The Petrodollar Is Not Ending — It Is Being Rewired

Stablecoins, Electrification, LNG, and the Emerging Monetary–Energy Order

The current tensions around Iran are being discussed primarily through the language of uranium enrichment, deterrence, and regional escalation.

Those dimensions are real.

But the crisis is also revealing something deeper: the global monetary-energy order is entering a period of structural transition.

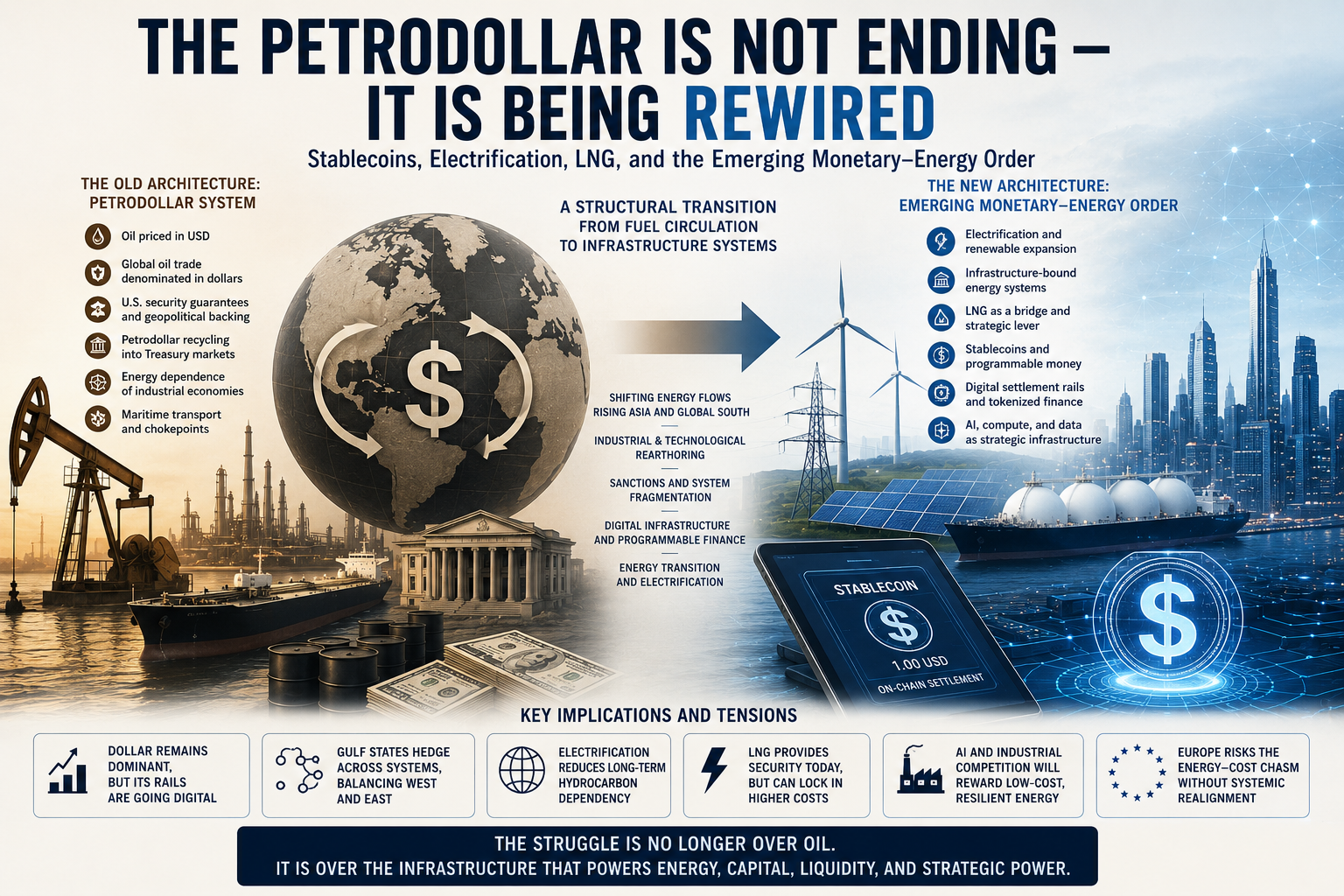

For decades, the international system rested upon a relatively coherent architecture linking Gulf energy production, maritime security, dollar-denominated oil settlement, U.S. Treasury markets, and American strategic power.

