Energy Constraint and the Monetary Ceiling

The Energy → Industry → Trade → Currency Transmission Chain

Doctrine — EU Sovereignty Panel

In an energy-bound system, persistently higher marginal energy costs impose a structural ceiling on currency strength by compressing industry, investment, and external balances over time.

![]()

Transmission Mechanism

Energy systems shape industrial competitiveness, capital allocation, and ultimately the durability of monetary systems.

Persistent energy cost divergence propagates through the real economy:

Energy cost divergence

→ industrial margin compression

→ reduced reinvestment and industrial relocation

→ trade balance deterioration

→ currency vulnerability

Monetary systems ultimately reflect the underlying structure of production and trade.

When energy costs structurally weaken industry and external balances, monetary strength becomes constrained regardless of monetary policy settings.

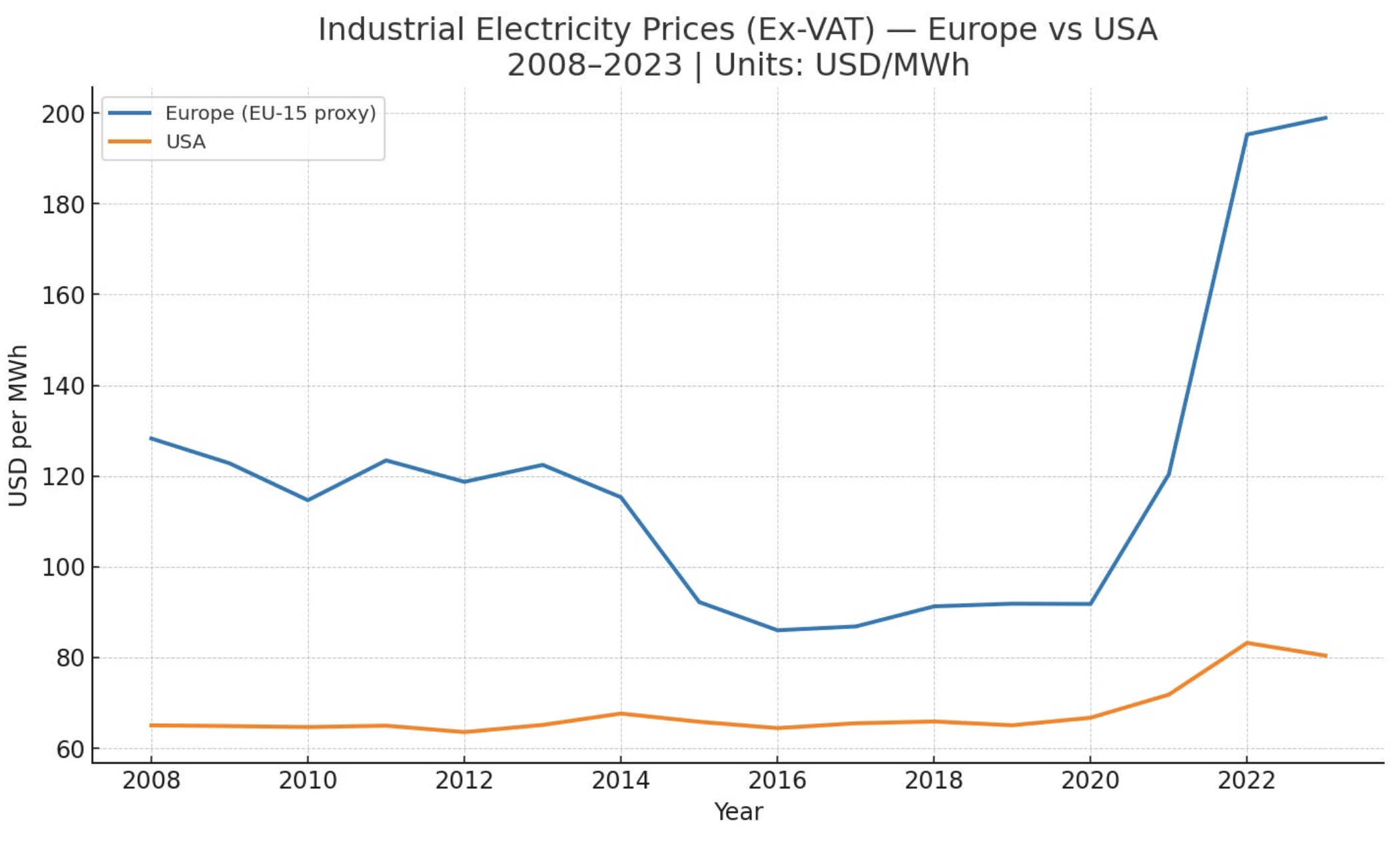

