AI Energy Sovereignty (Macro) -Article I/III: AI, Energy, and Sovereignty

Why Europe’s AI Future Is Now an Infrastructure Race

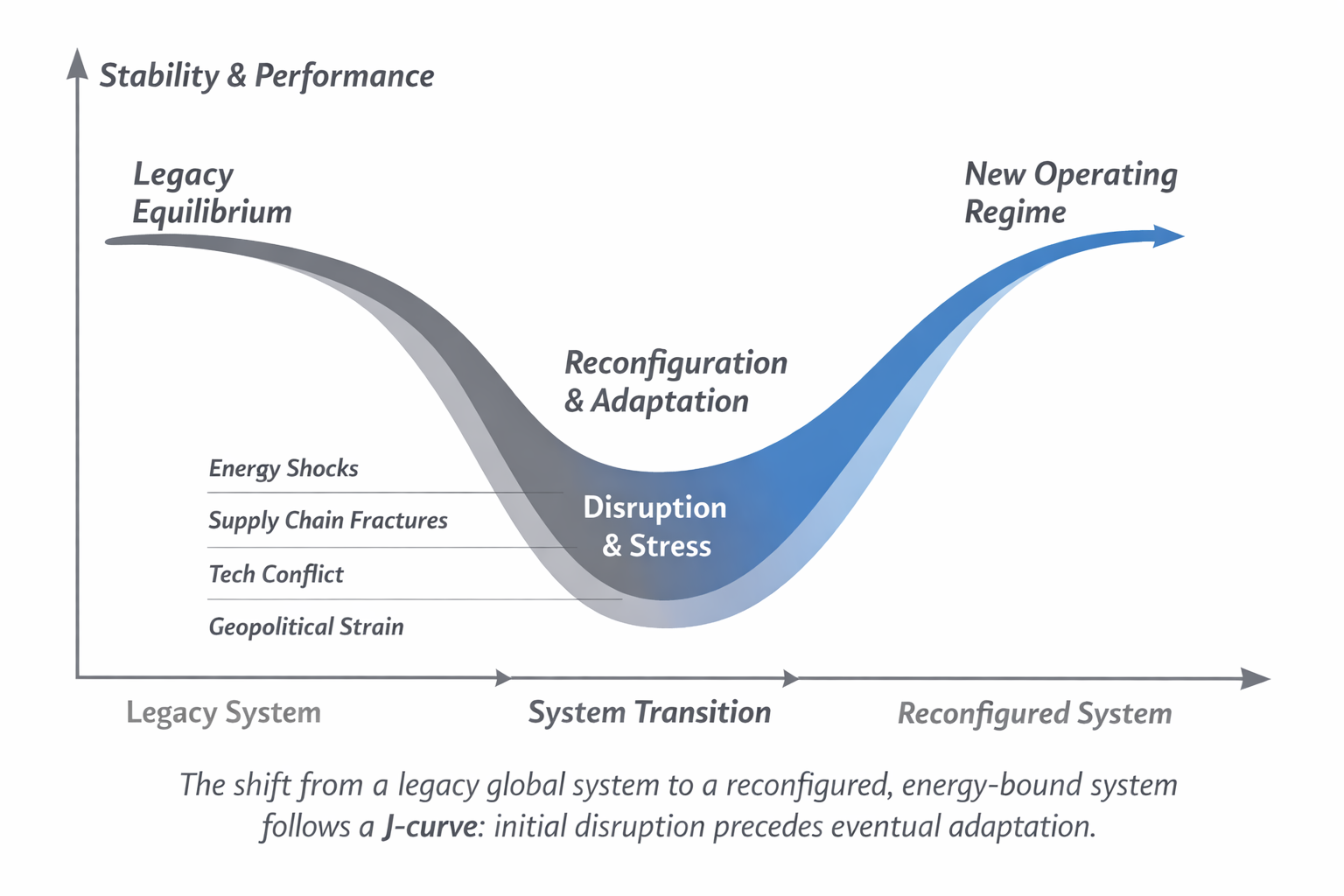

Energy Transition J-Curve and the European Energy

Chasm

Energy transitions temporarily increase marginal energy costs as legacy

systems are dismantled before renewable infrastructure fully scales.

Economies that move slowly risk remaining trapped in the transition

trough — the energy chasm — characterised by high

energy prices, compressed industrial margins, fiscal subsidies, and

rising debt pressure. Accelerating renewable deployment shortens this

phase and restores long-term energy cost advantage.