This architecture became known as the petrodollar system.

But the petrodollar was never simply about pricing oil in dollars. It was a wider geopolitical-financial structure through which hydrocarbon flows reinforced global dollar demand, deepened Treasury market liquidity, and stabilised American monetary power across the international system.

Energy and monetary order became structurally intertwined.

The global economy therefore operated through a reinforcing cycle:

oil trade generated dollar demand,

dollar demand reinforced Treasury markets,

Treasury markets stabilised American financial power,

and American strategic power protected the wider energy system upon

which the architecture depended.

For decades, this system functioned with remarkable durability.

Today, however, the foundations beneath it are beginning to shift.

Global energy flows are increasingly moving toward Asia. China has become the principal growth market for Gulf energy exports. Eurasian industrial integration continues to deepen. Simultaneously, sanctions regimes, technological fragmentation, AI infrastructure competition, industrial reshoring, and geopolitical instability are accelerating pressure on the existing monetary system.

This does not mean that the dollar is disappearing.

In fact, periods of instability often strengthen it.

Capital still overwhelmingly moves toward dollar assets and U.S. Treasury markets during moments of geopolitical stress. The dollar remains dominant across reserve systems, sovereign financing, liquidity markets, energy settlement, and global trade.

But dominance and stability are not necessarily the same thing.

This distinction is increasingly important.

The Gulf states themselves increasingly embody the contradictions of the emerging order.

On the one hand, Gulf sovereign wealth continues recycling enormous amounts of capital into the American financial system, particularly into technology and AI-related assets. U.S. capital markets remain the deepest and most liquid in the world. The United States continues to dominate advanced financial infrastructure, cloud-scale computing, semiconductor design, AI platforms, and global liquidity architecture.

But strategically, the long-term orientation of the Gulf increasingly points toward Asia.

This shift is not ideological.

It reflects the changing geography of the global economy itself.

China increasingly represents:

the centre of industrial expansion,

the largest source of future energy demand,

the core manufacturing ecosystem of Eurasia,

and an increasingly important technological and infrastructural partner.

At the same time, Gulf states increasingly understand that the long-term hydrocarbon era itself is evolving.

Climate pressure, electrification, AI infrastructure, logistics integration, industrial diversification, and sovereign wealth repositioning are gradually transforming how these states understand future power.

The Gulf is therefore attempting to hedge structurally across systems.

This is why Gulf strategy increasingly revolves around:

sovereign wealth diversification,

AI infrastructure,

logistics corridors,

industrial partnerships,

digital systems,

and strategic balancing between Washington and Beijing.

The Gulf is no longer operating exclusively inside a purely Atlantic system.

It is positioning itself between systems.

And this creates one of the defining asymmetries of the emerging global order:

financial capital continues recycling through the American monetary

system,

while industrial and energy gravity increasingly shifts toward

Eurasia.

That divergence matters enormously.

Because monetary systems ultimately require stability.

They require confidence that financial claims remain anchored, at least indirectly, to productive systems, industrial capacity, energy resilience, and long-term economic coherence.

This is where stablecoins and digital monetary infrastructure become strategically significant.

Many analysts assume that stablecoins threaten dollar dominance.

But the opposite outcome may ultimately prove more important.

Stablecoins may become one mechanism through which the United States attempts to extend dollar power into a new technological phase.

Under this model, the transition is not necessarily:

petrodollar → post-dollar world

but rather:

petrodollar → programmable dollar infrastructure.

This distinction is critical.

The United States increasingly appears to understand that monetary power in the twenty-first century may depend not only upon reserve holdings and traditional banking systems, but increasingly upon:

programmable payment rails,

digital settlement systems,

Treasury-backed liquidity,

sanctions-compliant financial infrastructure,

cloud-scale financial architecture,

and technologically integrated capital networks.

