Monetary Sovereignty and the New Monetary Cold War

Energy, Infrastructure, and the Struggle for System Control

Keynote

Monetary sovereignty no longer begins with currency issuance.

It begins with infrastructure.

In the twentieth century, monetary power was anchored in institutions — central banks, reserve agreements, trade settlements, and treaty systems. In the twenty-first century, it is embedded in digital architecture: cloud concentration, AI compute, payment rails, stablecoin protocols, and capital market depth.

Money now circulates through systems that sit upstream of law.

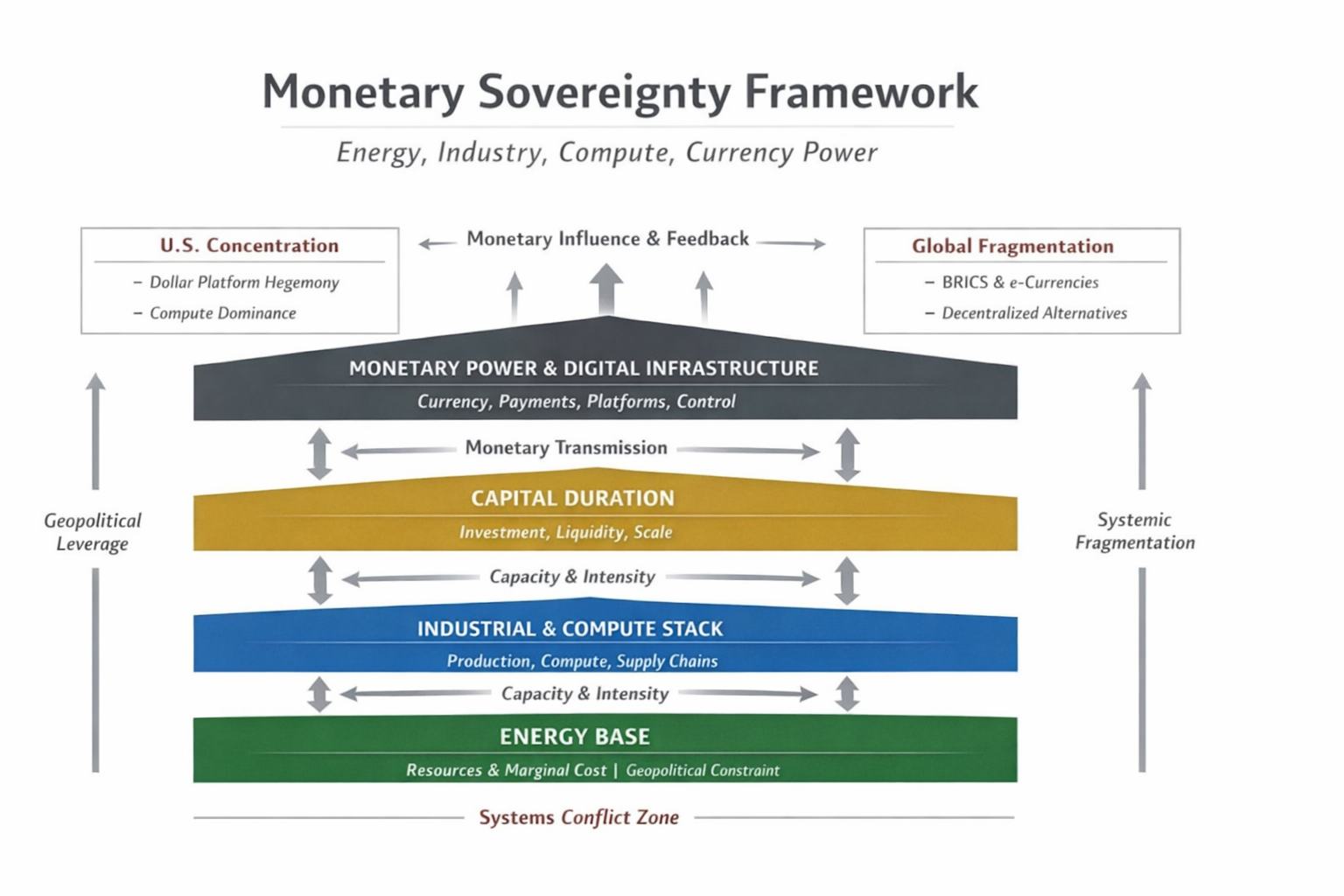

In an energy-bound global order, marginal energy cost shapes industrial competitiveness; industrial competitiveness shapes capital formation; capital formation shapes currency resilience. Digital infrastructure amplifies this chain. The actors that control the stack — energy, industry, compute, capital, and payment rails — shape the monetary order.