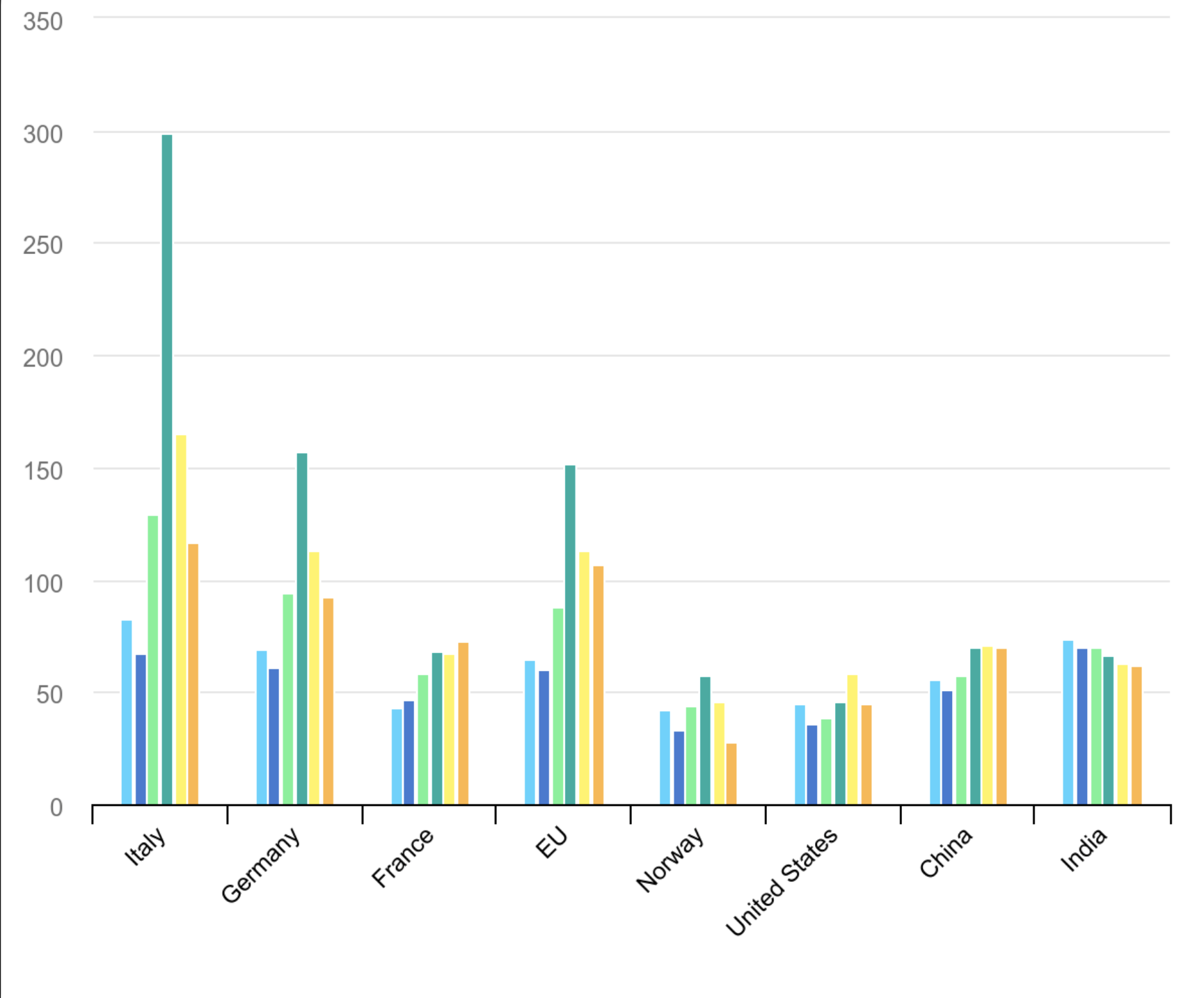

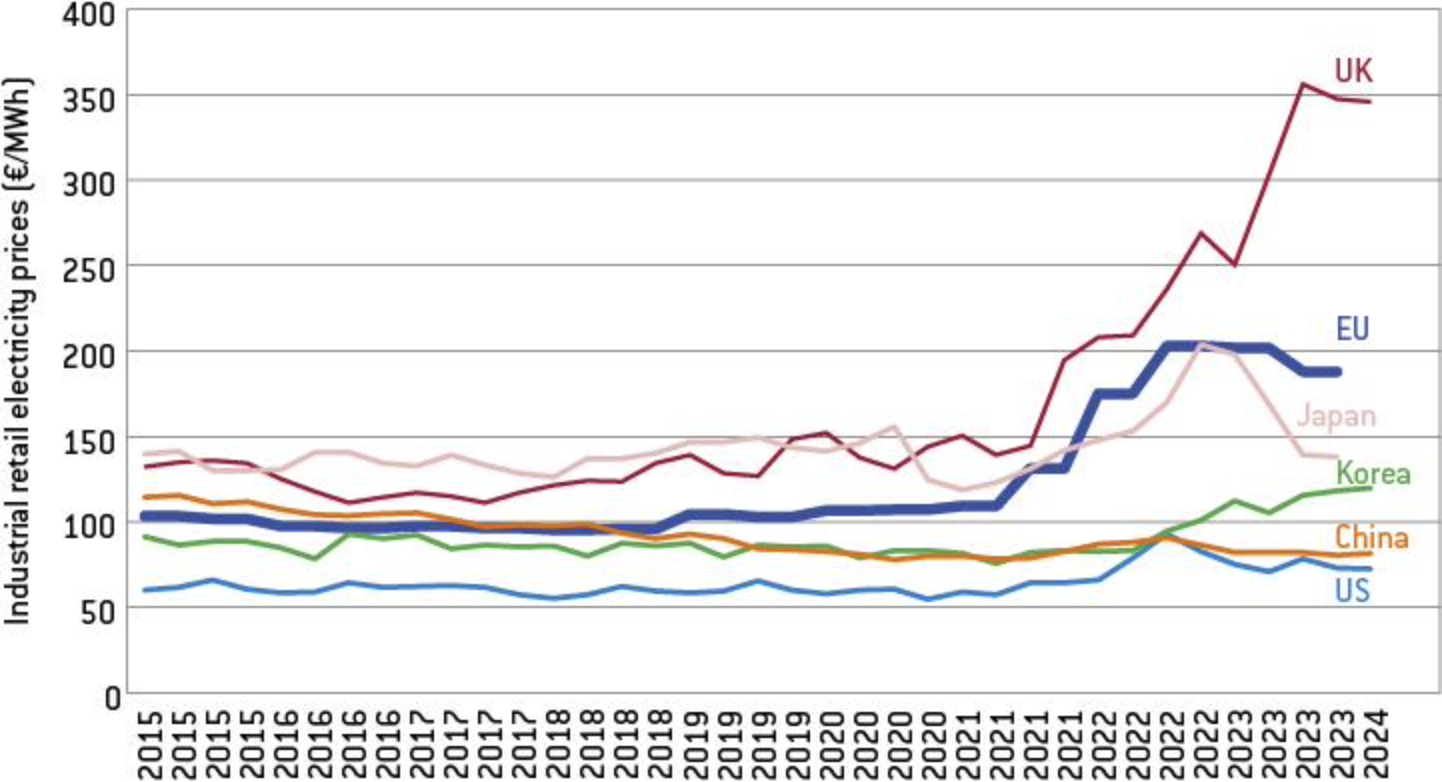

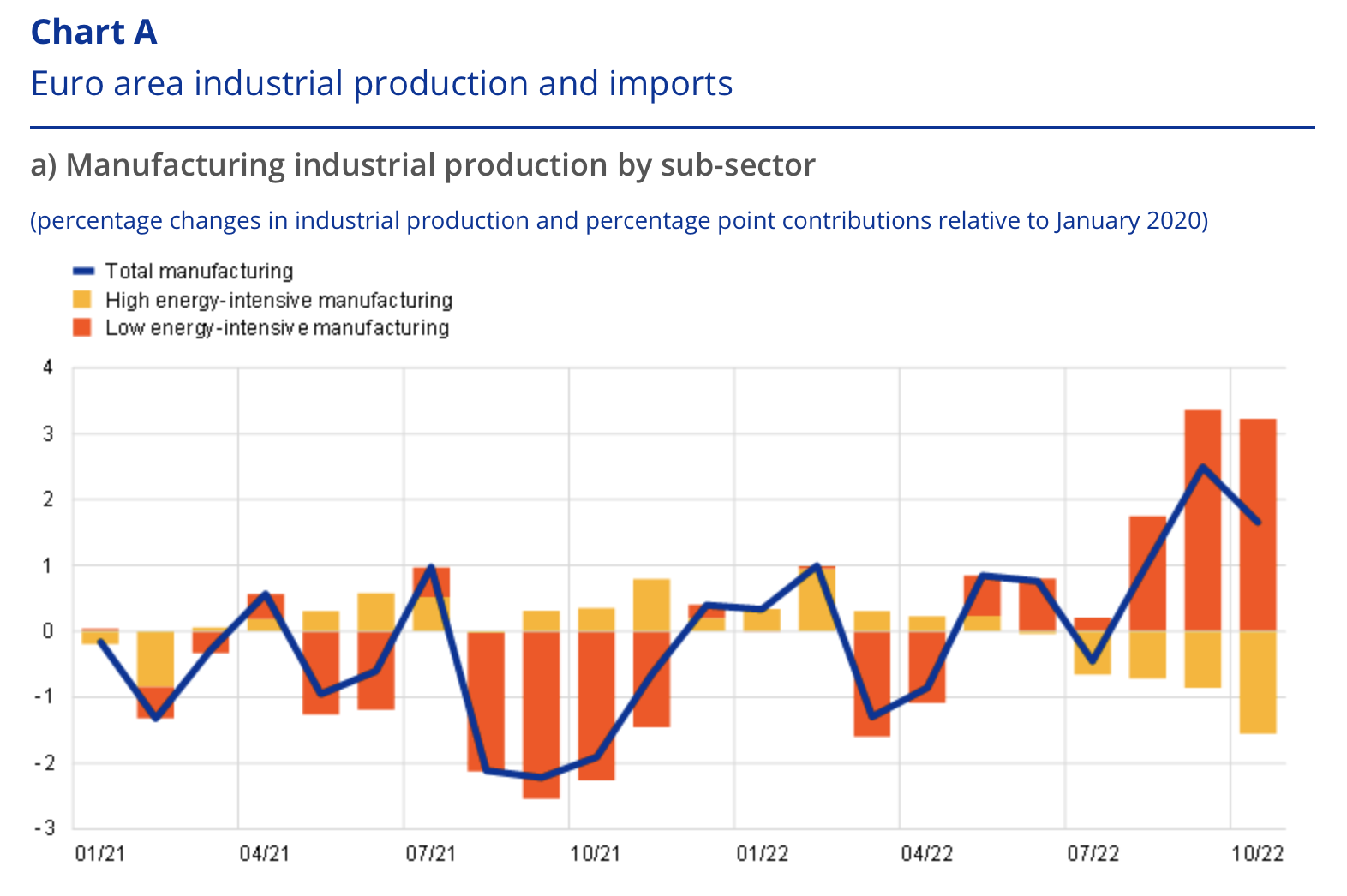

1. Industrial Energy Price Divergence

A growing body of empirical research demonstrates that energy prices are a critical determinant of industrial competitiveness and production location.