Under these conditions, stablecoins cease functioning merely as speculative crypto instruments.

They become geopolitical-financial infrastructure.

But this transition also introduces new systemic contradictions.

If global asymmetry was already a defining feature of the previous phase of globalisation, the emerging monetary transition may reinforce those imbalances even further.

A digitally extended dollar system could become simultaneously:

more powerful,

more abstract,

and increasingly detached from the physical foundations of the wider global economy.

This matters because the American financial system increasingly concentrates global liquidity, technological valuation, and capital absorption even while parts of the underlying productive economy become more fragmented, more financialised, and more politically inward-looking.

The contradiction is profound.

The dollar system can continue strengthening financially even while broader systemic instability intensifies underneath it.

And this may not even ultimately strengthen the wider U.S. economy itself.

Financial dominance and domestic industrial resilience are not identical things.

A system increasingly driven by:

digital liquidity expansion,

financial concentration,

speculative AI valuation,

and global capital absorption

can generate enormous monetary power while simultaneously amplifying:

internal inequality,

industrial hollowing,

asset inflation,

geopolitical instability,

and systemic fragility.

At the same time, another structural shift is beginning to emerge beneath the surface of the global economy.

The petrodollar system was built around globally traded hydrocarbons. Oil required continuous maritime transport, large-scale foreign-currency recycling, and globally integrated energy markets.

Electrification gradually changes part of this logic.

Electricity is far more infrastructure-bound and geographically localised than oil.

As economies increasingly rely upon:

domestic renewables,

nuclear systems,

storage infrastructure,

regional grids,

and industrial electrification,

part of the structural dependence on continuous hydrocarbon imports may gradually decline.

This has profound implications not only for Europe, but also for the Gulf itself.

Under the hydrocarbon era, Gulf states accumulated structural power because the global economy required permanent hydrocarbon circulation. Oil exports reinforced dollar demand because industrial economies required constant access to imported fossil fuels.

But under electrification conditions, parts of the global system gradually become less dependent on permanent hydrocarbon imports and therefore potentially less dependent upon continuous foreign-currency recycling through oil trade itself.

This does not eliminate the strategic importance of the Gulf.

Far from it.

The Gulf is increasingly repositioning itself as:

a logistics node,

an AI-energy infrastructure node,

a sovereign investment node,

a digital-financial node,

and a strategic connector between Asia, Europe, and Africa.

But the underlying monetary-energy logic is nevertheless evolving.

Under the hydrocarbon era, power flowed primarily through fuel circulation.

Under electrification, power increasingly flows through infrastructure systems.

The strategic struggle therefore is no longer simply over energy resources themselves.

It is increasingly over the systems that organise energy:

grids,

compute,

industrial ecosystems,

semiconductor capacity,

infrastructure coordination,

and digital settlement architecture.

This is where Europe’s position becomes especially dangerous.

In theory, electrification should gradually allow Europe to reduce part of its structural dependency on imported hydrocarbon systems.

But Europe now risks becoming trapped inside the transition layer itself.

This is because LNG re-globalises dependency precisely at the moment electrification could theoretically begin regionalising resilience.

Unlike locally generated electricity, LNG remains:

globally traded,

dollar-denominated,

maritime-dependent,

financially intermediated,

and structurally tied to international commodity markets.

LNG certainly improves short-term resilience after the Russian rupture.

But strategically, it can also deepen Europe’s dependency on:

dollar settlement systems,

global energy-price volatility,

imported inflation,

external supply dependency,

and U.S.-centred energy-financial architecture.

This is the deeper contradiction now confronting Europe.

At precisely the historical moment when electrification could theoretically reduce structural dependence on foreign-currency hydrocarbon recycling, Europe may instead be locking itself more deeply into expensive transition energy systems.

And under AI-electrification conditions, this matters enormously.

Because the transition is not occurring symmetrically.

The United States crosses the transition with domestic hydrocarbons, LNG export capacity, reserve-currency privileges, deep capital markets, and technological dominance.

China crosses it with industrial scale, manufacturing ecosystems, infrastructure coordination, and increasingly integrated energy-industrial planning.