This is the new monetary cold war.

It is not fought through reserve replacement. It is fought through system design.

The United States has fused dollar dominance with digital platform concentration and energy resurgence. China is constructing programmable state money to reduce external vulnerability. Europe stands between concentration and fragmentation, institutionally strong yet infrastructurally dependent.

The comfortable middle ground of the post-war era is dissolving.

Monetary sovereignty in the digital age requires stack coherence. Without control over the layers beneath currency, sovereignty becomes conditional.

Executive Summary

The global monetary system is undergoing structural transformation driven not by treaty change but by digital infrastructure consolidation.

Three developments define the shift:

1. Monetary power is moving upstream.

Payment systems, cloud infrastructure, AI compute, and stablecoins now

mediate transactions before they enter the banking system. Currency

influence is increasingly embedded in privately operated digital

rails.

2. Energy and capital depth determine currency

resilience.

In an energy-bound system, marginal energy cost conditions industrial

competitiveness. Industrial depth supports productivity and capital

formation. Capital formation underpins monetary strength. Digital

infrastructure intensifies this transmission by concentrating compute

and liquidity where energy and capital are coherent.

3. Structural asymmetry is widening.

The United States combines energy abundance, deep capital markets,

platform dominance, and dollar centrality into a self-reinforcing

architecture. China is constructing programmable digital currency

systems to reduce dollar exposure. Digital dollarization is spreading

through private stablecoin infrastructure in emerging markets.

Europe faces a structural constraint:

higher marginal energy cost,

dependence on non-European cloud and AI infrastructure,

delayed digital monetary integration.

Without alignment across energy reform, industrial reinvestment, compute localization, and digital currency design, Europe risks gradual monetary leverage erosion rather than sudden crisis.

The strategic question is no longer whether the dollar will be replaced.

It is whether Europe will build sufficient stack coherence to prevent its currency from operating within infrastructure governed elsewhere.

Monetary sovereignty in the digital age is not a legal status.

It is a systems outcome.

I. The Quiet Rewriting of Monetary Power

The global monetary order is not collapsing.

It is being re-architected.

Not through treaty rupture.

Not through reserve replacement.

Not through overt geopolitical confrontation.

But through infrastructure.

Cloud platforms, hyperscale data centres, AI training clusters, semiconductor design chains, payment networks, digital wallets, and stablecoin protocols now mediate economic activity before it reaches traditional financial institutions. Monetary authority is migrating upstream — into the digital systems that structure transactions themselves.

This shift marks the beginning of a new monetary cold war.

It is not fought with tariffs or tanks. It is fought through control of the rails on which value moves. Whoever controls the energy base, the compute layer, the capital markets, and the payment architecture shapes the monetary environment within which all others operate.

In the twentieth century, money was anchored in institutions.

In the twenty-first, it is embedded in systems.

Europe enters this transition from a position of institutional strength but infrastructural dependency. That distinction will determine its strategic trajectory.

II. Monetary Power in an Energy-Bound World

In an era of abundant, cheap energy, monetary strength could be sustained by credibility, financial sophistication, and political stability. In an energy-constrained system, the hierarchy is harder and more material.

Marginal energy cost determines industrial competitiveness.

Industrial competitiveness determines productivity growth.

Productivity growth determines capital formation.

Capital formation determines currency resilience.

When structural energy disadvantage persists, the monetary system tightens. Investment weakens. Fiscal capacity narrows. Current-account pressure accumulates. The currency may not collapse, but its strategic leverage erodes.

Digital infrastructure intensifies this transmission.

AI compute is energy-intensive. Hyperscale data centres cluster where electricity is abundant and predictable. Advanced semiconductor fabrication depends on stable industrial ecosystems. Payment networks embed currency choice into daily commercial routines. Stablecoins scale where capital markets are deepest and regulation is permissive.

Monetary power is no longer an abstract financial phenomenon. It is a derivative of energy depth and compute concentration.

Money now sits inside the Energy–Industry–Compute stack.

III. The American Stack: Coherence as Power

The United States has assembled a structurally coherent system.