Research from several institutions highlights this relationship:

International Energy Agency (IEA)

documents that European industrial electricity prices are frequently two to three times higher than those in the United States.European Central Bank (ECB)

analysis since 2022 shows that energy price shocks significantly reduced European industrial margins and production output.International Monetary Fund (IMF)

research links energy shocks to manufacturing competitiveness losses and trade balance deterioration.

Structural patterns in global industry reflect these price differences.

Industrial electricity prices for manufacturing:

Europe: structurally higher

United States: structurally lower (domestic gas abundance)

China: partially state-managed and subsidised

Observed empirical developments since the 2022 energy shock:

EU industrial production declined

US manufacturing investment surged

energy-intensive sectors began relocating outside Europe

Energy cost divergence

→ industrial margin compression

→ reduced reinvestment

→ industrial relocation

Evidence: Industrial Energy Price Divergence

OECD Electricity Price Comparison

Ref: Comparative Industrial Energy Prices: Europe vs China and the USA (2008–2025) — João Neves Analytics

Bruegel — Decarbonising for Competitiveness

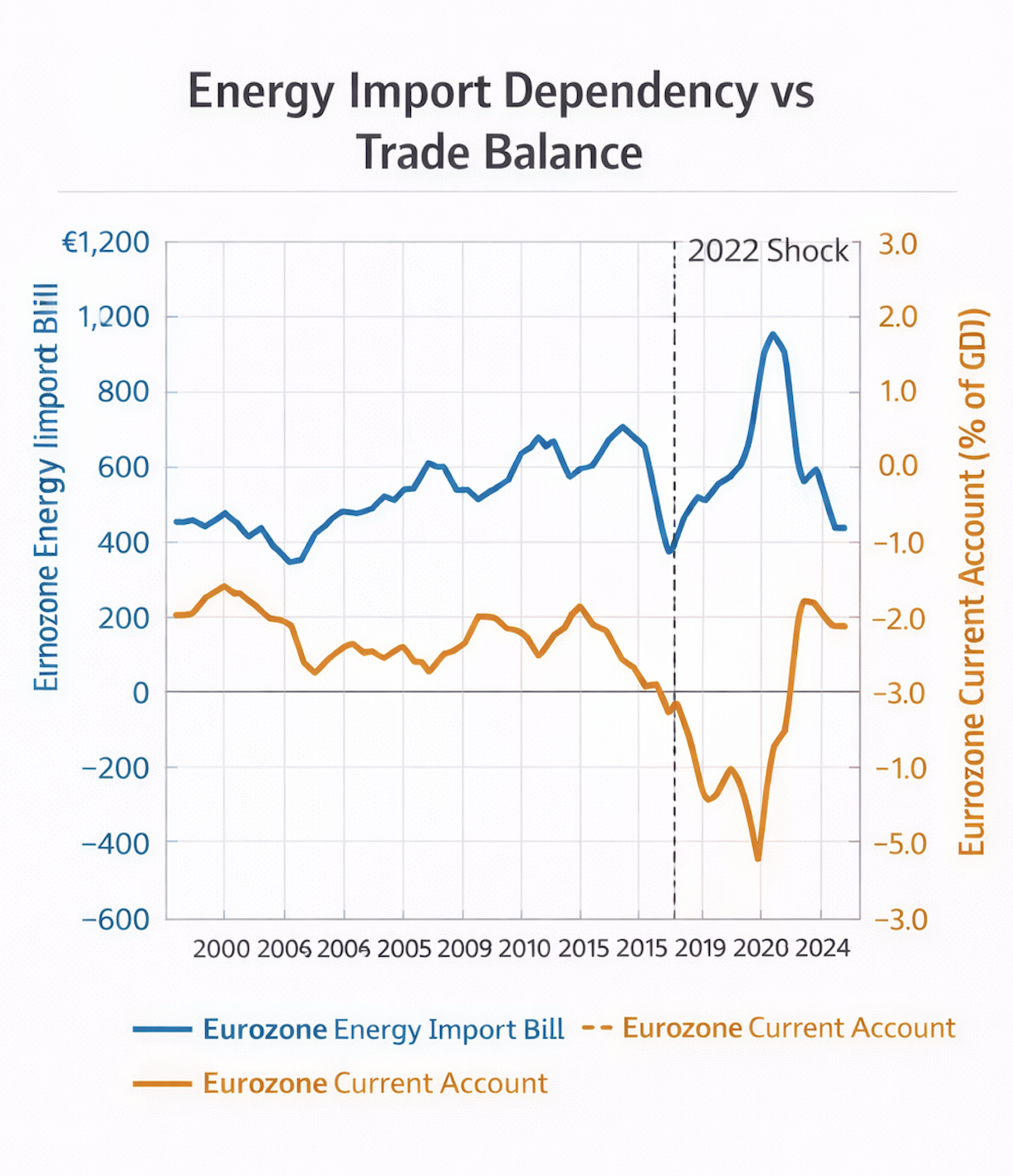

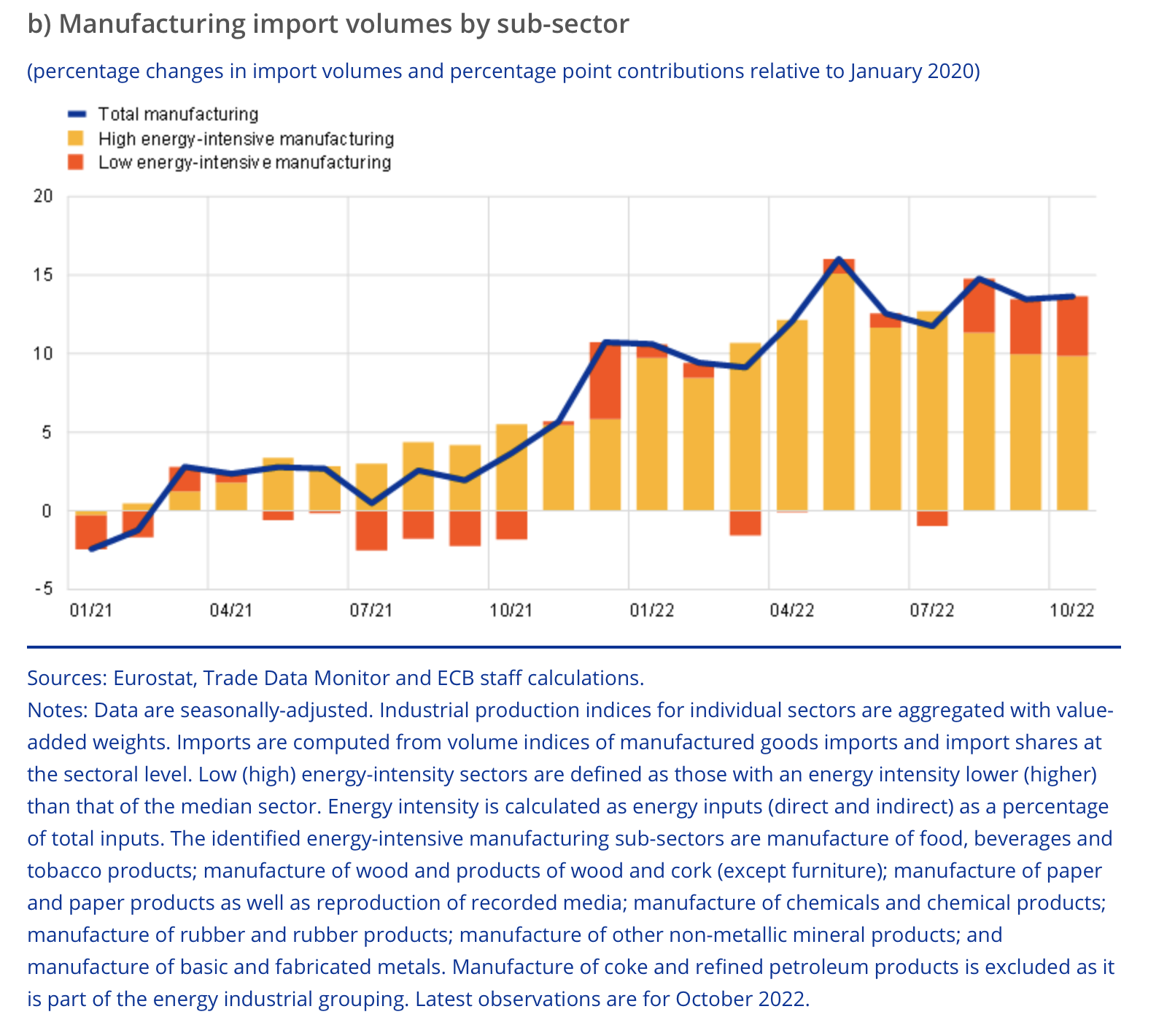

2. Energy Import Dependency and Trade Balance

Energy-importing economies are structurally vulnerable to energy price shocks.

Rising energy prices directly increase the cost of imports, affecting the external balance:

Energy price increase

→ larger energy import bill

→ current account deterioration

Evidence for this mechanism has been widely analysed by:

International Monetary Fund (IMF)

European Central Bank (ECB)

Following the 2022 energy shock:

Europe’s energy import bill increased dramatically

the euro area temporarily moved into trade deficit

This supports the second transmission stage:

Energy constraint

→ external balance deterioration

Evidence: Energy Import Dependency and External Balance

Energy Import Dependency and the Eurozone Current Account

Rising energy import costs directly affect the euro area’s external balance.

The 2022 energy shock sharply increased the energy import bill and coincided with the eurozone’s temporary shift into trade deficit.

Supporting Evidence

Sources:

ECB Economic Bulletin

Eurostat: EU imports of energy products

IMF research on energy shocks and current account balances

Further reading:

ECB Economic Bulletin — Energy Shock Analysis

Eurostat — EU Imports of Energy Products

Energy Price Shocks and Current Account Balances — Science Direct (2024)

