Italy — Industrial Structure Deep Dive

Resilience, Fragmentation, and Constraint in an Energy-Bound System

Keynote

Italy possesses one of the most sophisticated industrial systems in Europe.

It combines advanced manufacturing capabilities, highly specialised production, deeply embedded regional ecosystems, and dense networks of industrial coordination.

However, this industrial capacity does not translate into sustained system-level power.

This outcome is not the result of insufficient capability.

It results from the interaction between energy constraint, industrial fragmentation, capital limitations, incomplete compute integration, and weak platform control.

In an energy-bound system, industrial strength alone is not sufficient to generate durable strategic power.

Industrial systems must also be aligned with:

stable and competitively priced energy

scalable infrastructure

compute capacity

digital coordination systems

technological ecosystems

and capital capable of supporting long-term expansion

Italy therefore represents a distinct structural condition within the European system:

a high-capacity industrial ecosystem operating under persistent structural constraint and incomplete system conversion

System Navigation

This article extends the Mediterranean diagnostic layer by analysing the internal structure of Italy’s industrial system under conditions of energy, capital, and technological constraint.

It should be read alongside:

– Italy —

Industrial Capacity Under Energy Constraint

– Italy

— Energy–Industrial Transmission Under Constraint

– Spain — Iberian

Constraint

– Greece — Capital

Allocation Problem

– France

— Nuclear Continuity and Hybrid Infrastructure Sovereignty

– Mediterranean System Architecture — Western, Eastern, and Hinge Nodes

And within the broader system:

– EU Systemic

Asymmetry

– Europe — The

Missing Conversion Layer

– AI–Energy–Cost

Chasm

– Energy–Industry–Compute

Stack

– Industrial

Ecosystems — Cross-Panel Index

– Digital

Sovereignty Index

System Position

Italy occupies a central position within the European industrial system.

It sits between the energy-constrained Mediterranean periphery and the industrial and financial core of Northern Europe.

Within the broader system chain:

Energy → Infrastructure → Compute → Ecosystems → Capital → Sovereignty

Italy is strongly positioned in industrial production and manufacturing ecosystems, but less aligned in the surrounding layers that increasingly determine long-term system power.

Its condition reflects a structural imbalance.

Industrial capability is advanced and resilient, but energy remains externally exposed and volatile. Capital is fragmented and constrained, and integration into compute infrastructure, software ecosystems, platform layers, and digital coordination systems remains incomplete.

As a result, Italy sustains industrial production, but does not fully convert industrial capability into system-level power.

