Italy — Industrial Capacity Under Energy Constraint

System Navigation: Mediterranean System Navigation

Keynote

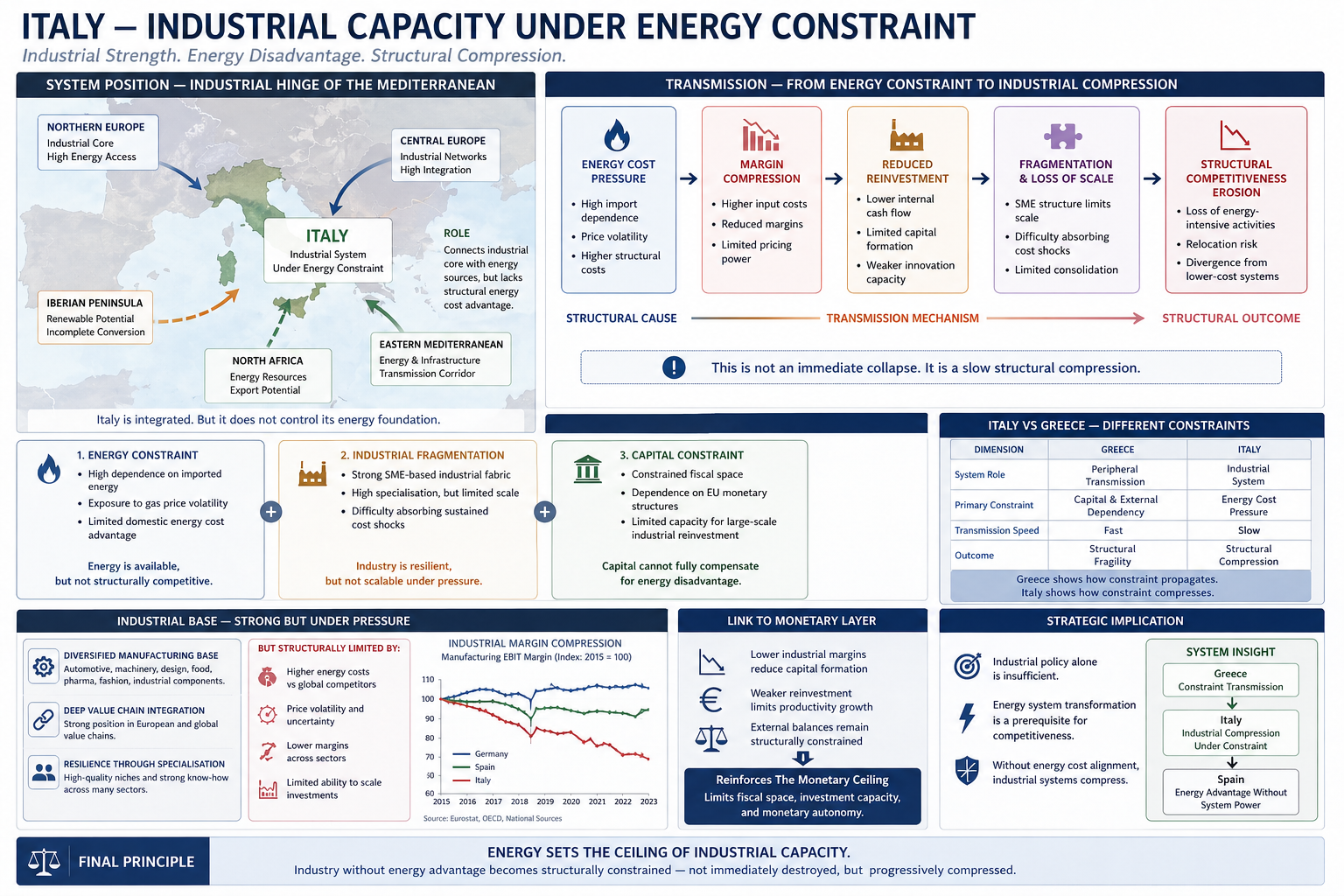

Italy occupies a structurally distinct position within the European system.

It is not a peripheral economy.

It is an industrial economy operating under energy

constraint.

Unlike Greece, where constraint transmits primarily through capital dependency and external exposure, Italy demonstrates a different systemic dynamic:

Constraint operating directly on an existing industrial ecosystem.

This makes Italy a critical case within an Energy-Bound System.

Italy reveals not how systems fail to build industrial capacity, but how existing industrial ecosystems become progressively compressed when energy systems, infrastructure, capital, and industrial scaling cease to align structurally.

The Italian case therefore represents a broader European problem:

industrial capacity without a fully competitive energy foundation.

System Position — Industrial Layer Under Constraint

The system operates through a hierarchical chain:

Energy → Industry → Capital → Currency → Sovereignty

Italy sits primarily at the industrial layer of this chain.

The country retains significant structural advantages:

substantial manufacturing capacity

integration into European industrial value chains

advanced regional production clusters

specialised export-oriented industries

dense networks of SMEs and industrial ecosystems

Italy therefore remains one of Europe’s most important industrial systems.