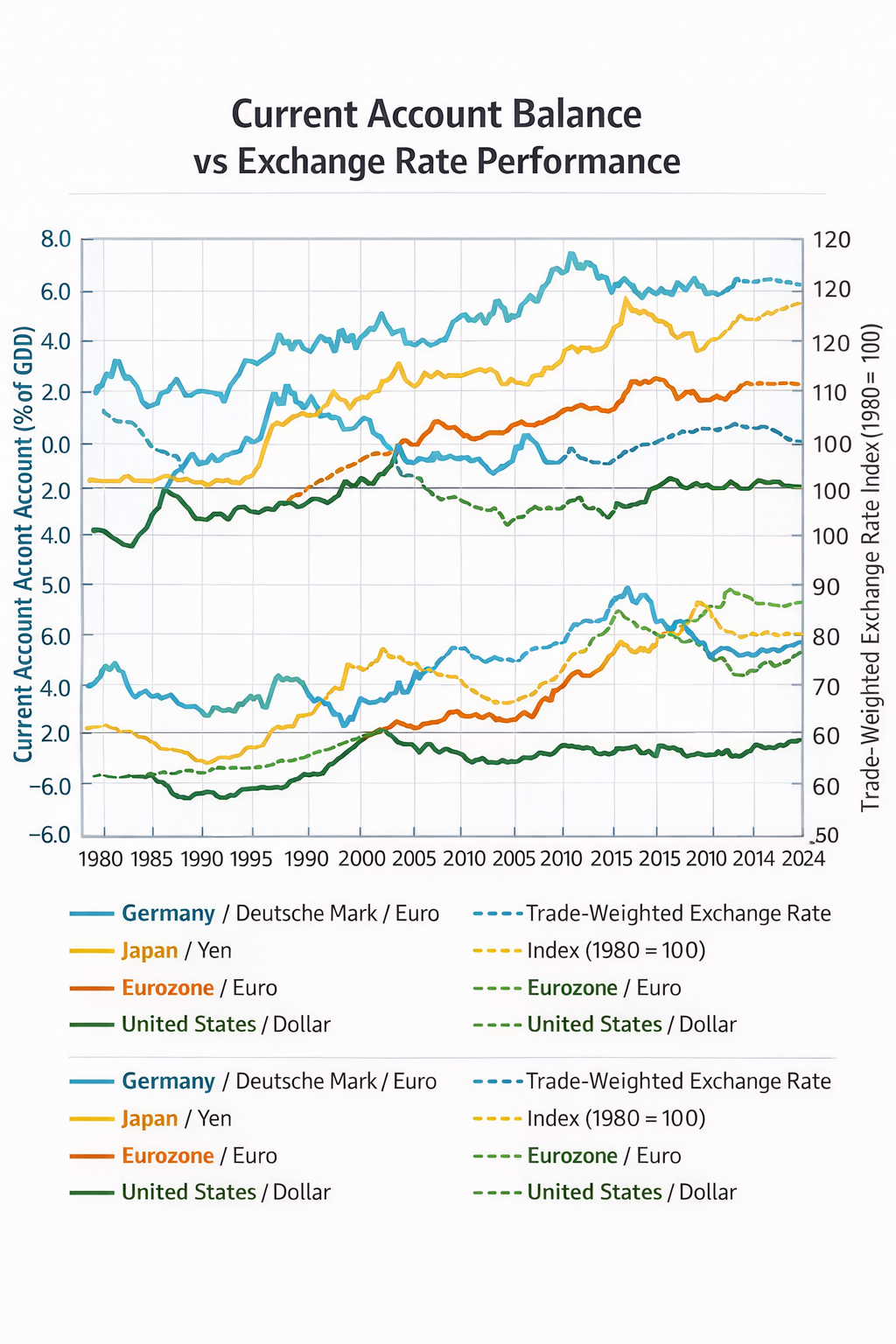

3. Current Account Balance and Currency Strength

External balances are one of the strongest long-run determinants of currency stability.

Persistent patterns observed across global economies include:

Persistent trade surplus

→ currency stability or appreciation

Persistent trade deficit

→ currency vulnerability

This relationship is frequently analysed by:

Bank for International Settlements (BIS)

International Monetary Fund (IMF)

Examples across different economies:

| Country / System | Energy position | Currency pattern |

|---|---|---|

| Norway | energy exporter | strong currency |

| Gulf economies | energy exporters | persistent external surpluses |

| Japan (post-Fukushima) | energy importer | structural yen weakness |

| Eurozone (post-2022 shock) | energy import shock | euro depreciation pressure |

Current Account Balances and Long-Run Currency Performance (1970–2024)

Economies with persistent external surpluses tend to experience stronger or more stable currencies over long horizons. External deficits, by contrast, require sustained capital inflows and often coincide with periods of currency vulnerability.

Structural Implication

Energy systems ultimately shape monetary durability.

When marginal energy costs remain persistently higher than those of competing industrial systems, the effects accumulate across the real economy:

industrial competitiveness weakens

investment relocates

external balances deteriorate

Over time these pressures impose a structural ceiling on currency strength, regardless of monetary policy settings.

In an energy-bound global system, currencies are therefore anchored not only in financial credibility, but in the energy systems that sustain industrial production and capital formation.