It combines energy abundance, deep capital markets, AI leadership, cloud concentration, semiconductor intellectual property, and dollar centrality into a mutually reinforcing architecture.

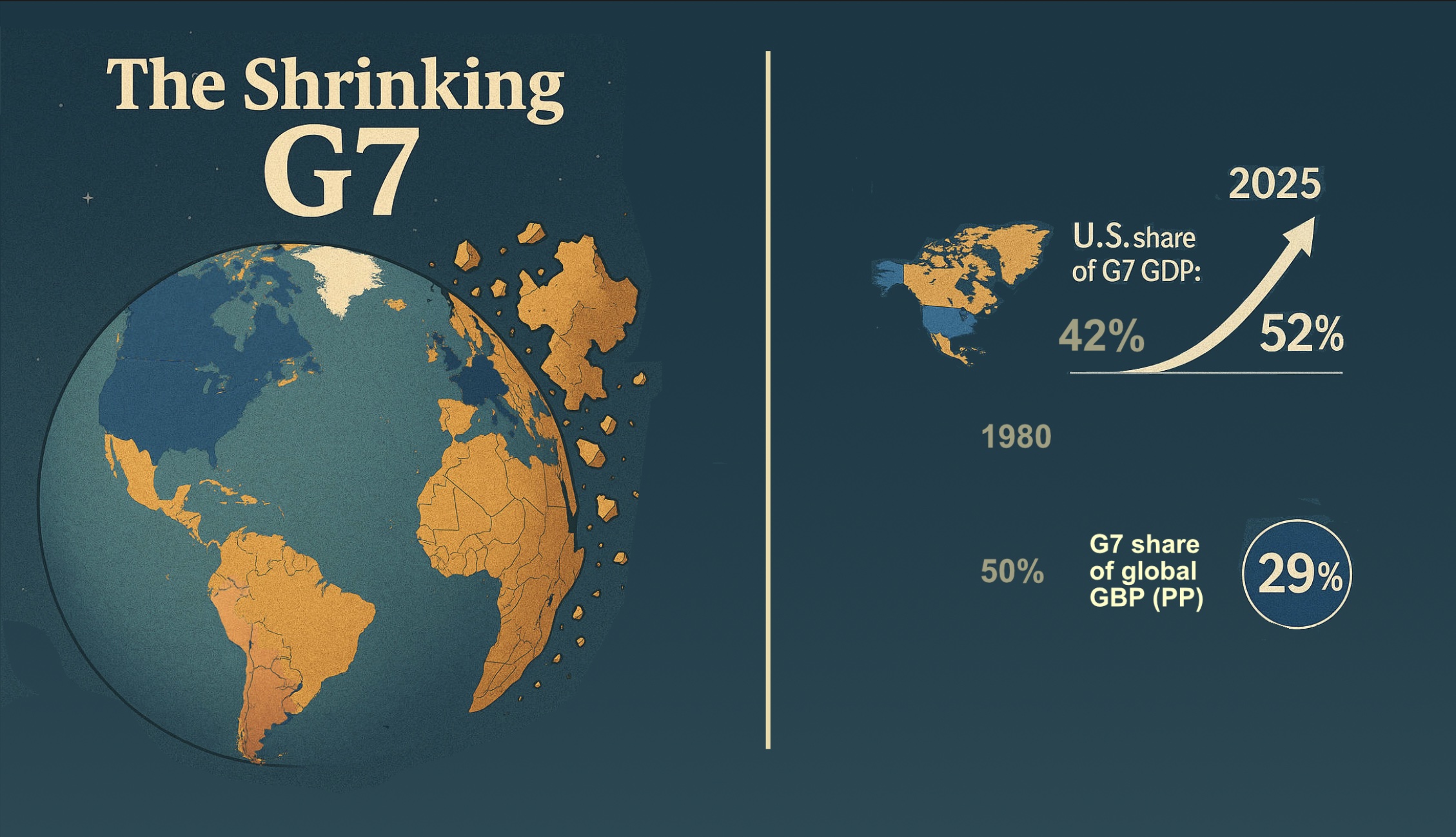

The U.S. now accounts for more than half of total G7 GDP. It dominates global equity capitalization and venture capital flows. Its firms operate the world’s largest hyperscale data centres. Its semiconductor designers anchor global supply chains. Its capital markets absorb global savings. Its energy production reduces domestic industrial cost pressure.

This coherence matters.