However, these strengths operate within an increasingly constrained energy environment:

energy costs remain structurally elevated relative to major competitors

the system remains exposed to imported energy pricing

industrial scaling capacity remains uneven

monetary and fiscal flexibility remain constrained

As a result:

industrial capacity exists, but the energy foundation beneath it remains structurally unstable.

Core Mechanism

Industrial Systems Require Energy Cost Stability

Industrial competitiveness is not determined solely by:

labour cost

technological capability

productivity

market access

Industrial competitiveness increasingly depends upon:

energy cost, energy stability, infrastructure integration, and long-term scalability

This condition becomes even more important under conditions of industrial electrification, automation, AI integration, and compute-intensive production systems.

In Italy:

energy costs remain structurally elevated

electricity price volatility transmits directly into industrial production costs

industrial margins remain under sustained pressure

reinvestment capacity becomes progressively constrained

This produces a structural condition in which:

industrial capacity persists, but operates under continuous structural compression.

Structural Characteristics

Italy’s industrial system reflects three interacting structural constraints.

1. Energy Constraint

Italy remains heavily exposed to imported energy dependency.

The system experiences:

exposure to gas price volatility

elevated electricity costs

limited domestic low-cost energy advantage

uneven infrastructure integration

Energy therefore remains physically available within the system, but it does not provide a sufficiently competitive cost foundation for long-term industrial scaling.

Energy availability does not automatically produce energy competitiveness.

2. Industrial Fragmentation

Italy possesses a dense and historically resilient industrial ecosystem.

This ecosystem is built around:

regional manufacturing clusters

SME-based industrial networks

specialised production systems

export-oriented industrial districts

This structure provides flexibility and resilience.

However, fragmentation also creates structural limitations:

limited economies of scale

uneven access to capital

lower shock absorption capacity

difficulty sustaining large-scale reinvestment during prolonged energy stress

As a result:

the industrial ecosystem remains resilient, but structurally difficult to scale under sustained cost pressure.

3. Capital Constraint

Industrial systems require continuous reinvestment.

However, Italy operates within a constrained monetary and fiscal framework.

The system therefore experiences:

constrained fiscal space

dependence on European monetary structures

limited strategic industrial financing capacity

uneven capital allocation toward infrastructure transformation

This reduces the system’s ability to offset energy disadvantage through industrial policy alone.

Capital cannot fully compensate for structural energy disadvantage.

Transmission — From Energy Constraint to Industrial Compression

Energy constraint propagates through the industrial system via a clear structural transmission chain:

Energy cost pressure

→ industrial margin compression

→ reduced reinvestment capacity

→ fragmentation and reduced scaling ability

→ industrial competitiveness erosion

→ long-term structural compression

This process does not produce immediate industrial collapse.

Instead, it produces:

slow structural weakening within the industrial base itself.

Industrial Ecosystems and the New Competitive Layer

The Italian case becomes increasingly important within the emerging AI–energy transition.

Industrial competitiveness is no longer determined solely by manufacturing output.

It increasingly depends upon the alignment of:

energy systems

industrial ecosystems

compute infrastructure

automation capacity

logistics integration

capital coordination

Advanced manufacturing, AI-enabled production systems, industrial automation, and compute-intensive infrastructure all require:

stable, scalable, and competitively priced electricity systems

As the global system shifts toward energy-intensive compute architectures and electrified industrial production, industrial ecosystems operating under structurally elevated energy costs face increasing long-term competitive pressure.

This places Italy within a wider systemic divergence emerging across the global economy.

Comparison — Italy vs Greece

| Dimension | Greece | Italy |

|---|---|---|

| System role | Peripheral transmission | Industrial ecosystem |

| Primary constraint | Capital dependency and external exposure | Energy cost pressure |

| Transmission speed | Faster | Slower |

| Core dynamic | Structural fragility | Structural compression |

| System effect | Transmission instability | Industrial erosion |

Greece demonstrates how constraint propagates through dependency.

Italy demonstrates how constraint compresses existing industrial capacity.

System Consequence

Italy does not lose its industrial base immediately.

Instead, the system experiences:

gradual erosion of competitiveness

relocation pressure on energy-intensive industries

reduced long-term industrial scaling capacity

lower reinvestment intensity

increasing divergence from lower-cost industrial systems

This divergence becomes increasingly important under conditions of:

industrial electrification

AI-enabled manufacturing

compute-intensive infrastructure scaling

global energy competition

Industrial presence without structural energy advantage cannot sustain long-term system power.

Link to the Monetary Layer

Industrial compression feeds directly into the monetary layer of the system.

When industrial margins weaken:

capital formation weakens

reinvestment slows

productivity growth becomes constrained

external balances remain under pressure

This reinforces:

the Monetary Ceiling

Even within a major industrial economy, energy constraint limits:

fiscal flexibility

industrial investment capacity

infrastructure transformation

monetary autonomy

The result is a structurally constrained industrial system operating within a constrained monetary architecture.

Mediterranean Position — Industrial Hinge Within the Conversion Layer

Italy occupies a unique structural position within the Mediterranean system.

