AI, Energy, and Platform Power

The System Architecture of the US MAG7

System Navigation

The system unfolds across three layers:

Foundations → Dynamics → Outcomes

Energy-Bound System → AI–Energy–Cost Chasm → Energy Constraint and the Monetary Ceiling

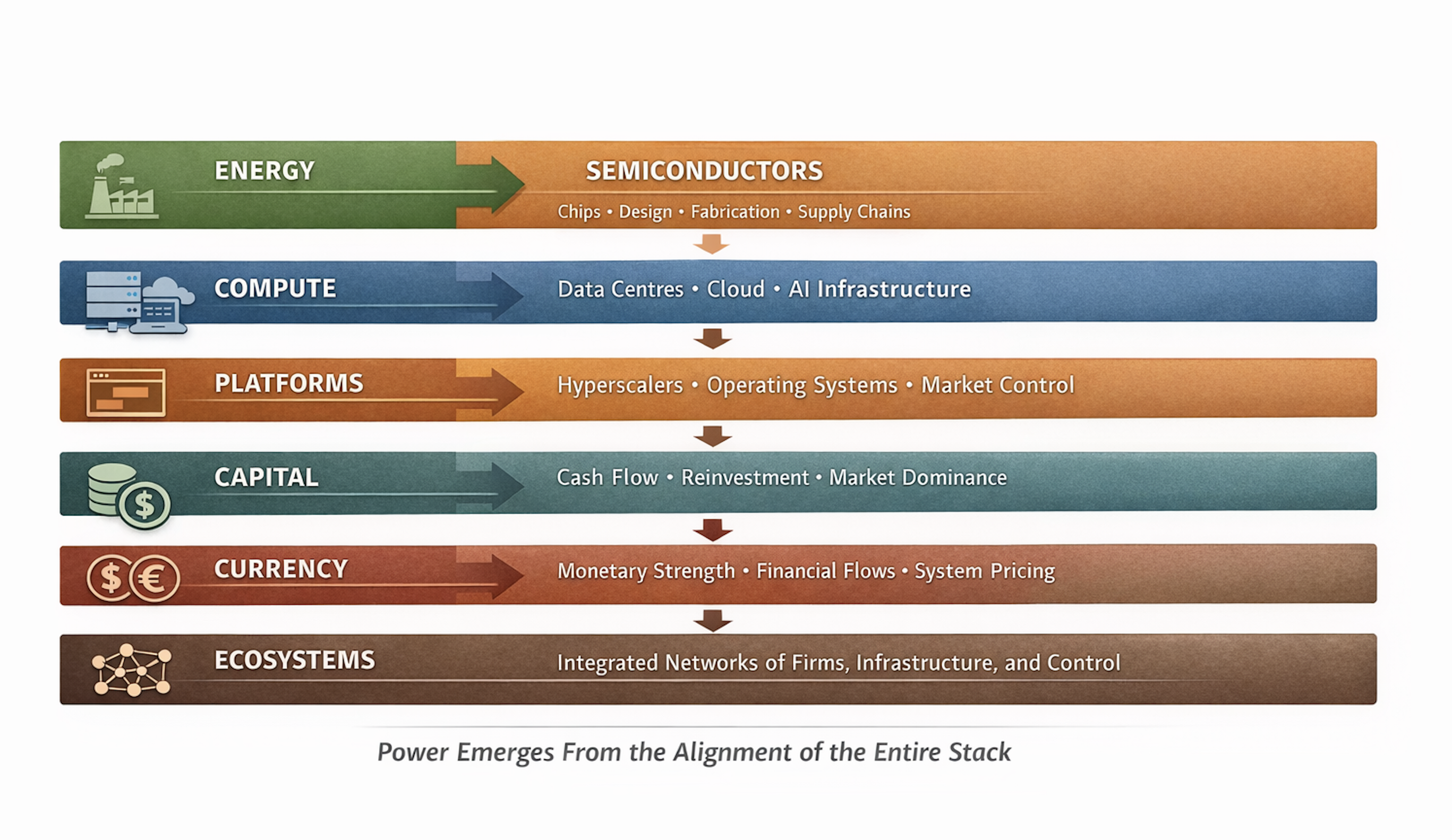

System Architecture — Energy to Monetary Power

I. The Misreading of Power

The dominance of US technology firms is often explained through:

innovation

software ecosystems

entrepreneurial culture

These explanations are incomplete.

They describe outcomes, not structure.

The US MAG7 — Apple, Microsoft, Amazon, Google, Meta, Nvidia, and Tesla — should be understood as a system, not a collection of firms.

A system defined by the integration of:

energy

compute infrastructure

semiconductor ecosystems

global value chains

capital markets

→ See also:

Energy–Industry–Compute

Convergence

Energy

Systems and the Tech War

II. Compute is Energy Infrastructure

AI scaling is not primarily a software problem.

