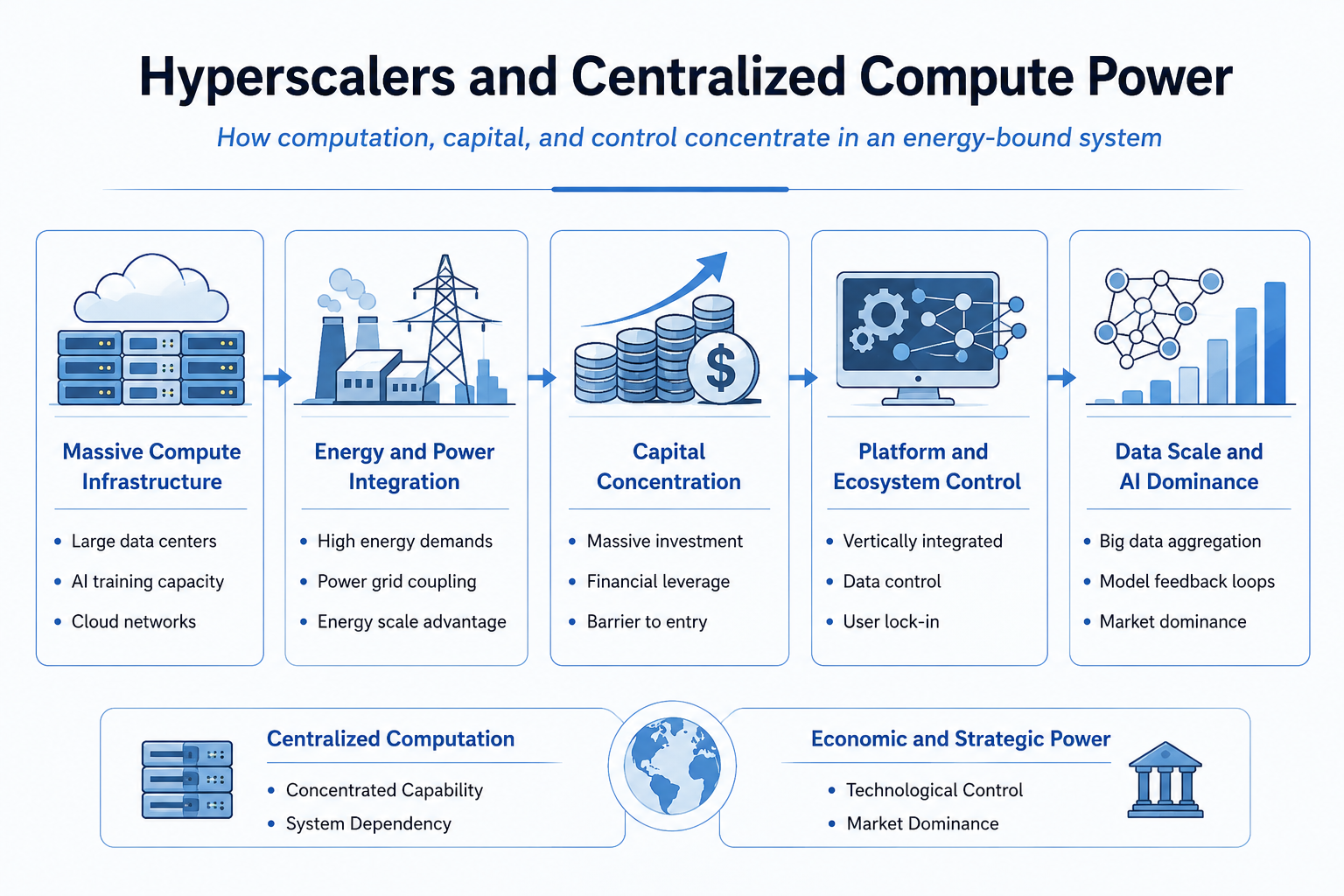

I. The Centralisation of Compute

Artificial intelligence dramatically increases the importance of large-scale computational infrastructure.

Training advanced AI systems requires enormous computational resources.

Inference deployment at scale also requires persistent compute availability, orchestration systems, networking infrastructure, and highly optimised cloud environments.

This creates progressively higher barriers to entry.

