Systemic Asymmetry in the Emerging G2 Order

Keynote

Periods of stress do not merely disrupt systems; they reveal them. As energy constraints tighten, supply chains fragment, and financial conditions harden, structural asymmetries that were previously obscured by global integration become visible and consequential. In the emerging G2 order, these stresses expose not a balance between comparable powers, but a divergence between structurally unequal systems. This article examines how stress functions as a diagnostic force in global competition—revealing differences in resilience, coordination capacity, and shock absorption—and why power increasingly accrues to systems that can transmit pressure outward rather than absorb it internally.

- Energy-Bound

System

- System Re-Concentration

- Systemic Asymmetry Cross Panel Index ### Preface — Stress as Exposure

For much of the post–Cold War era, global integration masked structural imbalance. Open trade, liquid finance, and institutional coordination softened the visible consequences of unequal energy endowments, industrial depth, and financial capacity. Stress was treated as episodic, and recovery as a return to equilibrium.

That buffering effect has eroded.

In an energy-bound and fragmented global system, stress no longer dissipates. It accumulates. Energy price shocks, monetary tightening, supply disruptions, and technological rivalry now interact, revealing which systems can absorb volatility and which convert it into internal instability. Political backlash, inflation persistence, and strategic overreach are not anomalies; they are symptoms of exposure.