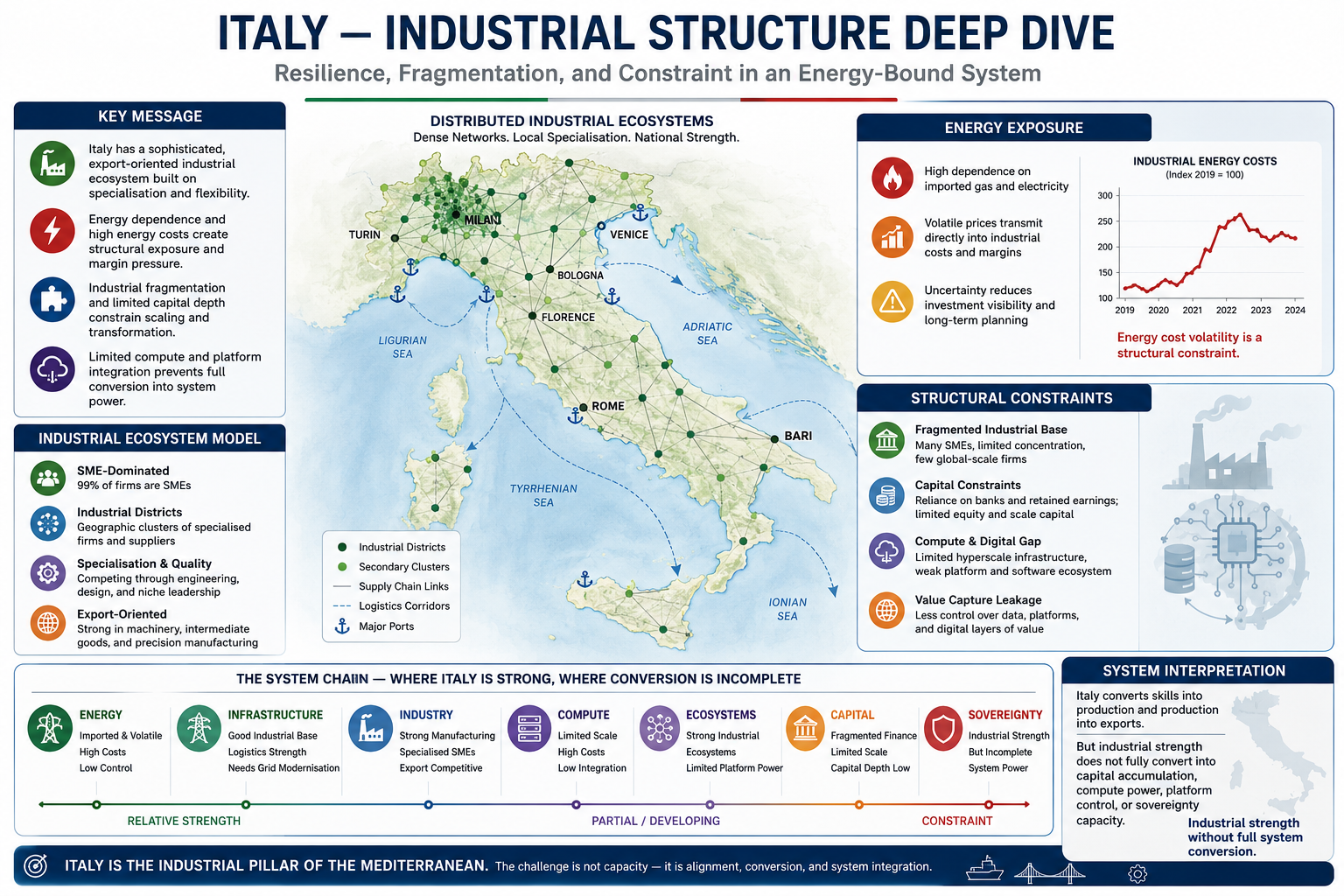

I. The Structure of Italian Industry

Italy’s industrial system is defined by a distinctive organisational model based on distributed industrial ecosystems rather than large-scale concentration.

Small and medium-sized enterprises form the core of this structure. These firms are highly specialised, export-oriented, and deeply embedded within regional production networks and supply chains.

Production is organised geographically into industrial districts, particularly across Northern Italy. These districts concentrate suppliers, technical knowledge, engineering capability, specialised labour, and production infrastructure within dense local ecosystems.

This organisational structure enables high levels of flexibility, resilience, technical specialisation, and adaptive manufacturing capacity.

Firms are often able to respond rapidly to changing demand conditions, shifting market requirements, and supply-chain disruptions.

Italy’s export profile reflects this structure.

The country remains a major exporter of machinery, intermediate industrial goods, precision manufacturing products, and specialised industrial systems.

Its competitiveness is based less on scale and more on:

quality

flexibility

technical depth

specialised manufacturing capability

and ecosystem density

However, this structure also imposes systemic limitations.

The prevalence of small firms leads to fragmented ownership structures and limited industrial concentration.

This fragmentation reduces the capacity for:

large-scale capital accumulation

vertically integrated industrial scaling

platform development

strategic technology coordination

and long-term industrial consolidation

As a result, Italy possesses strong industrial density, but weaker systemic concentration.

II. Energy Exposure and Cost Transmission

Italy’s industrial system is structurally exposed to energy costs due to its reliance on imported energy.

Historically, a significant share of gas supply was linked to Russian flows. This dependence created vulnerability to external shocks, including supply disruptions, geopolitical instability, and extreme price volatility.

In an energy-bound system, energy costs transmit directly into industrial structure.

Higher electricity and gas prices increase production costs, compress industrial margins, reduce investment visibility, and weaken long-term competitiveness, particularly in energy-intensive sectors.

However, the effect extends beyond immediate profitability.

Volatile energy systems undermine the long-term coordination mechanisms required for industrial scaling, compute deployment, infrastructure investment, and technological upgrading.

Under these conditions, firms prioritise operational resilience over strategic expansion.

This creates a broader system outcome.

Industrial systems remain operational, but become progressively constrained in their ability to scale, consolidate, digitise, and transform.

System Transmission Map — Distributed Industry and Energy Alignment

III. Industrial Ecosystems and Resilience

Despite these constraints, Italy’s industrial system remains highly resilient.

This resilience emerges primarily from the structure of its industrial ecosystems.

Small and medium-sized enterprises are able to adapt production processes, reconfigure supplier relationships, and respond rapidly to changes in cost conditions and market demand.

Industrial districts reinforce this flexibility through:

dense supplier coordination

knowledge spillovers

informal industrial networks

technical specialisation

and geographically concentrated expertise

In many sectors, competition is based on engineering capability, specialised production, and technical quality rather than low-cost mass manufacturing alone.

This reduces vulnerability to certain forms of price competition.

However, resilience at the ecosystem level does not automatically produce system-level power.

Italy demonstrates strong adaptive capability at the microeconomic level, but limited scaling capability at the macro-system level.

The industrial ecosystem can absorb shocks efficiently.

It cannot easily expand into dominant platform, compute, or capital architectures.

IV. Fragmentation and Capital Constraints

The limitations of the industrial structure become more pronounced at the level of capital formation.

Italy exhibits a lower degree of industrial concentration than Germany and fewer globally dominant industrial firms.