Earlier phases of the software economy allowed relatively small firms to compete through software innovation alone.

Under AI conditions, however, software increasingly depends upon access to hyperscale infrastructure.

The decisive competitive advantage shifts from software abstraction toward compute access.

This transition favours firms possessing:

hyperscale cloud infrastructure,

semiconductor procurement power,

massive data centre capacity,

global networking systems,

AI deployment infrastructure,

and deep capital reserves.

As a result, AI scaling progressively concentrates inside a relatively small number of hyperscale ecosystems.

This concentration is not accidental.

It is increasingly structural.

The economics of AI favour systems capable of distributing enormous fixed infrastructure costs across planetary-scale user bases.

This creates reinforcing scale advantages.

More compute capacity enables larger AI models.

Larger AI models attract more developers and enterprises.

More developers and enterprises generate more usage.

More usage finances additional infrastructure expansion.

Infrastructure expansion further deepens compute advantages.

This creates increasingly self-reinforcing hyperscale ecosystems.

II. Cloud Infrastructure and Ecosystem Dependency

Cloud infrastructure increasingly functions as the operational foundation of the AI economy.

Enterprise systems, software deployment, AI services, developer environments, APIs, data storage, orchestration layers, and AI inference systems increasingly depend on hyperscale cloud environments.

This produces new forms of ecosystem dependency.

The strategic significance of cloud dominance derives not merely from hosting capacity.

It derives increasingly from ecosystem integration.

Hyperscalers progressively integrate:

cloud services,

AI models,

orchestration systems,

enterprise tooling,

APIs,

security systems,

developer environments,

data pipelines,

and deployment architectures.

This creates increasingly integrated computational ecosystems.

The result is not simply software dependence.

It is infrastructural dependence.

As enterprises integrate deeper into hyperscale ecosystems, migration costs rise progressively.

Operational systems become increasingly dependent upon:

proprietary APIs,

cloud-native architectures,

orchestration tooling,

AI integration layers,

and hyperscaler deployment environments.

This creates powerful ecosystem lock-in effects.

Under AI conditions, cloud infrastructure increasingly becomes:

the operating environment through which intelligence itself is accessed and deployed

This dramatically strengthens hyperscaler leverage across the digital economy.

III. Developer Ecosystems and Platform Gravity

Developer ecosystems increasingly determine the scaling dynamics of technological power.

The most powerful hyperscale ecosystems are not merely infrastructure providers.

They are developer environments.

Developers increasingly build applications, services, AI integrations, and enterprise systems directly inside hyperscale architectures.

This creates ecosystem gravity.

The more developers build within a platform environment:

the more tooling improves,

the more integrations emerge,

the more enterprise adoption expands,

the more data flows increase,

and the more ecosystem dependency deepens.

AI intensifies this process.

Foundation models, AI APIs, orchestration systems, vector databases, inference infrastructure, and deployment frameworks increasingly become integrated directly into hyperscale developer ecosystems.

As a result, developers increasingly optimise around:

hyperscaler infrastructure,

hyperscaler tooling,

hyperscaler APIs,

and hyperscaler deployment architectures.

This strengthens platform concentration.

The strategic issue therefore extends beyond software innovation itself.

The decisive issue concerns:

which ecosystems become the default environments through which future software, intelligence, and enterprise systems are built

Under AI conditions, developer ecosystems increasingly function as strategic scaling architectures.

IV. APIs, AI Models, and Computational Gatekeeping

Artificial intelligence increasingly operates through API-mediated ecosystems.

This creates a new layer of computational gatekeeping.

AI capabilities increasingly become accessible not through direct ownership of infrastructure, but through controlled access to hyperscale AI systems.

This shifts the structure of computational power.

Instead of distributing compute ownership broadly across the economy, hyperscale systems increasingly centralise compute while distributing controlled access.

This distinction is critical.

The user may access intelligence.

But the infrastructure producing intelligence remains centrally controlled.

This creates asymmetrical ecosystem structures.

Hyperscalers increasingly determine:

access conditions,

pricing structures,

compute allocation,

deployment permissions,

integration standards,

model access,

and optimisation pathways.

This produces increasingly platformised intelligence systems.