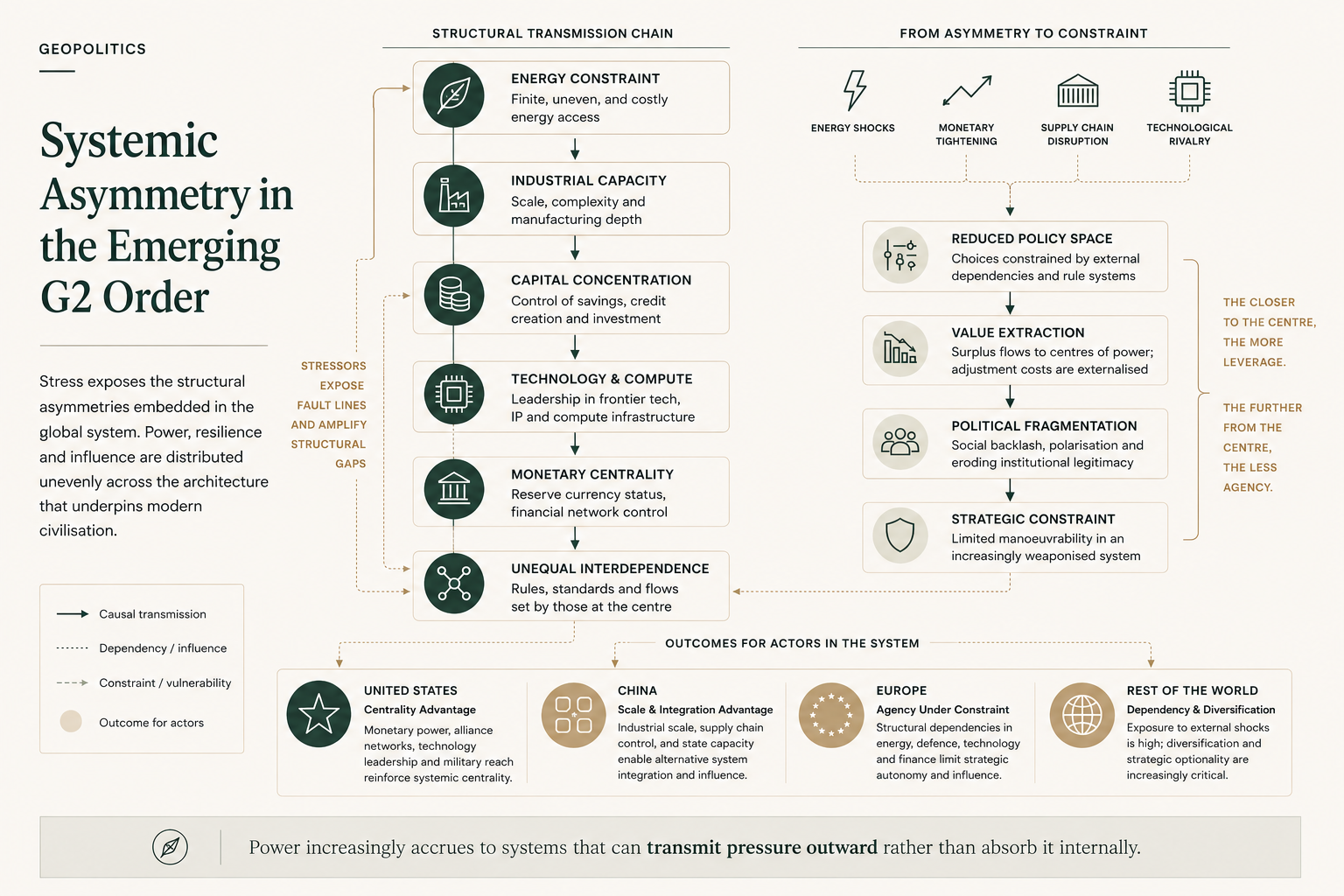

In the emerging G2 order, this exposure is uneven. The United States and China are not symmetrical rivals differentiated primarily by ideology or alignment, but structurally distinct systems with divergent energy profiles, industrial architectures, financial transmission mechanisms, and coordination capacities. Stress reveals these differences more clearly than growth ever did.

This article focuses on how stress operates across competing systems rather than who is to blame. It examines the mechanisms through which pressure propagates across energy, finance, trade, and technology—and how systemic asymmetry becomes decisive when systems are forced beyond their design limits..

Inequality, ideology, and the breakdown of shared growth

Asymmetry is often treated as a moral or political problem: inequality, unfairness, domination, or exploitation. This framing is incomplete. Asymmetry is a structural feature of all economic and political systems, and in many cases it is a precondition for exchange, coordination, and growth.

What matters is not whether asymmetry exists, but what kind of dynamics it produces.

In periods of expansion, asymmetry can underpin shared development. Differences in capacity, capital, and power allow systems to scale, risks to be pooled, and productivity gains to diffuse. Under these conditions, inequality is often tolerated because the system delivers rising returns and broad-based improvement.

When underlying system conditions change, however, asymmetry can invert. Exchange that once generated growth begins to extract value. Returns concentrate, adjustment costs are displaced, and dependence deepens without corresponding gains in productive capacity. Inequality becomes politically salient not because norms have shifted, but because the system no longer compensates for imbalance.

The present phase of ideological polarisation, social fragmentation, and institutional strain reflects this transition. It is not primarily a crisis of beliefs or governance. It is the manifestation of systemic asymmetry in an environment where energy, industrial, and technological constraints have tightened simultaneously.

From this perspective, the growing dominance of certain economies within advanced blocs, the erosion of cohesion among allies, and the internal strain on integration projects are not anomalies. They are predictable outcomes of asymmetric exchange operating under new material conditions.

As explored in The Global Energy Paradigm Shift, the tightening of energy, industrial, and infrastructural constraints reshapes how value is generated and distributed; systemic asymmetry is the social and ideological expression of that underlying shift.

The sections that follow examine how this dynamic has shifted from an engine of post-war growth to a source of extraction, diminishing returns, and political instability.

How Power Is Structured Before It Is Contested

I. The End of Symmetric Globalisation

For much of the late twentieth century, globalisation was widely understood as a process of convergence. Trade liberalisation, capital mobility, technological diffusion, and institutional integration were expected to reduce disparities over time. While inequalities persisted, the underlying assumption was that participation in global markets would gradually align productivity, income, and influence.

That assumption no longer holds.

The emerging global order — increasingly described as a G2 system centred on the United States and China — is not producing convergence. It is producing persistent, structural asymmetry. Power is accumulating unevenly across technology, finance, infrastructure, and governance, reinforcing hierarchy rather than flattening it.

This asymmetry is not the result of policy failure or incomplete integration. It is the structural outcome of how the contemporary global system is organised.

II. Asymmetry is not a failure, it is a feature

Global economic systems have never been symmetrical, and no serious analysis should pretend otherwise. Geography, scale, technology, and timing inevitably produce hierarchies. The critical question is therefore not whether imbalance exists, but how it is managed and where adjustment costs fall. In the current global configuration, asymmetry is not simply tolerated; it is systematically reinforced. Value, liquidity, and decision-making capacity accumulate in a narrow set of actors and locations, while volatility, constraint, and fiscal pressure are displaced outward. This is not the result of individual policy errors, but of a system that increasingly stabilises itself by exporting instability.