It functions simultaneously as:

an industrial node

a logistics corridor

an infrastructure interface

a Mediterranean conversion hinge

Italy connects:

Northern European industrial systems

Mediterranean energy corridors

regional infrastructure flows

industrial manufacturing networks

The country therefore occupies a potential conversion position between:

Mediterranean energy systems and European industrial demand

However:

connection does not automatically produce strategic control or conversion capacity.

The absence of fully aligned:

energy systems

industrial infrastructure

compute capacity

capital coordination

long-term industrial strategy

limits Italy’s capacity to convert its structural position into sustained system power.

Strategic Implication

Italy demonstrates a central principle of the Energy-Bound System:

industrial capacity alone cannot compensate for structural energy disadvantage.

This carries several strategic implications.

Industrial policy alone is insufficient.

Long-term industrial competitiveness increasingly depends upon:

energy system transformation

electricity cost competitiveness

infrastructure integration

compute and industrial coordination

ecosystem-scale reinvestment

Without these alignments:

industrial systems progressively compress under energy constraint.

System Insight

Italy represents the second layer of the Mediterranean system structure:

Greece → constraint transmission

Italy → industrial compression under constraint

This prepares the system for the next structural case:

Spain — Energy Advantage Without Full System Conversion

Final Principle

Energy establishes the structural ceiling of industrial capacity.

Industrial ecosystems operating without competitive energy foundations do not immediately disappear.

They become progressively compressed over time through cost pressure, fragmentation, and declining scalability.

Italy therefore represents more than an industrial economy under pressure.

It represents a broader European structural problem:

the incomplete alignment of energy systems, industrial ecosystems, infrastructure, compute capacity, and capital allocation into a coherent architecture of long-term system power.

In this sense, Italy functions simultaneously as:

a compressed industrial system

and a strategic hinge within the emerging Mediterranean energy–compute architecture

References — Italy, Energy, and Industrial Constraint

These sources support the structural dynamics described above.

They do not define the framework.

They validate its mechanisms.

Energy Systems and Cost Structure

International Energy Agency — Italy Energy Policy Review

European Commission — Energy Prices and Costs in Europe

Ember — European Electricity Review

Industrial Structure and Competitiveness

OECD — Italy Economic Surveys

World Bank — Manufacturing and Value Chain Integration Data

Confindustria — industrial reports on competitiveness and energy cost pressures

Monetary and Structural Constraint

European Central Bank — monetary policy and transmission reports

International Monetary Fund — Italy Article IV Consultations

Energy–Industry–Compute Dynamics

Bruegel — European energy crisis and industrial competitiveness

Centre for European Policy Studies — industrial policy and energy transition

International Energy Agency — electricity demand and industrial electrification

Cross-Reference Reading Architecture — Mediterranean System

From Energy Constraint to System Power in an Energy-Bound Europe

SYSTEM POSITION

This analysis sits within the Mediterranean conversion layer:

Energy → Industry → Compute → Capital → Sovereignty

Italy represents:

industrial capacity operating under structural energy constraint

I. FOUNDATIONS — System Logic

The system is structured by energy, infrastructure, and scaling capacity.

Extended Foundations

II. GLOBAL DYNAMICS — Constraint Formation

How the global system produces structural divergence

III. EUROPE — STRUCTURAL CONSTRAINT

Europe as a constrained industrial and monetary system

IV. MEDITERRANEAN — SYSTEM ARCHITECTURE

The Mediterranean as an energy–industry–compute interface

V. COUNTRY SYSTEMS — Comparative Layer

Greece — Constraint Transmission

Italy — Industrial Compression

- Italy — Industrial Capacity Under Energy Constraint (this article)

Planned (Evidence Layer)

- [Italy — Energy–Industrial Transmission Under Constraint]

Planned (Investor Layer)

Spain — Incomplete Conversion

Planned (Evidence Layer)

- Spain — Energy Advantage and Incomplete Transmission #review #mediterannean

Planned (Investor Layer)

- Spain — Energy Arbitrage Without Full Capture ??? #review #mediterannean

Spain — Energy Arbitrage and Capital Allocation

VI. ENERGY–COMPUTE LAYER — Future Scaling Constraint

Where future industrial competitiveness will increasingly be decided

VII. EVIDENCE — System Validation

Data, transmission mechanisms, and structural exposure

VIII. INVESTOR LAYER — Capital Allocation

Where structural divergence becomes actionable

Mediterranean Allocation

IX. SYSTEM SYNTHESIS (Planned)

Mediterranean — From Constraint to System Power

Europe — From Industrial Core to Constrained System

Energy–Industry–Capital Misalignment in Europe

Final Orientation

The system is not ultimately defined by individual economies.

It is defined by the degree to which energy systems, industrial ecosystems, compute infrastructure, and capital allocation align—or fail to align.

Greece demonstrates transmission.

Italy demonstrates industrial compression.

Spain demonstrates incomplete conversion.

Together, they define the structural logic of the Mediterranean system within an Energy-Bound Europe.