Cloud Dependency and the Missing Compute Layer

Why Digital Sovereignty Begins Below the Cloud

A Reference Guide within TechWar

The debate surrounding digital sovereignty is becoming increasingly prominent across Europe.

Governments discuss sovereign cloud providers, European AI models, data localisation requirements, cybersecurity frameworks, and alternatives to foreign software platforms. New datacentres are announced. Investment strategies increasingly focus on digital infrastructure. Policymakers seek ways to reduce dependence upon external technology providers.

These concerns are legitimate.

Yet they frequently begin at the wrong layer of the system.

Digital sovereignty is often treated as a software problem.

Increasingly it is becoming an infrastructure problem.

As artificial intelligence scales and computation becomes embedded throughout economic systems, sovereignty questions migrate downward through the stack. The critical issue is no longer simply who owns the software.

It is increasingly who controls the infrastructure, energy systems, semiconductor ecosystems, compute architectures, developer ecosystems, and capital structures upon which software depends.

Digital sovereignty increasingly begins below the cloud.

I. The Digital Sovereignty Debate and the Wrong Layer of the System

Much of the contemporary debate focuses on visible interfaces.

Cloud providers.

Software platforms.

AI applications.

Data governance.

Cybersecurity.

These layers matter because they shape access, governance, and control.

Yet they sit near the top of a deeper architecture.

Beneath applications lies cloud infrastructure.

Beneath cloud infrastructure lies compute.

Beneath compute lies semiconductor capability.

Beneath semiconductor capability lies infrastructure, industrial ecosystems, and energy systems.

The deeper layers increasingly determine the possibilities available to the higher layers.

As AI becomes embedded throughout economies, sovereignty questions increasingly move downward through the system.

The debate therefore shifts from software ownership toward infrastructure control.