Preface — Why This Is No Longer a Technology Debate

This article examines the system layer — the macro constraints that determine whether firms and ecosystems can scale. It asks a decisive question: who can power AI at continental scale, and who cannot?

If Article I showed why productivity falls inside firms, and Article II explained why it fails to diffuse across ecosystems, this final layer asks what ultimately determines whether AI can scale at all.

Artificial intelligence is still discussed as a contest of algorithms, talent, and venture capital. That framing is already obsolete. The binding constraint is no longer computational ingenuity, but energy, infrastructure, and time.

AI, electrification, climate adaptation, and the Fourth Industrial Revolution are unfolding simultaneously. Together, they are producing a structural surge in electricity demand and a transformation in how power systems are designed, financed, and governed. This is not an incremental upgrade of existing grids; it is a system-wide shift.

For Europe, this convergence arrives after decades of deindustrialisation, ecosystem thinning, underinvestment in grids, and fragmented governance. Yet it also arrives at a moment when the material nature of AI is becoming unavoidable.

Energy is no longer an input into growth. It is the upstream determinant of industrial viability, geopolitical agency, and sovereignty.

1. From Digital Illusion to Physical Reality

For much of the last three decades, Europe operated under a comforting assumption: that economic growth could be progressively dematerialised. Services, finance, and intangible technologies would substitute for energy intensity, heavy industry, and physical infrastructure.

AI shatters that illusion.

Training, deploying, and operating AI systems requires:

- vast data centres

- continuous, high-quality electricity

- cooling, storage, and redundancy

- resilient grids with low downtime

- physical proximity between compute, power, and demand

At the same time, transport, heating, industry, defence, and logistics electrify. These demands stack; they do not substitute for one another. AI does not reduce energy consumption—it multiplies it.

The result is not linear growth in demand, but a step-change in system stress.

2. Electrification Is Not Optional — It Is Binding

Europe’s electrification agenda is often framed as a climate choice. In reality, it is becoming a structural necessity.

- Electric vehicles replace combustion engines

- Heat pumps replace gas boilers

- Industrial processes electrify to decarbonise

- Defence and logistics digitise

- AI and 4IR embed real-time optimisation everywhere

Each transition raises peak load, not just average demand. Power systems designed for predictable, centralised generation now face volatile, decentralised, and time-sensitive loads.

The strategic risk is clear: power systems are slow to build, while demand is accelerating rapidly.

In this environment, energy availability, grid capacity, and permitting speed determine which regions can host AI infrastructure and advanced industry—and which cannot.

3. Investor Mythology and the US Model: Cheap Energy, Fragile Foundations

Investor enthusiasm for US AI dominance rests on a narrow reading of advantage: cheap fossil energy, hyperscale data centres, and an apparently frictionless innovation machine. This reading misses the binding constraint: infrastructure.

The US economy remains structurally dependent on:

- low-cost fossil fuels as a competitiveness lever

- highly centralised generation

- a rapidly ageing electrical grid designed for a different industrial era

Much of that grid depends on:

- long-distance transmission

- scarce transformers and power electronics

- globally stretched supply chains

- components increasingly sourced abroad

Cheap energy is not free. It is purchased through fragility, deferred maintenance, and exposure to disruption. Grid failures, transformer shortages, cyber risks, and long replacement timelines introduce systemic vulnerabilities that compound as AI and electrification scale.

This is why “AI gimmicks” and capital-market narratives can mislead: models can be trained quickly and valuations can rise overnight, but the physical substrate—grids, generation, permitting, components, and skilled labour—moves at the pace of infrastructure.

US advantage is therefore conditional: powerful in the short term, brittle over time.

4. Infrastructure Speed Is the New Strategic Variable

The decisive variable in the coming decade is not technological sophistication, but infrastructure speed.

- AI models train in months

- Data centres build in years

- Grids, permitting, and coordination take decades

This mismatch creates a strategic trap: regions approve technologies they cannot power.

Delays in:

- grid expansion

- transformer availability

- interconnectors

- storage deployment

- local generation

translate directly into:

- stalled industrial investment

- regional divergence

- external dependence

- loss of geopolitical leverage

In this context, energy policy becomes industrial policy—and industrial policy becomes security policy.

5. Decentralisation Is Not Ideology — It Is Geometry

Europe’s energy debate often treats decentralisation as a political preference. In reality, it is a question of geography and system design.

Europe is structurally different from the US:

- shorter distances

- denser population and industry

- strong regional economies

- high SME density

- advanced governance and standards capacity

These characteristics are not disadvantages. They are preconditions for decentralised energy systems.