It is an energy problem.

Training, inference, and continuous deployment require:

large-scale data centres

high-density compute clusters

stable and abundant electricity

Compute scaling = energy scaling

The geography of AI is therefore constrained by:

access to low-cost power

grid capacity

infrastructure deployment speed

→ See:

Compute

Locality in an Energy-Bound System

Energy–Compute

Infrastructure Geography

III. The Semiconductor Layer: Control of the Bottleneck

At the core of the system sits the semiconductor stack.

Advanced AI systems depend on:

- high-performance GPUs

- specialised chips

- tightly integrated hardware–software ecosystems

This creates a structural bottleneck.

Control is not exercised at the level of individual firms

alone.

It is embedded within semiconductor ecosystems that

combine:

- design

- fabrication

- tooling

- and supply chain coordination

Semiconductors are the gating mechanism of the AI system

→ See:

AI

Compute Ecosystems

Semiconductor

Ecosystems

IV. Global Value Chains and Ecosystem Control

The system extends beyond national borders through global value chains.

The work of Patrick McGee on Apple’s supply chain illustrates this clearly.

Apple is not simply a product company.

It is:

- an orchestrator of a global manufacturing ecosystem

- deeply embedded in Chinese industrial capacity

- structurally dependent on coordinated production networks

This reveals a key principle:

Control does not require domestic production.

It requires control over ecosystems — design, coordination, and value capture.

The MAG7 system operates through:

- distributed production

- centralised coordination

- ecosystem dependency

→ See:

Global

Value Chains in an Energy-Bound World

Corridors,

Chokepoints, and the Geography of Leverage

V. Ecosystems as the Unit of Power

In industrial-era analysis, firms were the primary unit of competition.

In the AI and energy-constrained era, this has shifted.

The relevant unit is the ecosystem.

An ecosystem combines:

- infrastructure

- firms

- supply chains

- capital flows

- and coordination mechanisms

The US advantage lies not only in leading companies, but in:

- tightly integrated compute ecosystems

- dominant semiconductor ecosystems

- globally embedded production networks

- capital markets that reinforce system expansion

Power now resides in the ability to build, coordinate, and scale ecosystems — not in isolated firms.

→ See:

AI

Compute Ecosystems

Semiconductor

Ecosystems SME Innovation

Networks

VI. Platform Power as System Integration

The MAG7’s advantage lies in integration across layers.

But this integration is not vertical in a traditional industrial sense.

It is ecosystem-based integration:

- energy systems enable compute ecosystems

- compute ecosystems enable platform ecosystems

- platform ecosystems generate capital flows

- capital flows reinforce infrastructure expansion

Increasingly, platforms also operate as monetary layers within the system:

- controlling payment flows

- shaping digital transaction environments

- influencing currency usage and capital circulation

Platforms do not simply intermediate economic activity.

They increasingly define the terms under which value is created, exchanged, and retained.

Platform power is ecosystem power expressed at scale — and increasingly, monetary power.

This is not firm-level competition.

It is competition between integrated systems.

→ See:

Digital Sovereignty

Reading Map SME Innovation

Networks Digital

Economy: Platforms and Currencies

VII. Europe: Demand Without Control

Europe participates in this system primarily as:

a consumer of platforms

a host of demand

a regulatory actor

But not as:

a controller of compute infrastructure

a leader in semiconductor design

a coordinator of capital at comparable scale

This produces a structural imbalance:

costs are imported

value is externalised

capital formation weakens

→ See:

Europe’s

Challenge

EU

Asymmetry Under Stress

VIII. The Alternative: Architecture, Not Protectionism

The strategic question for Europe is not replication.

It is architecture.

Possible pathways include:

decentralised energy systems

localised compute deployment

SME-integrated digital ecosystems

hybrid cloud–edge infrastructure

Sovereignty emerges from system design, not policy declaration

→ See:

EU

Energy Paradigm Shift — Part I

Strategic Autonomy Without Illusions (planned)

IX. Investor Implications

Where value accrues:

energy-abundant systems

semiconductor control points

hyperscale compute infrastructure

integrated platform ecosystems

Where value leaks:

high-cost energy regions

systems without compute ownership

fragmented capital environments

Where opportunity emerges:

energy–compute integration

infrastructure deployment

regional system nodes

hybrid and decentralised architectures

→ See:

- Investor

Framework - Capital Allocation in an Energy-Bound System

X. Conclusion

The dominance of the US MAG7 is not accidental.

It is the outcome of a system in which:

energy

compute

semiconductors

capital

and global value chains

are aligned.

Power in the AI era does not reside in software alone.

It resides in the system that sustains it.