Energy Geopolitics & Global Shift

Why Decarbonisation Must Become a Competitiveness Strategy; the Decisive Global Race: Fossil-Fuel Incumbency vs. Renewable Electrification

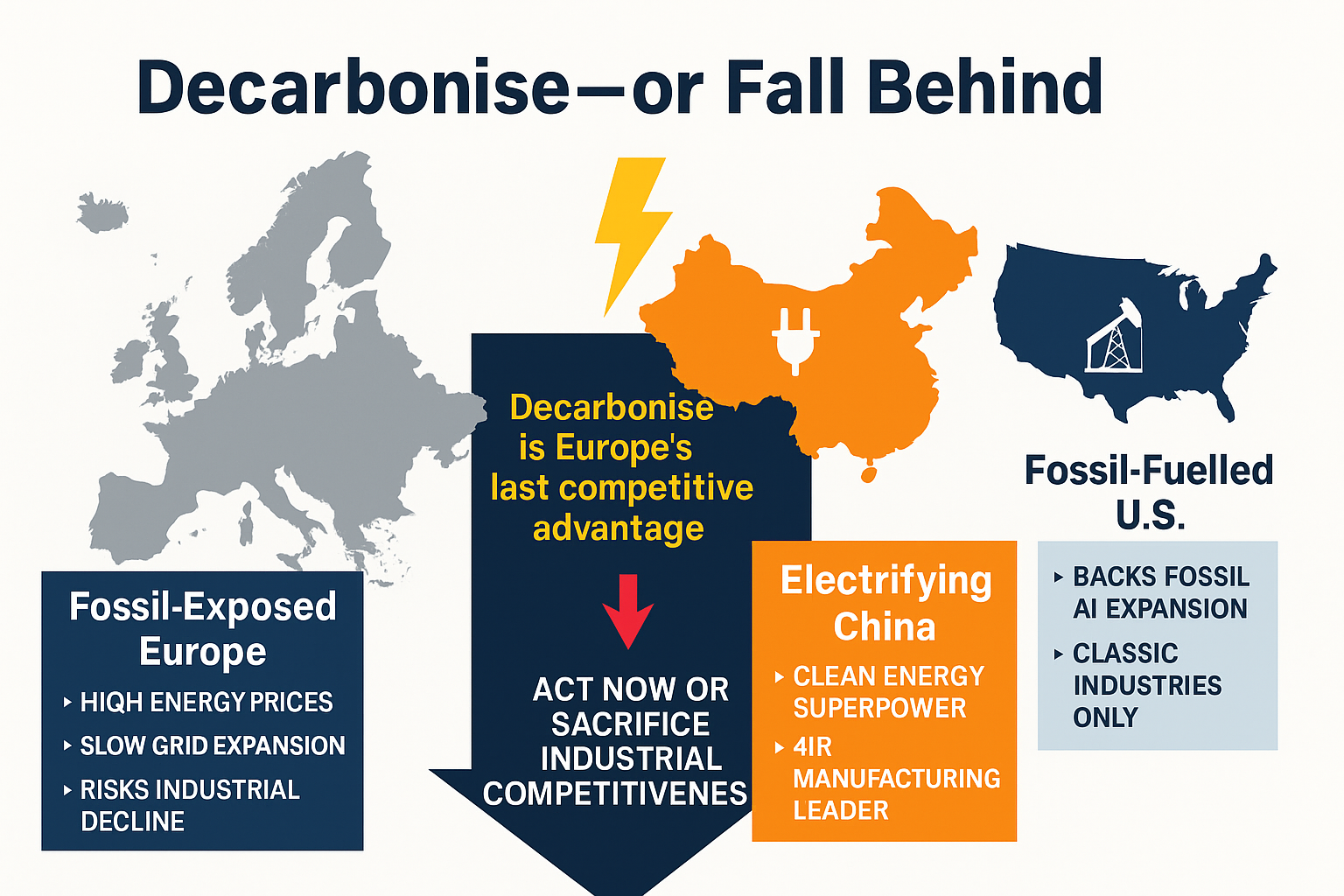

The global energy transition is no longer about climate commitments—it is an industrial and geopolitical race. The decisive divide is between fossil-fuel incumbency and renewable electrification, and it is now shaping economic power, technological leadership, and geopolitical influence. The critical question is not who pledges net-zero, but who builds an electrified industrial system fast enough to dominate the next economic cycle.