Europe crosses it with fragmented capital allocation, higher marginal energy costs, infrastructure latency, LNG dependency, regulatory fragmentation, and incomplete industrial coordination.

This is the Energy–Cost Chasm.

And LNG may unintentionally reinforce it.

High energy costs under AI-electrification conditions transmit directly into industrial compression, weaker reinvestment, slower infrastructure scaling, reduced compute competitiveness, lower productivity growth, capital outflows, and eventually monetary fragility.

Because AI infrastructure increasingly scales through electricity intensity, compute locality, grid resilience, cooling systems, and industrial ecosystems, the cost divergence compounds over time rather than remaining temporary.

This is why the current transition matters so profoundly.

The future monetary order will not be determined only by central banks or reserve holdings.

It will increasingly be determined by the systems behind currencies:

energy systems,

infrastructure systems,

industrial ecosystems,

technological coordination,

and settlement architecture.

The global order is entering a phase in which energy systems, monetary systems, AI infrastructure, digital finance, industrial capacity, and geopolitical power are becoming increasingly integrated.

The petrodollar is not disappearing overnight.

But it is beginning to evolve.

And the emerging struggle is no longer simply over oil.

It is increasingly over the infrastructure through which energy, capital, liquidity, and strategic power will be organised in the next global system.

System Navigation

Reading the Emerging Monetary–Energy Transition

This article examines how the transition from hydrocarbon circulation toward infrastructure-based electrification is beginning to reorganise monetary power, geopolitical asymmetry, and strategic dependency.

The following reading sequence expands the wider system architecture behind this transition.

I. Foundational Monetary and Energy Architecture

These articles establish how energy systems condition monetary durability, capital allocation, and geopolitical power under Energy-Bound conditions.

Energy Constraint and the Monetary Ceiling How persistent energy-cost divergence gradually produces monetary compression and capital asymmetry.

AI Energy and the Future of Sovereignty Why AI infrastructure increasingly depends upon electricity systems, industrial depth, and infrastructure coordination.

AI Has Become Physical Why computation increasingly scales through physical systems rather than software abstraction alone.

Strategic Minerals AI Energy System How strategic minerals increasingly function as infrastructure inputs into computational civilisation.

II. Systemic Asymmetry and the Emerging Transition

These articles examine how the AI-energy transition amplifies structural divergence between systems crossing the transition from different starting conditions.

AI Energy Cost Chasm Why energy-cost divergence increasingly translates into industrial, technological, and monetary asymmetry.

Financialised AI and the Infrastructure Reality Why financial valuation increasingly diverges from the physical infrastructure requirements of AI scaling.

Infrastructure Currency Doctrine Why monetary durability increasingly depends upon infrastructure systems rather than financial abstraction alone.

III. Europe and the Transition Layer

These articles examine why Europe risks becoming trapped inside the high-cost transition phase between hydrocarbon dependency and infrastructure sovereignty.

Europe Missing Conversion Layer Why Europe struggles to convert energy transition into industrial and strategic power.

LNG, NATO, and the Enforcement of System Power How LNG stabilises Europe short term while potentially reinforcing long-term structural dependency.

Mediterranean AI Infrastructure Geography Why Mediterranean infrastructure geography increasingly matters under AI-electrification conditions.

IV. Infrastructure Sovereignty and System Power

These articles examine how sovereignty increasingly depends upon integrated infrastructure architecture.

Energy Sovereignty as System Control Why energy architecture increasingly determines industrial resilience and monetary durability.

System Stack Architecture How energy, compute, infrastructure, capital, and sovereignty increasingly function as integrated systems.

Ecosystem Sovereignty Why future geopolitical power increasingly depends upon ecosystem coordination rather than isolated sectors.

V. Next Doctrine Layer

This article functions as an operational transition text within the wider monetary-energy framework.

The next major synthesis layer expands the transition from hydrocarbon monetary systems toward infrastructure-based electrification systems:

From Petrodollar to Electrodollar

This forthcoming framework examines how electrification, compute infrastructure, digital settlement systems, and energy sovereignty may reorganise monetary geography in the emerging global order.