Recent empirical work by the International Monetary Fund reinforces this logic in concrete terms: export success does not automatically translate into national gain. In its January 2026 working paper Who Captures Export Windfalls?, the IMF demonstrates that exchange rates, pricing conventions, and financial openness function as distribution mechanisms that determine whether export windfalls are retained domestically or absorbed abroad. In many advanced economies, currency appreciation and dominant-currency pricing neutralise export price gains, reallocating rents to foreign buyers, multinational firms, or global financial markets. What appears as competitiveness at the trade level thus frequently dissolves into leakage at the monetary and financial level.

Understanding how this asymmetry is produced requires examining the structural mechanics of the system itself.

III. From Interdependence to Unequal Interdependence

The previous phase of globalisation was characterised by dense interdependence: complex supply chains, cross-border investment, and institutional coordination. Today, interdependence remains — but it has become unequal.

Certain nodes in the system exercise disproportionate control over:

- capital allocation

- technological standards

- data flows

- payment and settlement infrastructure

- legal jurisdiction

Others remain connected, but without reciprocal influence.

This produces a system in which participation does not guarantee agency. States may be deeply integrated while remaining structurally dependent.

IV. Why integration no longer guarantees convergence

For much of the late twentieth century, economic integration was assumed to lead, over time, to convergence. Participation in global markets was expected to generate upgrading, productivity growth, and institutional strengthening. That logic has weakened. In a world where value is concentrated in technology, finance, and intangible assets, integration alone no longer ensures development or resilience. Countries and regions can be deeply embedded in global value chains while remaining locked into low-margin roles, exposed to shocks they cannot absorb, and unable to reinvest at scale. Integration persists, but agency diminishes.

V. The United States: Asymmetry Through Centrality

The United States occupies a uniquely central position in the global system.

Its power does not derive solely from military capability or diplomatic reach, but from structural centrality across multiple layers:

- the world’s deepest capital markets

- the dominant reserve currency

- leading digital platforms and cloud infrastructure

- frontier artificial intelligence and semiconductor design

- legal jurisdiction that underpins global finance

These layers reinforce one another. Financial centrality supports technological dominance; technological platforms extend monetary reach; legal authority underpins both.

The result is systemic asymmetry without formal empire: influence exercised through infrastructure rather than territorial control.

VI. China: Asymmetry Through Scale and Integration

China’s position in the emerging G2 order is structurally different.

Rather than centrality, China’s asymmetry derives from:

- industrial scale

- state-directed capital allocation

- infrastructure-led integration

- long-term planning capacity

China has embedded itself deeply into global manufacturing and logistics while simultaneously reducing exposure to external vulnerability. Through initiatives such as the Belt and Road Initiative, China has extended this model outward, linking trade, finance, energy, and transport across Eurasia, Africa, and beyond.

This approach does not aim to replicate U.S. financial centrality. Instead, it builds alternative corridors of economic gravity, anchored in physical infrastructure and state-backed finance.

VII. Asymmetry Without Alignment: The Rest of the World

Outside the G2, most states do not seek to choose sides. Their primary objective is risk reduction.

Exposure to a single monetary or technological centre generates vulnerability:

- currency volatility

- capital-flow reversals

- sanctions and extraterritorial enforcement

- supply-chain disruption

As a result, many states pursue diversification rather than alignment. This impulse underpins the expansion of BRICSand similar groupings. These initiatives do not represent a unified alternative order, but a shared desire to dilute dependence.

The consequence is not balance, but fragmented asymmetry: multiple partial systems coexisting without a single stabilising centre.

IIX. Technology as the Multiplier of Asymmetry

Technology is the decisive multiplier in this process.

Control over:

- data

- compute

- platforms

- standards

generates compounding advantage. Unlike traditional industrial assets, digital systems scale globally with minimal marginal cost, allowing early leaders to entrench dominance rapidly.

Once embedded, these systems are difficult to displace. Switching costs rise, interoperability declines, and governance authority migrates toward those who control the underlying infrastructure.

Asymmetry thus becomes path-dependent.

IX. Financialisation and the Compounding of Asymmetry

A critical but often underappreciated driver of systemic asymmetry is the financialisation of advanced economies. Since the end of the Bretton Woods system, global growth has become increasingly mediated through financial markets rather than through the expansion of productive capacity.

In this environment, price is frequently treated as a proxy for value, and short-term financial returns are mistaken for long-term economic strength. Activities that extract value through leverage, asset inflation, or speculative trading are rewarded more immediately than investments in infrastructure, skills, or industrial capability.

This dynamic compounds asymmetry. Economies and firms positioned upstream in global value chains — particularly those controlling technology, intellectual property, and financial intermediation — capture stable rents. Those positioned downstream face volatile prices, thin margins, and limited capacity to reinvest.