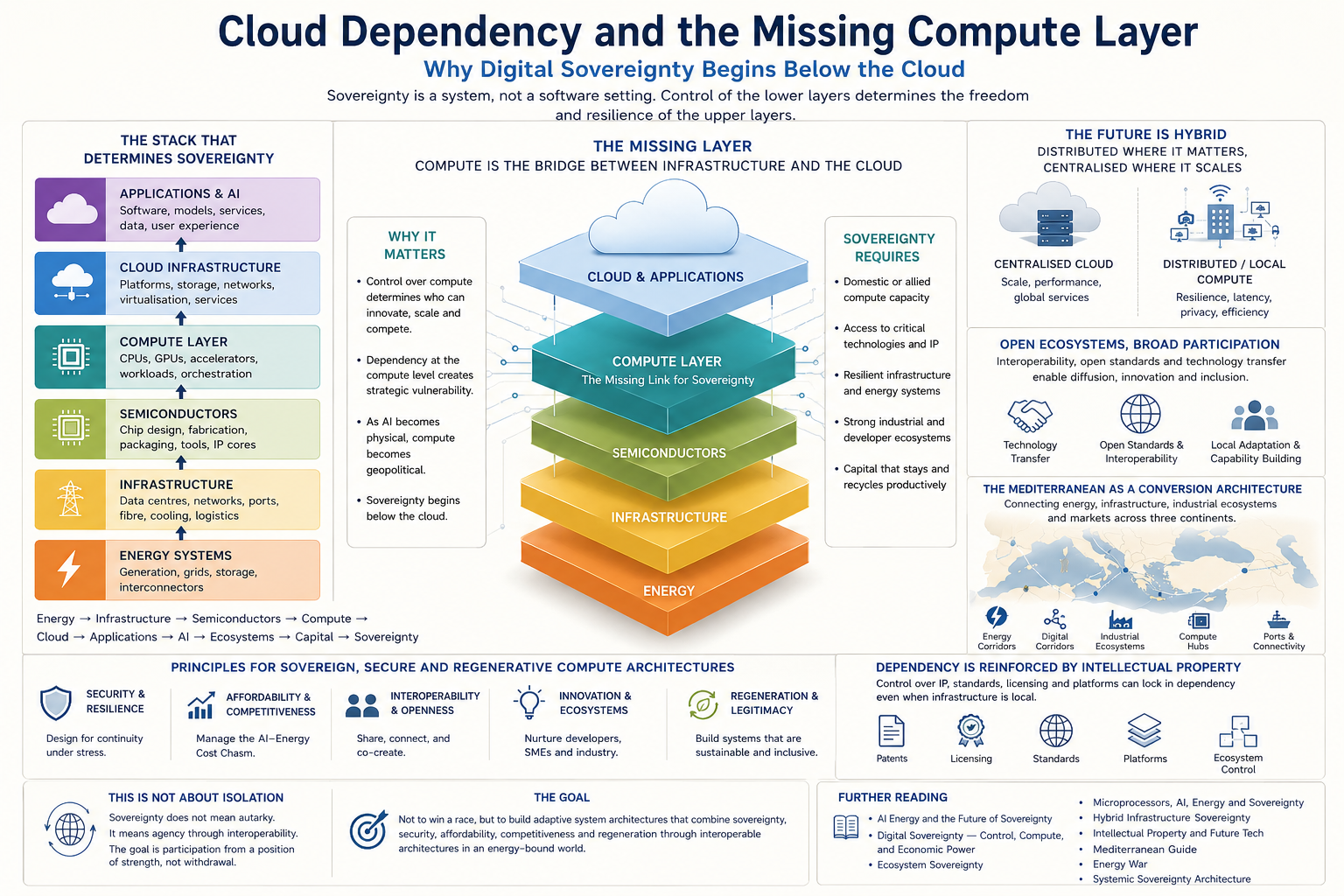

II. The Missing Compute Layer

The modern digital economy is often presented as a software economy.

Yet software ultimately runs on physical systems.

The emerging architecture increasingly resembles:

Energy

↓

Infrastructure

↓

Semiconductors

↓

Compute

↓

Cloud

↓

Applications

↓

Artificial Intelligence

Each layer depends upon the successful operation of the layer beneath it.

Applications cannot function without cloud infrastructure.

Cloud infrastructure cannot function without compute.

Compute cannot function without semiconductors.

Semiconductor ecosystems cannot scale without infrastructure and energy systems.

As AI expands, the lower layers become progressively more important.

This transformation explains why energy systems, industrial ecosystems, semiconductor supply chains, infrastructure investment, and compute capacity increasingly shape geopolitical competition.

The digital economy is becoming more physical rather than less.

III. AI Has Become Physical

Artificial intelligence is often described as a software revolution.

Increasingly it resembles an infrastructure revolution.

Training and deploying advanced AI systems requires electricity, compute capacity, cooling systems, specialised semiconductors, transmission infrastructure, datacentres, and large-scale capital investment.

This transformation creates the AI–Energy Cost Chasm.

The value generated by AI increasingly depends upon physical systems whose expansion remains constrained by:

energy availability

infrastructure deployment

industrial capacity

permitting

ecosystem density

capital expenditure

AI therefore becomes inseparable from infrastructure.

Competition increasingly becomes competition for conversion capacity: the ability to transform energy into infrastructure, infrastructure into compute, compute into ecosystems, ecosystems into capital formation, and capital formation into sovereignty.

IV. Why Cloud Concentration Emerged

The rise of hyperscale cloud providers was not accidental.

Cloud concentration emerged because centralised infrastructure delivered powerful economic advantages.

Large datacentres offered economies of scale, utilisation efficiency, software standardisation, capital concentration, and global deployment capability.

These advantages enabled extraordinary growth.

Cloud infrastructure became one of the defining architectures of the digital era.

Yet centralisation also concentrated control.

The same systems that improved efficiency increasingly concentrated influence over:

compute infrastructure

developer ecosystems

standards

data flows

capital formation

Cloud concentration therefore became not merely a technological phenomenon, but an increasingly geopolitical one.

V. Security, Resilience, and the Limits of Centralisation

Security and resilience are not identical.

A highly centralised system may be secure yet fragile.

A disruption affecting a small number of critical nodes can create systemic consequences across entire networks.

As AI becomes embedded throughout economic systems, resilience increasingly becomes a strategic variable.

This creates a growing tension.

Large-scale datacentres can improve efficiency and capability.

Yet they can also increase:

infrastructure concentration

energy demand concentration

grid dependency

capital concentration

The challenge is therefore not simply how to secure systems.

It is how to create systems capable of remaining functional under constraint.

Increasingly this points toward hybrid architectures combining centralised capability with distributed resilience.

VI. The Return of Compute Locality

While hyperscale cloud continues to expand, a parallel trend is emerging.

Computation is increasingly moving closer to users, devices, factories, vehicles, infrastructure systems, and industrial processes.

This shift reflects both technological and economic realities.

Latency constraints, privacy requirements, resilience considerations, transmission costs, and improvements in semiconductor efficiency increasingly favour local processing.

Apple provides one of the clearest examples.

Rather than relying exclusively upon remote cloud infrastructure, Apple increasingly emphasises:

specialised silicon

on-device AI

integrated hardware and software design

energy-efficient processing

local computation

The significance extends far beyond consumer electronics.

Apple demonstrates how sovereignty, resilience, efficiency, and ecosystem control can increasingly emerge through distributed compute architectures.

The future is unlikely to be exclusively centralised or exclusively distributed.

Increasingly it appears hybrid.

VII. Open Ecosystems, Technology Diffusion, and the Next Phase of AI

The future of compute is unlikely to be determined solely by proprietary systems.

Alongside hyperscale cloud architectures, many countries increasingly pursue models based upon interoperability, technology diffusion, local capability development, and open ecosystem participation.