China has moved decisively. It is becoming an electrostate—scaling solar, batteries, EVs, and grids at unprecedented speed, hitting renewable targets early, and exporting cleantech across the Global South. Its model tightly integrates industrial policy, manufacturing scale, and cheap clean energy, creating a powerful competitiveness loop. The United States is responding through the Inflation Reduction Act, but remains structurally anchored to fossil fuels, particularly to power AI, defence, and heavy industry.

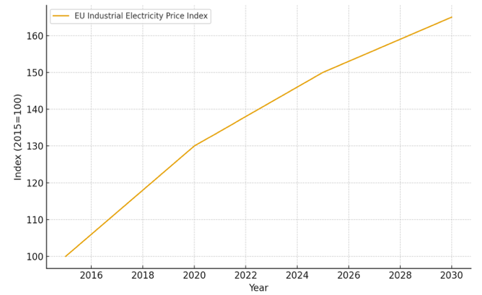

Europe sits between these paths—and is losing ground. High energy prices, ageing grids, slow permitting, and fragmented markets are eroding industrial competitiveness. If Europe follows a U.S.-style fossil-powered model, it will lock in high costs and import dependence. If it fails to match China’s pace of electrification, it will forfeit the industries of the future.

The Global South reflects this shift. Falling renewable costs create a once-in-a-century opportunity to leapfrog fossil dependence, enabling energy sovereignty and industrial development without the constraints of legacy infrastructure. China’s cleantech exports are accelerating this transition, extending its influence across emerging markets.

The strategic reality is clear: decarbonisation is no longer climate policy—it is a cost, security, and competitiveness strategy. Clean power is now structurally cheaper than fossil energy. Electrification reduces total energy demand, strengthens industrial resilience, and rewards early movers through scale and network effects. Countries that electrify fastest will control manufacturing, AI infrastructure, and the next industrial order.

For Europe, time is the binding constraint. Decarbonisation is Europe’s last major structural advantage—but only if it is pursued at scale and speed. Grid modernisation, rapid renewable deployment, storage, and an integrated industrial strategy are no longer optional. The energy transition has become a contest for power, prosperity, and sovereignty—and Europe must act now or accept strategic decline.

Part one of a three-article series on Europe’s strategic future in energy, AI, and the Fourth Industrial Revolution.

1. Introduction — The New Energy Divide

The global energy transition is no longer a matter of climate diplomacy, symbolic targets, or moral imperatives. It has become the defining strategic confrontation of the 21st century: a systemic contest between two opposing energy–industrial models. On one side stand the fossil-fuel incumbents, led primarily by the United States, whose economic, military, and technological ecosystems remain structurally tied to hydrocarbons. On the other side rises a new paradigm—renewable electrification—driven at unprecedented speed by China’s coordinated industrial expansion.

This clash is not abstract. It is reorganizing global power, reshaping trade structures, and determining which nations will dominate the next technological era. The winner will not be the country with the most ambitious climate pledges—but the one capable of deploying clean energy systems at scale, integrating AI into electrified infrastructures, and securing control over the critical technologies of the Fourth Industrial Revolution.