X.Financialisation and the illusion of value creation

One reason this divergence has intensified is the growing dominance of financialised metrics over real economic capacity. When market prices are treated as proxies for long-term value, activities that extract returns through leverage, asset inflation, or speculative circulation are rewarded more quickly than those that build productive infrastructure, skills, or industrial depth. This does not merely reflect existing inequality; it accelerates it. Economies positioned upstream in finance and technology compound advantage, while those downstream struggle to translate participation into sustained development. Over time, this dynamic weakens the system’s capacity to correct itself.

XI. Asymmetry Without a Real-Economy Anchor

A further source of systemic fragility lies in the growing disconnection between monetary centrality and the real economy. Reserve-currency systems are most stable when they are anchored in broad-based productive capacity — encompassing manufacturing, infrastructure, energy, labour, and long-term investment. When monetary dominance becomes increasingly tied to intangible, financialised, and digital value, the system’s ability to absorb shocks internally diminishes.

In the contemporary global economy, a rising share of value creation — and valuation — is concentrated in digital platforms, financial assets, and intellectual property rather than in physically grounded production. This concentration reinforces asymmetry. Economies positioned at the centre capture rents from capital markets, data, and platforms, while those downstream supply labour, resources, or low-margin goods without commensurate upgrading.

Global financial markets amplify this dynamic. Capital is highly mobile, deeply integrated, and increasingly self-referential. Returns generated in the core are recycled back into the same markets, reinforcing valuation, liquidity, and monetary centrality. This process does not require deliberate policy coordination; it emerges endogenously from integrated financial systems.

For regions such as Europe, this creates a structural feedback loop. Institutional investors, pension funds, and households allocate a significant share of long-term savings to U.S. markets. As those markets become more concentrated in digital and intangible sectors, foreign capital increasingly underwrites an economic model over which external investors have limited control, while diverting investment away from domestic productive capacity.

The expansion of cryptocurrencies and digital financial instruments further intensifies this abstraction. Rather than anchoring value more firmly in the real economy, many digital assets layer additional financialisation onto an already intangible system, accelerating capital circulation without strengthening productive capacity.

Such a configuration is not inherently unstable in the short term. But over time, a reserve system that relies primarily on financial and digital dominance — rather than on a resilient real economy — becomes increasingly dependent on continuous capital inflows and confidence effects. Adjustment pressures are displaced outward, onto dependent economies and investors, rather than absorbed at the centre.

This is not a prediction of collapse. It is a structural condition that increases fragility, inequality, and systemic tension within an already asymmetric global order.

XII. Monetary Architecture and the Visibility of Power

Monetary systems reveal structural asymmetry rather than create it.

The global role of the dollar reflects deeper asymmetries in capital markets, legal enforcement, and financial infrastructure. Similarly, efforts to diversify settlement systems or develop alternative currencies respond to — rather than cause — unequal exposure.

Monetary architecture functions as a transmission mechanism, converting structural imbalance into tangible constraint or leverage.

This is why monetary tension emerges even in the absence of overt conflict.

XIII. Asymmetry, Exchange, and the Limits of the Post-War Order

Some degree of asymmetry is not only unavoidable, but necessary. It exists in all relationships and interactions and is the basis of exchange. Asymmetry becomes problematic not by its presence, but by the nature of the dynamics it produces: whether it enables shared growth and development, or whether it turns extractive and generates diminishing returns.

For much of the post-war period, the asymmetry embedded in the relationship between the United States, its allies, and the wider global economy functioned as an engine of growth. The system of exchange — anchored in security guarantees, open markets, industrial expansion, and energy abundance — contributed to the fastest period of economic and social development in human history.

That dynamic is now changing.

Under conditions of energy constraint, financialisation, and technological concentration, the same exchange increasingly exhibits extractive characteristics. Returns become uneven, adjustment costs are externalised, and dependence deepens without corresponding gains in productive capacity. This shift does not only affect allies and partners; it also generates dysfunction within the dominant economy itself.

From this perspective, recurring claims of “unfair trade,” “free-riding allies,” or insufficient burden-sharing misdiagnose the problem. They treat symptoms as causes. The reinforcing dynamic lies less in external behaviour than in internal policy choices that prioritise financial extraction, asset inflation, and short-term leverage over productive reinvestment and system balance.