Decentralised generation, storage, microgrids, and demand response:

- reduce transmission losses

- improve resilience

- deploy faster than centralised megaprojects

- integrate naturally with SMEs and regional ecosystems

- align with real-time optimisation under 4IR

Decentralisation does not replace central infrastructure. It relieves it.

Crucially, energy systems closer to demand shorten the feedback loop between innovation and deployment—a decisive advantage in a cyber-physical economy.

This is the balancing point European policymakers often miss: Europe’s economy and geography make it more competitive for decentralised energy adoption, provided governance and investment align with that reality.

6. REEs, Grids, and the Material Foundations of Power

Energy systems are physical systems. They are built from materials, components, and skills.

Transformers, inverters, motors, sensors, storage systems, and grid hardware depend on rare earths and critical minerals. These materials are not scarce geologically. What is scarce are the ecosystems that process, integrate, and manufacture them at scale.

Control over refining, component production, and grid hardware increasingly defines strategic autonomy. This is why competition over REEs and grid components has intensified: they sit at the intersection of energy, AI, defence, and industry.

Securing supply without rebuilding ecosystems produces dependence, not sovereignty.

7. Europe’s Constraint — and Its Opportunity

Europe’s core constraint is fragmentation:

- permitting regimes differ

- grid incentives diverge

- pricing lacks coherence

- fiscal capacity is uneven

- timelines are misaligned

In a world where speed determines sovereignty, fragmentation becomes a liability.

As Christine Lagarde has argued in recent interventions, even modest strengthening of internal EU growth materially increases Europe’s ability to absorb external shocks, including tariff escalation. A larger, more dynamic internal market cushions trade volatility by expanding domestic demand.

But internal growth is not abstract. It is energy-bound.

Sustained internal expansion requires grid capacity, generation build-out, permitting speed, and infrastructure coordination at continental scale. Without energy system expansion, growth cannot materialise; without growth, resilience weakens.

The shock-absorption capacity of the European market is therefore inseparable from its electricity system. Energy capacity is not only a climate instrument or industrial input — it is the foundation of macroeconomic resilience.

The implication is structural: resilience does not begin at the border. It begins with internal scale, coordination, and energy capacity.

But Europe has done large-scale coordination before—reconstruction, market-building, monetary integration. Energy now demands the same seriousness: shared planning, shared standards, pooled investment, and commitments insulated from electoral volatility.

Unlike the US, Europe does not need to retrofit a single oversized, fossil-heavy energy model across vast distances. Its geography and economic structure are better aligned with decentralised, resilient, low-loss systems—if policy recognises this.

In an era of tariff escalation and strategic decoupling, the size of a market matters less than its ability to power itself.

8. Urgency Without Panic

Europe’s position is not hopeless. But it is time-bound.

The window to:

- rebuild grids

- integrate decentralised energy

- anchor AI infrastructure

- restore industrial ecosystems

- retain geopolitical agency

is narrowing.

Delay compounds disadvantage. Once data centres, supply chains, and industrial clusters locate elsewhere, path dependency hardens.

The risk is not collapse. It is irrelevance through constraint: a Europe that regulates and consumes technologies it cannot host or scale.

9. The Strategic Choice

Europe faces a choice as consequential as any in the post-war period.

It can:

- treat energy as a market commodity

- manage AI as an intangible sector

- accept infrastructure delay as inevitable

- and drift into managed dependence

Or it can:

- treat energy as strategic infrastructure

- recognise AI as a physical system

- mobilise at continental scale

- and rebuild the foundations of sovereignty

Conclusion — Power Determines Scale

Firms require time. Ecosystems require coordination. Both require power.

AI, electrification, climate adaptation, and geopolitical fragmentation are converging into a single constraint: energy capacity and infrastructure speed. Without grids that expand, generation that scales, and material systems that hold, neither firms nor ecosystems can endure the transition.

In this environment, sovereignty is no longer an abstraction. It is the ability to power one’s own transformation.

Europe’s challenge is not to compete in AI narratives. It is to align organisation, ecosystems, and energy systems into a coherent architecture capable of scaling under constraint.

The trilogy began with firms under strain.

It ends with the recognition that scale is determined upstream.

Power — electrical, industrial, and political — is once again decisive.

Next Meso

For the full framework AI Energy Sovereignty Stress Test

AI Energy System Architecture Index

EU_Energy_Exposure_Sov_Data_Companion