Caught between these two models, Europe is approaching a historic inflection point. For decades, the EU attempted to balance environmental leadership with industrial competitiveness. Today, that balance is breaking. Rising energy costs, shrinking industrial output, and dependency on foreign fossil imports threaten the continent’s economic future. Meanwhile, AI’s exploding electricity demand is colliding with Europe’s fragile grids, creating a strategic dilemma:

If Europe attempts to follow a U.S.-style AI expansion powered by fossil-heavy energy systems, it will destroy its own competitiveness, deepen deindustrialization, and lock itself into permanent dependency.

Europe cannot build a future on another nations’s energy model—especially one fundamentally misaligned with its resources, infrastructure, and geopolitical constraints.

Instead, the only viable path for long-term competitiveness is clear: A rapid, massive acceleration of renewable electrification, grid modernization, and energy sovereignty.

Anything less would leave Europe stranded between two industrial giants, without the power base needed to remain a global actor.

2. The U.S. Petrostate Model — Why It Works for America but Would Break Europe

The United States presents itself as a leader in the clean-energy race, especially after passing the Inflation Reduction Act (IRA). In reality, the U.S. remains a hybrid petrostate, structurally anchored to hydrocarbons even as it subsidizes renewables. This duality is not a contradiction—it is the foundation of American power.

The U.S. today is the world’s largest producer of oil and gas, a position strengthened by shale, LNG exports, and a vast domestic fossil ecosystem. This fossil abundance underpins the entire U.S. economic structure:

- low industrial energy prices

- global LNG leverage

- an enormous military-industrial complex almost entirely dependent on fossil fuels

- a political economy shaped by petroleum-producing states

- a cultural and infrastructural bias toward the combustion engine

Nothing in Europe resembles this system. The U.S. energy system can absorb huge electricity shocks—data centers, crypto mining, AI clusters—because it can rapidly increase fossil output. When demand rises, America burns more gas. When prices rise, it subsidizes consumers. When infrastructure strains, it builds more fossil capacity.

Regardless of public messaging, the U.S. pathway is electrification on top of hydrocarbons, not electrification replacing hydrocarbons. For the United States, this hybrid model works. For Europe, it would be catastrophic.

Why the U.S. model is structurally incompatible with Europe:

- Europe has no domestic fossil abundance to sustain high energy consumption.

- Europe already suffers from the world’s highest industrial energy costs.

- Europe relies heavily on imported LNG, primarily from the U.S. at premium prices.

- Europe’s industrial base cannot survive volatile fossil markets.

- Europe lacks political appetite and physical space for U.S.-style energy expansion.

- Europe’s population is aging and shrinking, reducing economic resilience.

If Europe adopts a U.S.-style AI strategy—compute-intensive, fossil-backed, centralized in hyperscale data clusters—it will choke on energy costs, lose industrial competitiveness, and fall deeper into deindustrialization.

What works for a petrostate destroys a fossil-poor continent.

3. China the Electrostate — Scale, Coordination, and Global Influence

While the U.S. anchors its technological future to hydrocarbons, China has embraced a radically different paradigm: electrification as the core of national power. This is not green idealism—it is industrial strategy.

China reached its 2030 renewable energy targets six years ahead of schedule, installing renewable capacity on a scale the world has never seen:

- Gigafactories dominating global battery supply

- World-leading solar and wind manufacturing

- Massive electrification of transport (EVs, buses, logistics)

- Deep industrial policy integration across provinces

- Coordinated AI deployment powered by domestic clean energy

China’s cleantech ecosystem now accounts for roughly 9% of GDP, expanding at ~30% year-on-year. This industrial juggernaut allows China to:

- export affordable clean technologies

- reshape development models across the Global South

- reduce global oil demand by electrifying transport at home

- control supply chains for critical minerals, batteries, and solar

Where the U.S. builds influence through fossil exports and security alliances, China builds it through renewable hardware, electrification systems, and AI-enabled industrial platforms. Crucially, China’s energy strategy directly supports its AI ambitions. Unlike Europe and the U.S., where AI drives energy demand faster than supply can expand, China expands both simultaneously:

- more renewables > more electricity > more compute > more industrial capacity.