Dollar dominance attracts global capital seeking liquidity and security. That capital finances AI, defence-tech integration, and digital infrastructure expansion. Platform concentration embeds payment preference. Stablecoins denominated in dollars extend U.S. monetary influence into regions where traditional banking access is limited.

Digital dollarization operates without formal policy declaration. It spreads through usability.

The dollar is no longer only a reserve asset. It is a protocol layer.

Monetary power is exercised not solely by the Federal Reserve, but through private infrastructure embedded across global commerce.

This is not traditional empire. It is infrastructural entrenchment.

IV. China’s Counter-Architecture

China’s response reflects a different philosophy.

The digital yuan (e-CNY) is not a market innovation. It is a state-engineered instrument designed to reduce vulnerability to dollar-based settlement systems. It integrates programmable money with centralized data visibility, capital controls, and platform integration.

Its ambition is not to replace the dollar as global reserve currency. Such a role would impose constraints inconsistent with China’s domestic governance model. Instead, Beijing seeks insulation and regional leverage.

Cross-border pilots along Belt and Road corridors signal an effort to construct alternative settlement pathways. Programmability allows targeted stimulus and transaction monitoring. Data becomes monetary policy infrastructure.

If the American model embeds monetary power within private platforms, the Chinese model embeds it within state architecture.

Both models recognize the same truth: sovereignty in the digital age requires system control.

V. The Demonstration Effect: Digital Dollarization

The implications of infrastructural monetary power are visible in Latin America.

Across Argentina, Venezuela, Colombia, Brazil, and Mexico, citizens transact in dollar-denominated stablecoins to hedge against domestic currency instability. These digital dollars circulate outside local banking systems, weakening monetary transmission and compressing tax collection capacity.

This is not official dollarization. It is functional displacement.

Transactions settle in U.S.-denominated digital tokens. Savings migrate into private dollar infrastructure. Governments lose policy traction without formal loss of currency status.

The lesson is clear: in a digitized financial environment, currency preference can shift through convenience rather than legislation.

For Europe, this case is not peripheral. If the digital euro remains delayed, fragmented, or poorly integrated into trade settlement and corporate treasury systems, dollar-based digital instruments can scale within European networks by default.

Monetary sovereignty in the digital era depends on adoption architecture, not legal decree.

VI. Fiscal Erosion and the Shrinking State

Digitalization also alters the fiscal base of advanced economies.

Intangible assets shift to low-tax jurisdictions. Platform-mediated commerce diffuses VAT capture. Automation compresses payroll tax contributions. Stablecoins and crypto transactions bypass regulated banking channels. Data extraction concentrates profit in jurisdictions hosting digital giants.

Europe’s welfare architecture relies heavily on payroll taxation and VAT. As economic value migrates into cross-border digital ecosystems largely controlled by foreign firms, fiscal resilience weakens.

Monetary sovereignty without fiscal durability is fragile.

When states struggle to finance infrastructure, defence, and social stability, currency strength becomes dependent on external capital tolerance.

Digital infrastructure thus shapes not only monetary power but the capacity of the state itself.

VII. G7 Asymmetry and the End of Parity

The G7 was once a grouping of near-equals.

It is now structurally asymmetrical.

The United States dominates AI frontier development, hyperscale cloud capacity, defence-tech integration, and global capital markets. It has reduced its energy vulnerability while maintaining currency centrality.

Europe faces higher marginal energy cost, slower productivity growth, digital trade deficits, and reliance on non-European platforms for cloud and compute.

This asymmetry feeds monetary divergence.

Capital duration accumulates in U.S. markets. Innovation clusters where energy and capital are coherent. The dollar benefits from deep liquidity and embedded digital infrastructure. The euro remains globally significant but increasingly peripheral to system design.

Monetary competition no longer operates solely between currencies. It operates between stacks.

VIII. Europe’s Structural Constraint

Europe’s challenge is therefore structural rather than rhetorical.

First, its energy architecture remains fragmented and costlier than that of the United States. Persistent marginal disadvantage compresses industrial margins and constrains fiscal flexibility.

Second, its compute infrastructure is externally anchored. Hyperscale cloud and AI training capacity are dominated by non-European providers. Value capture migrates upstream.

Third, its digital monetary architecture remains cautious and incomplete. The digital euro project proceeds carefully, but private dollar instruments scale aggressively.

This triad — energy constraint, compute dependency, monetary passivity — forms a structural ceiling.