It possesses:

less vertical integration

weaker capital-market depth

reduced large-scale equity financing

and more limited strategic consolidation mechanisms

The financial structure of Italian firms reinforces this condition.

Firms rely heavily on:

bank financing

retained earnings

family ownership structures

and regional financial systems

rather than deep capital markets and large-scale institutional investment.

As a result, firms often face constrained access to long-duration growth capital.

This reduces their capacity to invest in:

technological upgrading

compute integration

automation

artificial intelligence systems

software coordination layers

and long-term industrial transformation

Capital fragmentation therefore reinforces industrial fragmentation.

It constrains scaling, consolidation, technological integration, and strategic investment across the wider system.

V. Missing Layers — Compute, Platforms, and Digital Coordination

The structural constraint extends beyond manufacturing into the digital and technological layers of the system.

Italy is not a primary hub for hyperscale data centres, large-scale AI infrastructure, or dominant cloud ecosystems.

This condition reflects the interaction between:

energy cost instability

infrastructure limitations

fragmented capital

and weaker integration into global digital ecosystems

As industrial systems increasingly integrate artificial intelligence, industrial software, cloud coordination, machine learning systems, and data-driven optimisation, compute infrastructure becomes part of industrial competitiveness itself.

Industrial capability can no longer be separated from digital coordination capacity.

This creates a major structural challenge for Italy.

Although the country maintains strong manufacturing ecosystems, it captures a smaller share of:

platform control

software ecosystems

industrial data value

AI infrastructure

and digital scaling dynamics

Italian firms often operate inside global supply chains without controlling the surrounding digital architectures through which value increasingly accumulates.

As a result, industrial production generates value, but substantial portions of digital capture, data coordination, and platform scaling occur outside the domestic system.

This limits Italy’s ability to move upward within an increasingly AI-driven industrial environment.

VI. System Interpretation

Italy should not be understood as an industrially weak economy.

It is a structurally capable but systemically constrained industrial ecosystem.

It successfully converts:

skills into production

production into exports

and industrial ecosystems into resilience

However, it struggles to convert:

production into large-scale capital accumulation

industrial ecosystems into platform ecosystems

and industrial capability into sovereignty capacity

This produces a defining system condition:

industrial strength without full system conversion

Strategic Role in the Mediterranean System

Italy represents the industrial pillar of the Mediterranean system.

Within the wider Mediterranean architecture:

Spain provides energy potential but lacks full transmission and conversion integration

Italy provides industrial capacity but lacks energy alignment, compute integration, and capital scaling

Greece reflects capital allocation constraints, financial fragmentation, and external dependency

Together, these conditions reveal a broader structural pattern.

The Mediterranean already contains many of the foundational layers required for long-term strategic autonomy:

energy

infrastructure

industrial ecosystems

logistics corridors

maritime connectivity

compute potential

and capital flows

However, these layers remain geographically fragmented, institutionally disconnected, and insufficiently integrated into a coherent system architecture.

The core Mediterranean challenge is therefore not the absence of capability.

It is incomplete system integration and weak conversion capacity.

Strategic Implications

Italy’s constraints are structural, but they are not permanent.

Improvement depends on alignment across multiple system layers.

First, energy alignment is required.

This includes access to stable and competitively priced electricity, stronger grid integration, infrastructure expansion, and deeper integration into European and Mediterranean energy systems.

Second, industrial scaling mechanisms must be strengthened.

This includes enabling firms to move beyond fragmented structures where appropriate and supporting larger industrial coordination frameworks capable of sustaining long-term technological transformation.

Third, compute and digital integration must expand.

Industrial ecosystems increasingly depend on:

AI-enabled production

industrial software

cloud coordination

automation

data infrastructure

and compute scalability

Without these layers, industrial systems risk remaining operationally capable but strategically subordinated.

Fourth, capital deepening is necessary.

This requires stronger capital markets, improved access to equity financing, long-term investment coordination, and mechanisms capable of supporting industrial and technological scaling.

Without alignment across these layers, structural constraints will persist.

Final Synthesis

Italy demonstrates a central principle of the energy-bound system:

industrial capability alone does not generate system power

System power emerges only when:

energy systems

industrial ecosystems

compute infrastructure

digital coordination layers

capital formation

and platform architectures

are aligned within a coherent strategic system.

When this alignment remains incomplete, systems can remain productive, resilient, and technologically capable, but they cannot scale efficiently into durable sovereignty capacity.

Italy therefore represents a structurally constrained industrial ecosystem:

capable of sustained production

resilient under pressure

but limited in conversion, scaling, and strategic expansion

System Continuity

Italy’s condition connects directly to the broader European system.

It highlights the widening gap between:

industrial capability

energy alignment

compute integration

capital formation

and system-level sovereignty capacity

across Europe’s wider architecture.

This leads directly to the next analytical layer:

→ Europe — The Missing Conversion Layer

Where the central question becomes whether Europe can align energy, infrastructure, industry, compute, ecosystems, and capital into a functioning system of strategic power.