Electrification is not a by-product of China’s rise—it is its engine.

4. Europe’s Strategic Dilemma — Between Petrostate America and Electrostate China

Europe sits between two incompatible superpower models:

- The U.S. petrostate model, anchored to fossil abundance and combustible engines

- China’s electrostate model, built on electrification, industrial policy, and scale

Neither model can simply be copied.

Europe must build its own.

But at present, Europe is drifting dangerously toward the wrong one: a U.S.-style AI ecosystem powered by imported LNG and fossil-heavy grids.

This would be an economic suicide pact.

Europe cannot run a U.S.-style AI economy.

Because:

- Energy costs:

Europe pays 2–4x more for electricity than the U.S.

AI is now one of the most electricity-hungry technologies ever created.

Running U.S.-style hyperscale AI clusters on Europe’s grid would bankrupt industries. - Structural energy dependency:

Europe relies heavily on imported fossil fuels—especially U.S. LNG.

America profits when Europe burns gas; Europe loses competitiveness every time. - Geopolitical fragility:

The 2022 energy shock revealed the truth:

Europe cannot be prosperous if it remains fossil-dependent. - Infrastructure mismatch:

AI demand is exploding.

Renewable expansion is lagging.

The grid is aging.

Data centers are already straining local networks. - Deindustrialization:

With every year of high fossil-based energy prices, Europe’s industrial heartlands—Germany, Italy, France, Belgium, Czechia—decline further.

Following the U.S. model is not just unsustainable.

It directly contradicts Europe’s structural realities.

Europe must choose electrification over combustion, or it will become economically irrelevant.

Europe’s unique position

Europe’s advantage—its only durable advantage—lies in:

- institutional trust

- regulatory strength

- technological governance

- early adoption of renewable energy

- human-centric digital policy

- energy efficiency leadership

- scientific research networks

But these strengths can only translate into competitiveness if Europe is powered by:

- abundant renewable electricity

- modernized grids

- decentralized energy systems

- efficient electrified industries

- AI running on clean, sovereign compute infrastructure

Europe cannot innovate if it cannot power its innovations.

5. AI’s Energy Crisis — and Why Europe Cannot Ignore It

The next technological revolution—AI, automation, robotics, cloud-edge systems—depends entirely on electricity. Not data. Not algorithms. Electricity.

The IEA now projects that by 2030:

U.S. data centers alone will consume more electricity than aluminium, steel, cement, chemicals, and other heavy industries combined.

And this is just the beginning.

AI is catalyzing a new global energy order.

The U.S. response?

Burn more gas.

Ramp up LNG exports.

Expand transmission where profitable.

Double down on fossil-backed compute.

China’s response?

Accelerate renewables.

Expand nuclear.

Deploy AI to optimize grid performance.

Integrate electrification with industrial policy.

Europe’s response?

None of the above—yet.

And that is the problem.

Europe’s grids are aging.

Its renewable deployment is insufficient.

Its industrial base is shrinking.

Its AI capacity is dependent on foreign cloud giants.

Its energy strategy is fragmented between member states.

Europe today faces an acute dilemma:

AI is essential for competitiveness—but AI requires massive electricity Europe does not yet have.

If Europe powers AI with LNG, it will:

- deepen dependency on U.S. hydrocarbons

- maintain high industrial energy costs

- undermine climate commitments

- push industries to relocate

- accelerate deindustrialization

- lock itself into a fossil-based energy trap

If Europe powers AI with renewables, it will:

- reduce long-term system costs

- increase energy sovereignty

- remain competitive with China

- reduce dependency on the U.S.

- stabilize electricity prices

- enable industrial electrification

- strengthen grid resilience

The choice is binary.

There is no middle path.

6. Deployment Speed — The Real Decider of Power

The world is no longer competing on who invents clean

technology.

It is competing on who deploys it fastest.