Without integration across these layers, monetary sovereignty becomes conditional on the goodwill and stability of external infrastructure.

Legal sophistication cannot substitute for system control.

IX. The Dissolution of the Middle Ground

For decades, Europe benefited from a stable transatlantic equilibrium. It relied on U.S. security guarantees, accessed dollar liquidity, and focused on regulatory refinement rather than infrastructural dominance.

That equilibrium is dissolving.

The United States increasingly operates as a consolidated digital-energy superpower. China constructs parallel monetary corridors. Regional blocs experiment with commodity-backed or fintech-driven settlement systems.

The middle ground narrows not because Europe lacks capability, but because infrastructure concentration reduces room for passive positioning.

Neutrality becomes structurally difficult when payment rails, cloud hosting, AI scaling, and digital currency issuance are controlled elsewhere.

X. Monetary Sovereignty as Stack Integration

In this environment, issuing a digital euro is insufficient.

Monetary sovereignty requires integration across the Energy–Industry–Compute stack.

Energy stabilization lowers industrial cost floors. Industrial depth supports productivity and capital formation. Compute localization retains data and AI value capture. Capital market depth anchors liquidity. Payment infrastructure embeds currency usage.

If one layer is externally dependent, sovereignty fragments.

The euro’s long-term resilience depends on structural coherence between energy reform, industrial reinvestment, compute autonomy, and digital currency architecture.

Absent this coherence, Europe risks strategic stagnation: a respected currency operating within infrastructure governed elsewhere.

XI. A Structural Decision

The new monetary cold war will not produce dramatic currency replacement.

It will produce gradual leverage shifts.

Currencies embedded in dominant infrastructure gain default status. Those operating within external systems become subordinate.

The contest is not about dethroning the dollar tomorrow. It is about determining whose architecture structures global exchange for the next generation.

Europe’s choice is therefore not ideological.

It is structural.

It can remain a sophisticated regulator of systems built elsewhere.

Or it can align energy, compute, capital, and currency into a coherent architecture capable of anchoring its own monetary sphere.

Infrastructure is becoming destiny.

In an energy-bound, digitally mediated world, sovereignty belongs to those who build and control the stack.

The question for Europe is no longer whether the monetary order is changing.

It is whether Europe intends to shape that order — or operate inside one designed by others.

Further Reading — Structural Foundations (From This Series)

Global System Architecture

Energy as the Operating System of Power How energy depth conditions industrial scale, monetary resilience, and geopolitical leverage.

Energy-Bound System (Doctrine) Defines structural constraint in an era of marginal energy cost divergence.

EU Sovereignty Panel

Energy Constraint and the Monetary Ceiling How persistent marginal energy disadvantage translates into currency pressure.

The Energy–Industry–Compute Stack Europe’s material operating system under structural compression.

Execution Under Compression A strategic warning for euro architecture under energy constraint.

Europe’s Vanishing Middle Ground The narrowing corridor between U.S. concentration and global fragmentation.

Further Reading — Structural Foundations (From This Series)

Global System Architecture

Energy as the Operating System of Power How energy depth conditions industrial scale, monetary resilience, and geopolitical leverage.

Energy-Bound System (Doctrine) Defines structural constraint in an era of marginal energy cost divergence.

EU Sovereignty Panel

Energy Constraint and the Monetary Ceiling How persistent marginal energy disadvantage translates into currency pressure.

The Energy–Industry–Compute Stack Europe’s material operating system under structural compression.

Execution Under Compression A strategic warning for euro architecture under energy constraint.

Europe’s Vanishing Middle Ground The narrowing corridor between U.S. concentration and global fragmentation.

AI–Energy–Sovereignty Trilogy

AI–Energy–Sovereignty (Micro) Infrastructure and compute constraint.

AI–Energy–Sovereignty (Meso) Industrial integration and scaling risk.

AI–Energy–Sovereignty (Macro) The sovereignty ceiling under energy-bound conditions.

Why Europe Needs a Compute-Locality Doctrine How compute placement determines monetary and industrial leverage.

Monetary & Infrastructure Layer

Monetary Power Energy, industry, infrastructure, geopolitics.

Beyond Ideology Why political framing collapses when systems become binding.

Suggested Reading — Monetary Sovereignty & Digital Infrastructure Power

1. Dollar Dominance & Monetary Power

IMF (2026) — Who Captures Export Windfalls?

