GEIYV — Phase 1 Asset Map (Investor Appendix)

From system assets to investable yield

Framework Context

This appendix operationalises GEIYV by identifying deployable asset clusters and translating them into investable return structures.

System Navigation: Mediterranean System Navigation

→ Investor Framework — Capital Allocation in an Energy-Bound System

→ Financial–Physical Asymmetry in an Energy-Bound System

→ Greece — Peripheral Transmission Under Constraint

→ Energy-Bound System

Core Principle

Phase 1 does not create assets.

It aggregates, structures, and aligns existing system capacity into investable form.

Structural Context

The Greek energy system already contains:

operational renewable capacity

regulated infrastructure

pipeline storage assets

strategic corridor positions

However:

Financial capital and physical system capacity remain structurally misaligned.

This reflects a broader condition:

Financial–physical asymmetry — where assets exist, but are not structured into investable scale.

I. Asset Universe (Indicative Ranges)

1. Renewable Generation (Operational Base)

Solar — Central & Northern Greece

Capacity:

→ 200–400 MW (aggregatable portfolio)Asset type:

→ multi-site PV parks (10–100 MW units)Status:

→ operational, revenue-generatingRevenue:

→ FiT / CfD / PPA-backedYield:

→ 5–7% unlevered

Wind — Evia / Thrace / Aegean

Capacity:

→ 300–500 MW (clustered)Capacity factor:

→ 25–35%Constraint:

→ grid congestion / curtailmentYield:

→ 6–8% unlevered

2. Grid Infrastructure (Constraint Layer)

Interconnections & Transmission

Assets:

→ Cyclades / Crete interconnections

→ mainland reinforcementType:

→ regulated infrastructureReturn profile:

→ 4–6% regulated / quasi-regulated

System Role

Grid capacity defines the ceiling of renewable deployment, compute scaling, and system integration.

3. Storage (Pipeline Layer)

Battery Systems

Capacity:

→ 100–200 MW initial integrationStatus:

→ national tender / pipelineRevenue:

→ capacity payments + balancing + arbitrageExpected return:

→ 6–9% (post-structuring)

4. Corridor Assets (Strategic Layer)

Northern Greece Energy Node

Assets:

→ LNG-linked infrastructure

→ cross-border electricity systemsFunction:

→ European energy entry pointCurrent condition:

→ transit without full value capture

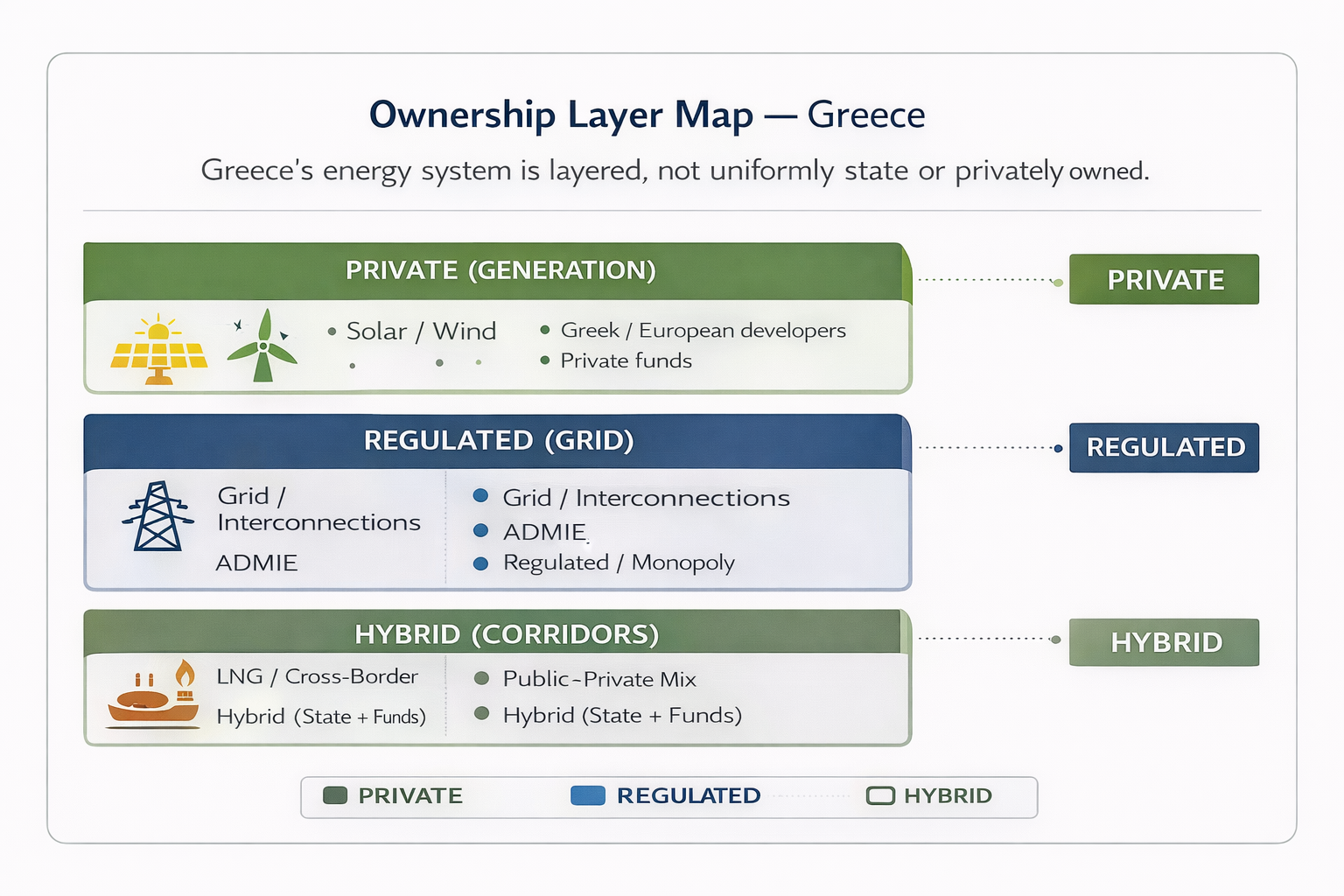

II. Ownership Structure (System Reality)

The Greek energy system is structurally layered:

Generation — Primarily Private

solar and wind owned by:

domestic developers

European utilities

infrastructure funds

→ fragmented ownership

Grid — Regulated / State-Controlled

transmission and interconnections

monopoly / regulated returns

→ system-critical layer

Storage — Private + Supported

early-stage private developers

EU-supported frameworks

→ emerging growth layer

Corridors — Hybrid

public–private ownership

international capital participation

→ strategic but under-monetised

Core Constraint

Ownership is not the limitation.

Fragmentation prevents investability.

III. Entry Mechanisms (Capital Alignment Layer)

GEIYV enables structured capital entry through:

aggregation of operating SPVs

minority or controlling stakes in portfolios

refinancing of existing assets

co-investment alongside developers

integration of pipeline assets into a unified platform

Structural Shift

From project-level exposure → to platform-level allocation.

This is the mechanism through which:

financial capital is aligned with physical system capacity.

IV. Illustrative Phase 1 Platform

Aggregated Portfolio

Solar: ~300 MW

Wind: ~400 MW

Grid: 1–2 major assets

Storage: ~150 MW pipeline

Scale

- indicative asset base:

→ €1–2 billion equivalent platform

Portfolio Characteristics

brownfield + late-stage assets

diversified energy mix

integrated infrastructure exposure

V. Return Structure (Investor View)

Revenue Composition

60–70% contracted (PPAs / regulated)

20–30% capacity-linked / semi-contracted

0–10% merchant exposure

Target Returns

Core yield: 4–6%

Blended yield: 5–7%

Optimised: 6–8%

Duration

asset life: 20–30 years

contracted visibility: 10–20 years

VI. Financial–Physical Transformation

Without Structure

fragmented ownership

project-level risk concentration

volatile and non-scalable returns

limited institutional access

With GEIYV

portfolio aggregation

diversified risk exposure

contracted revenue base

institutional-grade yield profile

Mechanism

GEIYV converts physical system assets into investable financial structures.

VII. Risk Decomposition

Energy Price Risk

→ mitigated via PPAs / regulation

Grid Constraint Risk

→ mitigated via integrated grid exposure

Construction Risk

→ phased integration + public capital layer

Regulatory Risk

→ EU-aligned frameworks + long-duration visibility

VIII. Capital Structure (Indicative)

Public / EU (10–20%)

→ guarantees / first-lossInstitutional (50–70%)

→ pensions / insurersPrivate / strategic (10–30%)

→ sovereign wealth funds / family offices

Result

Risk is aligned with capital absorption capacity.

IX. Structural Return Driver

Returns are driven by:

energy cost reduction

infrastructure integration

system stability

Transmission Logic

Energy → Infrastructure → Cost Stability → Capital Formation

X. Strategic Relevance

This structure addresses:

capital misallocation

energy cost volatility

infrastructure gaps

external dependency

And supports:

SME competitiveness

domestic reinvestment

system resilience

XI. Monetary Link

This structure reduces exposure to:

Energy → Inflation → Capital → Currency

as defined in:

→ Energy

Constraint and the Monetary Ceiling

XII. Investor Positioning

This is:

not venture

not speculative

not purely financial

It is:

system-aligned infrastructure exposure under structural constraint

XIII. Key Insight

Greece does not lack assets.

It lacks structure, aggregation, and investability.

XIV. Bottom Line

The opportunity is not asset creation.

It is asset structuring.