This is the “time value of carbon,” as Danny Kennedy describes:

The sooner emissions fall, the greater a nation’s long-term competitiveness and energy security.

China’s approach:

- Deploy now.

- Scale relentlessly.

- Learn by doing.

- Drive down costs through volume.

- Export to the Global South.

China installed 217 GW of solar and 76 GW of wind in a single year—more than the entire U.S. grid additions over the last several years combined.

China is deploying renewables fast enough to theoretically replace the world’s entire electricity system within two decades

Europe’s approach:

- High ambition

- Slow execution

- Regulatory bottlenecks

- Local resistance

- Long permitting timelines

- Fragmented energy markets

Europe has the vision, the ethics, the technology—but not the speed.

The U.S. approach:

The IRA is accelerating deployment—but fossil dependency dilutes the long-term competitiveness of the American strategy. The U.S. is innovating faster than China but deploying far slower.

In this global race:

- China wins on scale

- The U.S. wins on software innovation

- Europe wins on governance and trust

But only China’s model currently aligns energy, industry, AI, and national strategy into a unified system.

Europe must learn from this—not copy it, but adapt its logic.

7. The Economics of Electrification — Decarbonization as Europe’s Competitiveness Strategy

The debate around decarbonization is often framed—wrongly—as moral,

ideological, or environmental.

In reality, decarbonization is a hard-edged economic

strategy.

Renewable electrification is now the cheapest path to:

- energy security

- industrial competitiveness

- technological sovereignty

- geopolitical resilience

The numbers are unequivocal.

OpenSolar modelling projects that by 2035:

- Solar alone could supply over 50% of global energy demand

- Electrification could reduce global energy consumption by ~60%

- Annual global savings could reach US$9 trillion

These numbers are not speculative—they follow observed cost curves and learning rates in renewable technology.

Think of it this way:

- Fossil systems waste 60–70% of energy as heat.

- Renewable-electric systems waste virtually none.

- Electrified transport and industry are 3–5x more efficient.

Europe, which suffers from chronic structural energy scarcity, has the most to gain from this transition.

Europe’s competitiveness is collapsing because energy remains expensive.

In contrast:

- China is reducing system-level energy costs every year.

- The U.S. can keep costs lower because it produces fossil fuels.

- Europe imports everything—and pays the global price.

This is why Europe must choose electrification:

it is the only pathway where Europe can produce abundant, cheap,

domestic energy at scale.

Fossil fuels cannot do this for Europe.

They can only do it for America.

8. Europe’s Strategic Imperative — Electrify or Deindustrialize

This is the most important part of the analysis.

Europe today faces a stark and unavoidable binary:

A) Follow the U.S. petro-AI model

and Europe will lock itself into:

- a fossil-based, LNG-dependent energy system

- permanently high electricity and manufacturing costs

- increasing reliance on U.S. tech giants

- declining industrial competitiveness

- accelerated offshoring of industry

- shrinking workforce and rising welfare burdens

- deep strategic dependence on Washington

This path leads directly to European deindustrialization.

There is no world in which Europe thrives by powering AI and industry with expensive imported gas.

B) Build a European electrostate model (without copying China)

This means:

- rapid, large-scale deployment of renewables

- grid modernization

- digitalized, AI-optimized energy systems

- electrification of industry and transport

- European-owned cloud, compute, and AI infrastructure

- trusted data governance

- European-made batteries, solar, semiconductors, and power electronics

This is the only model consistent with:

- Europe’s geography

- Europe’s economy

- Europe’s political identity

- Europe’s social contract

- Europe’s climate goals

And it is the only model that allows Europe to remain a global power.

The core message:

Europe cannot afford to copy the U.S. because Europe is not

the U.S.

It has no cheap fossil abundance.

Its wealth depends on efficiency, not extraction.

Europe’s prosperity is impossible without full

decarbonization.

Europe must decouple its economy from fossil inputs if it wants to remain competitive.

