Energy as the Operating System of Power ext

Geopolitics in an Energy-Bound System(Extended Background)

Archive Note — Extended Background Essay

This text expands the doctrine of Energy as the Operating System of Power through geopolitical, macro-financial, and European examples.

It should be read as a longer-form background essay rather than the canonical doctrine page.

Keynote

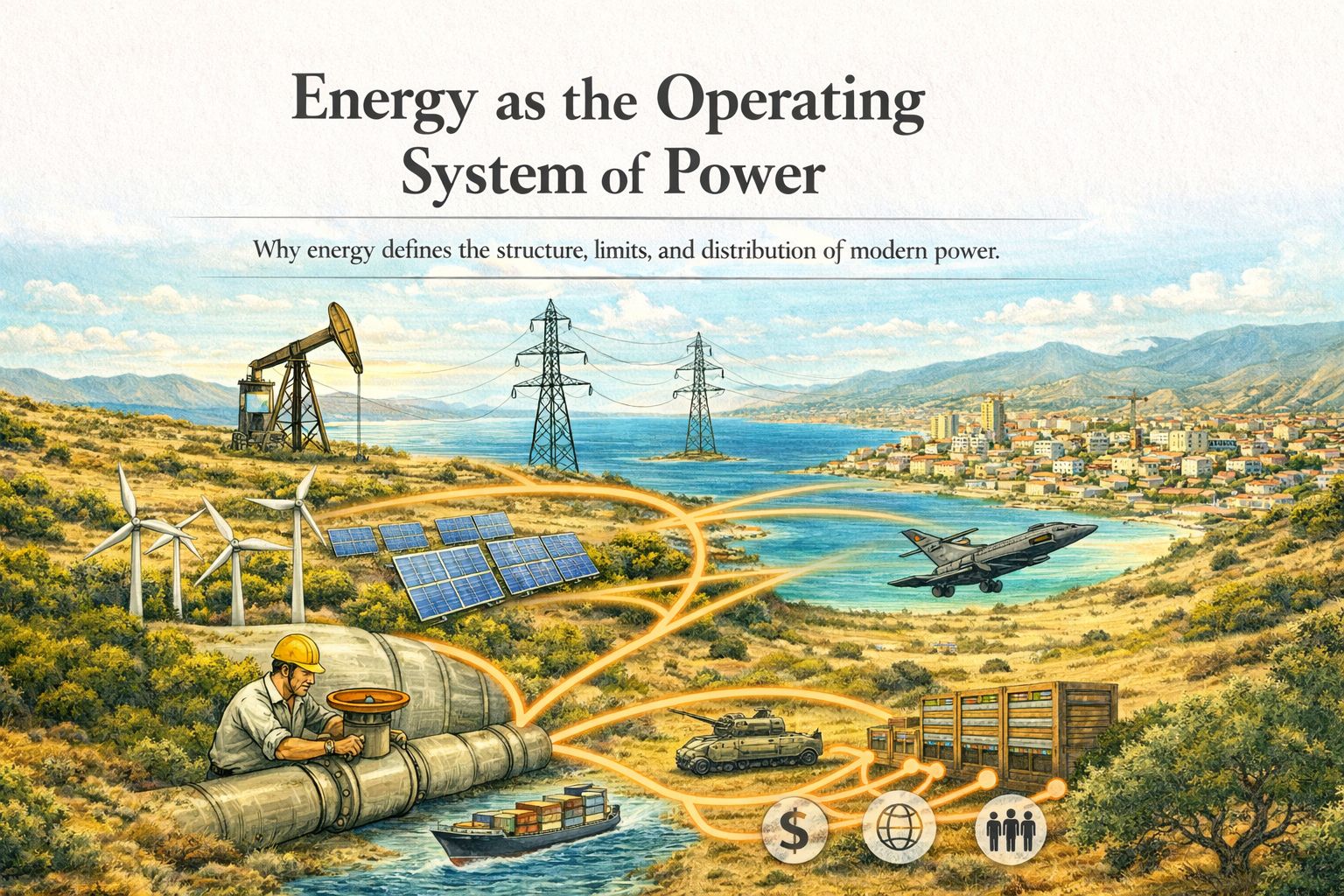

In the emerging global order, energy is no longer a background input into growth or security.

It has become the operating system through which power is organised, exercised, and constrained.

Energy availability, cost architecture, grid coordination, and shock absorption capacity now determine:

what can scale industrially

where AI infrastructure can concentrate

which monetary systems remain stable

where defence endurance is credible

whether sovereignty remains operational

These are not sectoral facts.

They are structural conditions.

Energy systems now shape outcomes across industry, finance, technology, and geopolitics. Control over energy architecture has become a decisive source of strategic advantage.

Introduction — The Return of Material Power

For decades, advanced economies operated under an implicit assumption: energy was abundant, scalable, and politically manageable.

Oil markets were deep and liquid.

Pipeline gas was treated as stable.

Electricity systems expanded incrementally.

Energy mattered, but often appeared as a background input rather than a

decisive constraint.

That assumption no longer holds.

Energy has re-emerged as the structuring layer of geopolitical power. It now functions as the operating system through which industrial scale, technological concentration, monetary stability, and defence credibility are organised.

Where energy depth exists, power compounds.

Where energy is externally priced, volatile, or

infrastructure-constrained, sovereignty becomes conditional.

This is not an ideological shift.

It is a material one.

As argued in Beyond Ideology, debates about deregulation, market reform, or industrial policy often misdiagnose the underlying constraint. Markets allocate within systems. They do not remove structural bottlenecks.

In an energy-bound system, infrastructure precedes ideology.