Recent developments are likely to intensify this misalignment. U.S. energy autonomy reduces external constraint but also weakens incentives for systemic coordination. The growth of digital currencies, platform-based finance, and so-called network states further decouples financial flows from domestic productive systems. These trends amplify asymmetry rather than resolving it.

For Europe, this dynamic manifests as both external dependence and internal strain. Uneven exposure to energy costs, capital flows, and industrial decline complicates integration and fuels ideological divergence. What appears as political fragmentation is, in large part, a structural outcome of asymmetric exchange in a system no longer configured for shared growth.

In this sense, systemic asymmetry is not a moral failure or a breakdown of trust. It is the predictable result of a global system whose underlying energy, financial, and technological foundations have shifted, while institutional arrangements remain anchored in an earlier era.

XIV. Why Regulation Alone Cannot Restore Balance

A key implication of systemic asymmetry is the declining effectiveness of rule-based correction.

Regulation operates within jurisdictions. Asymmetry operates across them.

When power is embedded in:

- global platforms

- cross-border capital markets

- infrastructure networks

legal remedies struggle to realign outcomes. Enforcement becomes reactive; remedies lag behind scale; compliance does not equal control.

This does not render law irrelevant — but it exposes its limits when not backed by material capacity.

XV. A System Designed for Imbalance

The emerging G2 order is not asymmetric because it is unfinished or malfunctioning. It is asymmetric because it is designed around mechanisms that systematically concentrate capacity, influence, and optionality.

Scale advantages in technology, finance, and platforms do not dissipate over time; they compound. Financialisation rewards liquidity and abstraction over production. Digital systems embed governance within infrastructure rather than institutions. Capital mobility allows adjustment costs to be externalised rather than absorbed.

Within such a system, imbalance is not an anomaly to be corrected through policy fine-tuning or regulatory harmonisation. It is an endogenous outcome of how value is created, captured, and reinforced across borders.

This is why corrective mechanisms that worked in earlier phases of globalisation — trade liberalisation, institutional convergence, rule-based coordination — now yield diminishing returns. They operate on the assumption of symmetry that no longer exists.

Understanding the system as designed for imbalance is a prerequisite for understanding why pressure accumulates, why diversification accelerates, and why confrontation eventually emerges — even in the absence of deliberate escalation.

Conclusion — Asymmetry as the New Baseline

Systemic asymmetry is no longer a deviation from the global order; it is its defining feature.

In the emerging G2 order, asymmetry is not a transitional imbalance awaiting correction, but an endogenous featureof a system structured around scale, financial centrality, technological concentration, and growing detachment from the real economy. It explains why pressure accumulates, why diversification accelerates, and why neutrality becomes harder to sustain.

Understanding this condition is essential before analysing conflict, rivalry, or response. How asymmetry turns into confrontation is the subject of the Techwar analysis that follows. Its regional consequences — particularly for Europe — are examined in subsequent sections.

The G2 order is not balanced.

It is not converging.

And it is not neutral.

It is asymmetric by design.

Reference:

International Monetary Fund (2026), Who Captures Export Windfalls? Exchange Rates, Export Profitability, and National Saving, IMF Working Paper, January 2026.

Further Reading

Foundational Context

Transmission Channels

System Response

Suggested Reading

- [System Foundations of the Energy–AI–Industrial Economy (Global / Foundations)]

- Energy Sovereignty as System Control (Global / Doctrines)

- Europe’s

Energy Paradigm Shift (EU Sovereignty)System Default (Systems under

Constraint)

On how systems revert to leverage, exclusion, and coercion under strain. - Systemic Asymmetry

European application:

- EU

Asymmetry Under Stress(EU Sovereignty) - Energy and the Base Layer

of Constraint On why energy volatility establishes the first binding

limit shaping system exposure. - The Global

Energy Paradigm Shift On how the end of fossil-fuel abundance

re-materialises inflation and vulnerability. - Energy

and the Base Layer of Constraint On why energy volatility

establishes the first binding limit shaping system exposure.

Transmission Channels - Monetary Sovereignty in an Energy-Bound System - Global Value Chains in an Energy-Bound World On how fragmentation transmits stress unevenly across regions and systems.

- System Default (Systems under

Constraint)

On how systems revert to leverage, exclusion, and coercion under strain. - Industrial Policy Inside Constrained Systems (Systems under Constraint) On why policy ambition collides with constraint when upstream systems misalign.

- Agency Under Constraint (Systems under Constraint) On how strategy is redefined once asymmetry becomes unavoidable.