This is not ideology.

This is arithmetic.

9. The Global South — The New Center of Energy Geopolitics

The world’s future energy geography will not be decided in Washington, Brussels, or Beijing—but in the Global South, where population and energy demand are growing fastest.

The race is already evident: rise of

distributed/microgrid systems vs stagnant centralized output.

China understands this.

The U.S. increasingly understands this.

Europe has not yet acted accordingly.

Why the Global South matters:

- 100+ countries will electrify without repeating the

fossil-fuel era

They will leapfrog directly to renewables and decentralized systems. - China already dominates these markets

Through cleantech exports, infrastructure investment, and concessional financing. - Europe is losing influence

Because it has not made clean energy central to its development partnerships. - The next global economic system will be built through energy

diplomacy

The countries supplying electrification—solar, batteries, grids, microgrids—will shape the political and technological norms of the century.

China does this aggressively.

The U.S. does this selectively.

Europe does this timidly.

Why this matters for Europe’s competitiveness

Europe cannot remain a global standard-setter if:

- China sets the energy norms

- The U.S. sets the AI norms

- The Global South becomes the new manufacturing ecosystem for clean technology

- And Europe remains in the middle, regulating while others industrialize

Europe’s leverage rests on:

- trusted governance

- high-quality standards

- renewable energy diplomacy

- green industrial partnerships

- supporting sovereign energy systems in developing nations

If Europe ignores this, it will be sidelined.

If Europe leads it, it becomes indispensable.

10. Conclusion — Europe’s Last Chance at Competitiveness

We are in a global struggle to define the energy and industrial architecture of the 21st century.

Three competing models are crystallizing:

- China: scale + coordination > the electrostate

- United States: innovation + market dynamism > the petro-AI hybrid

- European Union: governance + trust > but lacking speed and scale

Europe must choose now.

And it must choose correctly.

If Europe chooses a U.S.-style fossil-powered AI economy:

It will permanently cripple its competitiveness.

It will trap itself in fossil dependency.

It will accelerate deindustrialization.

It will become strategically subordinate to Washington.

It will lose the energy and AI races simultaneously.

If Europe chooses large-scale renewable electrification:

It can rebuild industrial sovereignty.

It can stabilize energy prices.

It can power AI domestically.

It can compete with China.

It can lead global standards.

It can anchor the Global South in equitable development

partnerships.

It can defend its prosperity in a turbulent geopolitical landscape.

The truth is simple:

Decarbonization is not a climate project.

It is Europe’s survival strategy.

Electrification is not an environmental choice.

It is the foundation of future competitiveness.

Europe must decarbonize to remain a global power.

REFERENCES

- IEA — World Energy Outlook 2023

- IEA–World Energy Outlook 2024

- IEA — Electricity 2024

- REN21 — Renewables Global Status Report 2024

- BloombergNEF — New Energy Outlook

- IRENA — Renewable Capacity Statistics 2023

- China National Energy Administration (NEA)

- IRENA — China Country Profile

- U.S. EIA — Annual Energy Outlook 2024

- U.S. DOE — Transmission Needs Study 2023

- CNBC — U.S. power demand & data centers

- Critical Technology Competition

- ITIF — Global Tech Tracker 2025

- OECD — Digital Economy Papers

#EnergyTransition #Electrification #Decarbonisation #Renewables #GeopoliticsOfEnergy #GlobalOrder #IndustrialStrategy #AI #Cloud #DigitalSovereignty #AIEthics #SmartTech #DataGovernance #EUSovereignty #TechGeopolitics #4IR #FutureOfIndustry #EnergySecurity #NetZero #EUCompetitiveness

Suggested Reading

- Global Energy Paradigm Shift

- Energy Sovereignty as System Control (EU Sovereignty)

- Industrial Power Post-Globalisation (Security)

- Africa & Eurasia Energy Overlays (Global)