Exchange Rates, Export Profitability, and National Saving under

Dominant-Currency Pricing

https://www.imf.org/en/publications/wp/issues/2026/01/16/who-captures-export-windfalls-exchange-rates-export-profitability-and-national-saving-573291

Explains how dominant-currency pricing reinforces structural asymmetry and capital accumulation advantages.

Barry Eichengreen (2011) — Exorbitant

Privilege

https://press.princeton.edu/books/hardcover/9780691138486/exorbitant-privilege

Classic analysis of dollar hegemony and its structural foundations.

BIS (2023) — Annual Economic Report —

Geoeconomics Fragmentation

https://www.bis.org/publ/arpdf/ar2023e.htm

Details how geopolitical fragmentation affects financial stability and cross-border capital flows.

2. Digital Currency & CBDCs

BIS (2021) — CBDCs: An Opportunity for the

Monetary System

https://www.bis.org/publ/arpdf/ar2021e3.htm

Foundational institutional view of CBDCs and monetary architecture.

ECB (Digital Euro Project Page)

https://www.ecb.europa.eu/paym/digital_euro/html/index.en.html

Official documentation and progress on the digital euro.

People’s Bank of China — e-CNY Overview

http://www.pbc.gov.cn/en/3688110/3688172/index.html

Primary material on the digital yuan framework.

Atlantic Council CBDC Tracker

https://www.atlanticcouncil.org/cbdctracker/

Real-time tracking of global CBDC development and cross-border pilots.

3. Stablecoins & Digital Dollarization

BIS (2023) — Stablecoins: Risks and Policy

Responses

https://www.bis.org/publ/qtrpdf/r_qt2309g.htm

Explains systemic implications of stablecoin expansion.

Federal Reserve (2022) — Money and Payments: The

U.S. Dollar in the Age of Digital Transformation

https://www.federalreserve.gov/publications/money-and-payments-discussion-paper.htm

The Fed’s framing of digital dollar risks and opportunities.

International Monetary Fund — Crypto & Financial

Stability Reports

https://www.imf.org/en/Topics/fintech

Covers digital dollarization in emerging markets.

4. Platform Power & Infrastructure Control

Henry Farrell & Abraham Newman

(2019) — Weaponized Interdependence (International

Security)

https://www.mitpressjournals.org/doi/full/10.1162/isec_a_00351

Seminal analysis of how infrastructure control becomes geopolitical leverage.

Shoshana Zuboff (2019) — The Age of Surveillance

Capitalism

https://www.publicaffairsbooks.com/titles/shoshana-zuboff/the-age-of-surveillance-capitalism/9781610395694/

Explores data extraction and platform concentration dynamics.

Foreign Affairs (2024) — Petrostate

America

https://www.foreignaffairs.com/united-states/petrostate-america

Examines U.S. energy resurgence and geopolitical leverage.

5. Energy, Compute & Monetary Transmission

IEA — World Energy Outlook (Latest Edition)

https://www.iea.org/reports/world-energy-outlook-2023

Energy cost trajectories and industrial competitiveness implications.

IMF (2023) — Energy Shocks and the

Macroeconomy

https://www.imf.org/en/Publications/WP/Issues/2023/06/09/Energy-Shocks-and-the-Macroeconomy-534978

Transmission of energy prices into inflation and monetary policy.

Stanford HAI (AI Energy Use Studies)

https://hai.stanford.edu/research

Research on AI compute intensity and energy demand scaling.

6. Geoeconomic Fragmentation & System Rivalry

European Central Bank (2023) — The Geopolitics

of the Euro

https://www.ecb.europa.eu/pub/economic-bulletin/articles/2023/html/ecb.ebart202301_02~b1b3f3e69c.en.html

Examines euro internationalization challenges.

Branko Milanović (2023) — Capitalism,

Alone

https://www.hup.harvard.edu/books/9780674987599

On competing models of capitalism in a multipolar world.

World Bank — Global Economic Prospects

https://www.worldbank.org/en/publication/global-economic-prospects

Covers fragmentation and capital reallocation.

Optional Advanced / Strategic Layer

If you want a sharper geopolitical reading layer to match the flagship tone:

• Michael Pettis — writings on global imbalances

https://carnegieendowment.org/experts/509

• Adam Tooze — analysis of dollar liquidity and crisis politics

https://adamtooze.com

• BIS Papers on Cross-Border Payment Systems

https://www.bis.org/list/bppapers/index.htm