Energy as the Binding Constraint

Energy has moved from influencing growth to delimiting it.

Industrial electricity prices now diverge structurally across major powers. The United States has benefited from relatively lower industrial electricity prices through domestic shale integration and abundant generation capacity. China combines large-scale generation with coordinated grid expansion and coal-buffered baseload, limiting volatility even where import exposure remains. Europe, by contrast, has often priced electricity at the margin through imported gas, embedding external volatility directly into domestic industry.

These are not cyclical distortions.

They are structural asymmetries.

In electricity-mediated economies, energy determines:

whether semiconductor fabs can operate competitively

whether AI clusters can scale

whether electrified transport and heating can expand without inflationary spillovers

whether defence logistics remain sustainable

When energy is abundant and controllable, strategic flexibility persists. When it is externally priced or infrastructure-fragile, economic and geopolitical autonomy narrow.

Energy no longer merely shapes growth trajectories.

It sets the outer limits of capability.

The Geopolitical Reconfiguration of Energy

Global energy flows remain highly concentrated.

Maritime chokepoints continue to function as systemic vulnerabilities. LNG trade has become increasingly price-sensitive and logistics-dependent. A limited number of exporters, shipping routes, insurance channels, and regasification systems shape the security of supply.

The United States transformed its position over the past decade from major importer to significant exporter of oil and LNG. This shift turned exposure into leverage. Energy exports now reinforce geopolitical positioning, domestic flexibility, and alliance influence.

China remains import-dependent, particularly in oil. Yet it offsets exposure through long-term contracts, strategic reserves, diversified supply corridors, and coal fallback capacity. Vulnerability is partially compensated by architectural control.

Europe replaced pipeline dependence with global LNG exposure after 2022. While supply security improved in one sense, marginal pricing volatility increased. Gas shocks transmitted directly into electricity prices, inflation, fiscal strain, and industrial contraction.

Interdependence did not disappear.

It became more financialised, more volatile, and more strategically usable.

Energy shocks now transmit rapidly into macro-financial conditions. Inflation, monetary tightening, fiscal strain, and industrial weakness increasingly follow the architecture of energy exposure.

Finance follows energy architecture.

Technology as an Energy Multiplier

Technology does not dissolve energy limits.

It amplifies them.

Artificial intelligence converts electricity directly into decision advantage. Data centres, semiconductor fabrication, and industrial automation all require stable, high-volume, reliable electricity supply.

Compute is electricity embodied.

Where electricity is abundant, scalable, and competitively priced, digital advantage compounds. Where it is volatile or constrained, cost cascades upward into industry, defence, and fiscal stability.

Technological divergence increasingly follows electricity depth.

Europe’s Structural Exposure — The SME Factor

Europe’s vulnerability is not solely a matter of import dependence.

It is also structural.

A large share of European economic activity depends on small and medium-sized enterprises. Unlike vertically integrated industrial conglomerates, SMEs often cannot hedge energy exposure, secure long-term contracts, or relocate production easily.

Energy price volatility therefore transmits directly into:

margin compression

delayed investment

employment stress

regional fragility

In an SME-dominant system, marginal cost volatility becomes politically and economically destabilising.

Energy architecture therefore becomes a democratic stability variable.

The central question is not whether Europe should be more market-oriented or more interventionist.

It is whether the energy system is designed to dampen volatility or amplify it.

Architecture, not ideology, determines resilience.

Re-Materialisation of Power

For a period, power appeared increasingly immaterial: financial flows, services, regulation, digital platforms, and intellectual property.

That phase depended on stable fuel supply and relatively low energy volatility.

Energy shocks have revealed the physical substrate of modern power:

grids

LNG terminals

storage capacity

baseload generation

maritime insurance

transmission lines

digital optimisation layers

Industrial production, AI infrastructure, and financial stability all rest upon this material foundation.

Energy is not one sector among many.

It is the operating system beneath the economic and technological stack.

From Operating System to System Control

If energy is the operating system of power, sovereignty is the capacity to control that operating system.

As developed in Energy Sovereignty as System Control, sovereignty now rests on three capabilities:

operational control — absorbing shocks without systemic breakdown

architectural control — shaping pricing, integration, and infrastructure design

temporal control — expanding capacity at strategic speed

States lacking control over price transmission, grid integration, storage buffers, deployment timelines, and digital optimisation layers may retain formal sovereignty while losing operational autonomy.

Energy depth without architectural control produces

vulnerability.

Markets without coordination produce volatility.

Policy without infrastructure produces rhetoric.

Sovereignty is not insulation from interdependence.

It is position within it.

Conclusion — A Capacity-Determined Era

When energy is abundant, efficiency dominates.

When energy is constrained, capacity determines power.

We are in a capacity-determined era.

Energy now structures the geopolitical environment within which industry, AI, finance, and defence operate. The global system is reorganising around energy depth, grid scalability, and architectural control.

The implications—power concentration, alliance strain, and G2 consolidation—are not ideological outcomes.

They are material consequences.

Energy is the operating system of modern power.

Data Annex — Energy Geopolitics Snapshot

Oil

global oil demand remains around the 100 million barrels per day scale

maritime chokepoints remain critical to supply security

OPEC+ remains a major concentration point in global supply

Gas

LNG has become a central transmission mechanism in global gas trade

supply remains concentrated among a limited number of exporters

import-dependent regions remain exposed to external price formation

Electricity

data centres are now a material source of electricity demand

AI clusters create concentrated load growth

advanced semiconductor fabs require continuous high-load power

Macroeconomic Transmission

energy price shocks transmit into inflation

inflation feeds monetary tightening

tightening increases fiscal and industrial strain

vulnerability is amplified where energy is externally priced