Under AI conditions, APIs increasingly become:

governance interfaces for access to computational capability

This creates new forms of dependency across:

startups,

enterprises,

governments,

software ecosystems,

and industrial systems.

The strategic issue is therefore not simply whether AI becomes widely available.

The issue concerns who controls the infrastructure layers through which access is mediated.

V. Edge AI, Platform Expansion, and Stack Integration

The expansion of edge AI strengthens hyperscaler ecosystems even further.

AI deployment increasingly extends beyond centralised cloud systems toward:

devices,

enterprise systems,

industrial systems,

logistics infrastructure,

robotics,

vehicles,

and distributed edge environments.

This creates a larger integrated compute stack.

Hyperscalers increasingly coordinate:

cloud infrastructure,

operating systems,

AI deployment,

edge inference,

enterprise integration,

and device ecosystems.

This integration strengthens ecosystem dominance.

The strategic significance of platform ecosystems therefore increases under AI conditions.

The most powerful systems increasingly combine:

infrastructure scale,

software ecosystems,

AI deployment,

cloud coordination,

developer dependency,

and edge integration.

This produces vertically integrated compute architectures.

Under AI conditions, technological power increasingly derives from:

stack integration across cloud, AI, operating systems, infrastructure, and deployment environments

This explains why platform sovereignty becomes increasingly important.

The decisive strategic advantage increasingly belongs not to isolated software products, but to integrated ecosystems capable of coordinating entire computational environments.

VI. The Economics of Hyperscale Expansion

AI scaling requires enormous capital expenditure.

Hyperscalers therefore benefit from powerful financial scale advantages.

The construction of hyperscale ecosystems increasingly requires:

semiconductor procurement,

massive data centre expansion,

energy procurement,

cooling infrastructure,

global networking,

AI model training,

and long-term infrastructure financing.

This favours firms possessing:

deep capital access,

large balance sheets,

global cloud revenues,

and infrastructure financing capacity.

The AI transition therefore increases barriers to entry.

Smaller firms may continue to innovate.

But scaling increasingly depends upon access to hyperscale ecosystems.

This creates asymmetric market structures.

Innovation remains distributed.

Infrastructure control becomes concentrated.

Under these conditions, hyperscalers increasingly function as:

the financial and infrastructural backbone of large-scale AI deployment

This reinforces compute centralisation across the global digital economy.

VII. Centralised Compute and Strategic Dependency

The concentration of compute infrastructure creates broader strategic consequences.

As economies become increasingly dependent on AI systems, dependency on hyperscale ecosystems also expands.

This dependency extends across:

enterprise software,

industrial systems,

logistics coordination,

cloud infrastructure,

AI deployment,

public services,

and digital governance.

The result is increasing systemic dependence on externally controlled computational architectures.

Under these conditions, digital dependency increasingly becomes compute dependency.

The strategic issue therefore concerns more than market concentration.

It concerns the concentration of operational computational capability itself.

As artificial intelligence becomes embedded deeper into economic systems, hyperscalers increasingly shape:

the availability of computational resources,

the structure of digital ecosystems,

the deployment of AI capability,

and the operational conditions under which digital economies function.

This explains why compute concentration becomes increasingly important to:

digital sovereignty,

technological competition,

industrial policy,

and geopolitical power.

VIII. Conclusion — Hyperscalers and the New Compute Order

The rise of hyperscalers represents one of the defining structural transformations of the AI era.

Artificial intelligence increasingly rewards:

scale,

infrastructure integration,

compute concentration,

ecosystem coordination,

and capital intensity.

This strengthens hyperscale ecosystems across the global digital economy.

The strategic significance of hyperscalers therefore extends far beyond cloud services alone.

Hyperscalers increasingly coordinate:

compute infrastructure,

AI deployment,

platform ecosystems,

developer environments,

edge integration,

enterprise systems,

and digital scaling architectures.

As AI systems expand, the concentration of compute increasingly shapes:

technological competition,

ecosystem power,

market dependency,

innovation pathways,

and digital sovereignty itself.

The decisive issue is no longer simply who builds software.

The decisive issue increasingly concerns:

who controls the computational infrastructure through which intelligence, platforms, ecosystems, and digital economic activity are scaled

Under AI conditions, hyperscalers increasingly become:

the operational core of the emerging centralised compute order