China and India have frequently placed greater emphasis upon technology transfer, domestic capability accumulation, local adaptation, and ecosystem development than on simple consumption of imported technologies.

As artificial intelligence expands beyond datacentres into:

factories

logistics networks

energy systems

agriculture

healthcare

industrial production

smart cities

interoperability becomes increasingly important.

The challenge is not merely controlling technology.

It is ensuring that technology can diffuse throughout the wider economy.

This distinction is critical.

A highly secure system that remains inaccessible, unaffordable, or disconnected from productive ecosystems may strengthen dependency rather than reduce it.

The objective is therefore not technological isolation.

It is the creation of interoperable architectures capable of combining security, resilience, affordability, innovation, and broad participation.

VIII. Cloud Sovereignty Is Not Compute Sovereignty

A country may host datacentres while remaining dependent upon foreign semiconductor ecosystems.

It may operate cloud services while relying upon foreign compute architectures.

It may possess software capability while depending upon intellectual property, licensing regimes, operating systems, developer frameworks, and standards controlled elsewhere.

Sovereignty therefore extends beyond physical infrastructure.

Control over intellectual property can influence who captures value, who sets standards, who controls technological evolution, and who accumulates capital from ecosystem participation.

Infrastructure dependency and intellectual property dependency increasingly reinforce one another across the digital economy.

IX. Compute Sovereignty as Ecosystem Sovereignty

Compute does not exist in isolation.

It emerges from ecosystems.

Energy systems, semiconductor supply chains, cloud infrastructure, operating systems, developer communities, industrial ecosystems, and capital formation increasingly function as interconnected architectures.

This is why ecosystem sovereignty increasingly becomes more important than isolated technological capability.

The competition is no longer simply between technologies.

Increasingly it occurs between ecosystem architectures capable of coordinating multiple layers simultaneously.

Ecosystem control increasingly extends beyond infrastructure ownership.

It also includes standards, developer communities, operating systems, software frameworks, intellectual property portfolios, and licensing structures that shape participation within the wider ecosystem.

This is one reason why technological capability alone does not automatically produce sovereignty.

The ability to generate, retain, diffuse, and capture value from knowledge increasingly becomes part of the sovereignty equation.

X. Europe’s Missing Conversion Layer

Europe possesses many of the individual components required for competitiveness.

It retains industrial capability, engineering expertise, research institutions, infrastructure assets, and specialised manufacturing ecosystems.

Yet capability does not automatically produce sovereignty.

The challenge increasingly lies in conversion.

Can energy systems be converted into competitive compute?

Can compute be converted into ecosystem density?

Can ecosystem density be converted into capital formation?

Can capital formation be retained within productive systems?

Europe’s challenge increasingly resembles a conversion challenge rather than a capability challenge.

XI. Compute Geography, the Mediterranean, and Regeneration

As AI becomes physical, compute increasingly follows infrastructure.

Energy availability, transmission networks, interconnectors, ports, fibre corridors, logistics systems, and industrial ecosystems all influence where future compute capacity emerges.

This creates new opportunities for regions positioned at the intersection of multiple systems.

The Mediterranean increasingly occupies such a position.

Its significance extends beyond geography.

It increasingly functions as a potential conversion architecture linking:

energy systems

infrastructure corridors

industrial ecosystems

European demand

emerging compute networks

The objective is not merely technological competitiveness.

It is regeneration.

The combination of distributed energy, local compute, industrial ecosystems, infrastructure investment, and regional connectivity creates opportunities for economic renewal, productive participation, and strategic agency.

XII. From Digital Sovereignty to System Sovereignty

The digital sovereignty debate remains important.

Yet the emergence of AI increasingly pushes the debate deeper into the system.

The central question is no longer:

Who owns the software?

Increasingly it becomes:

Who controls the energy systems, infrastructure networks, semiconductor ecosystems, compute architectures, developer ecosystems, and capital structures upon which software depends?

As AI becomes physical, sovereignty becomes infrastructural.

As infrastructure becomes strategic, compute becomes geopolitical.

As compute becomes geopolitical, digital sovereignty increasingly begins below the cloud.

Ultimately sovereignty propagates through a structured chain:

Energy → Infrastructure → Compute → Ecosystems → Capital → Sovereignty

Control of the lower layers increasingly determines the possibilities available to the higher layers.

The emerging competition is therefore not simply technological.

It is a competition between system architectures capable of combining interoperability, resilience, affordability, security, innovation, participation, and agency.

The objective is not technological isolation.

Nor is it winning a race.

The objective is the construction of adaptive system architectures capable of sustaining sovereignty, competitiveness, and regeneration within an increasingly energy-bound world.

Further Reading

Foundations

Compute and Sovereignty

Ecosystems and Capability

Regional Architectures