EU Asymmetry Under Stress

Inflation, External Cost Transmission, and the Case for System Building

In an energy-bound global order, asymmetry becomes visible under stress — particularly when energy, currency, and financial dynamics interact.

In recent years, Europe has absorbed significant externally generated inflation through energy imports, currency dynamics, and global pricing power. These effects are often misinterpreted as trade imbalances or competitiveness failures. In reality, they reflect cost transmission through energy-dependent systems.

When energy prices rise globally, regions with domestic, capital-intensive energy systems experience inflation differently from regions dependent on imports and price-indexed markets. Inflation is not only a monetary phenomenon; it is a system cost outcome. It reflects the structure of energy dependence embedded in the economy itself.

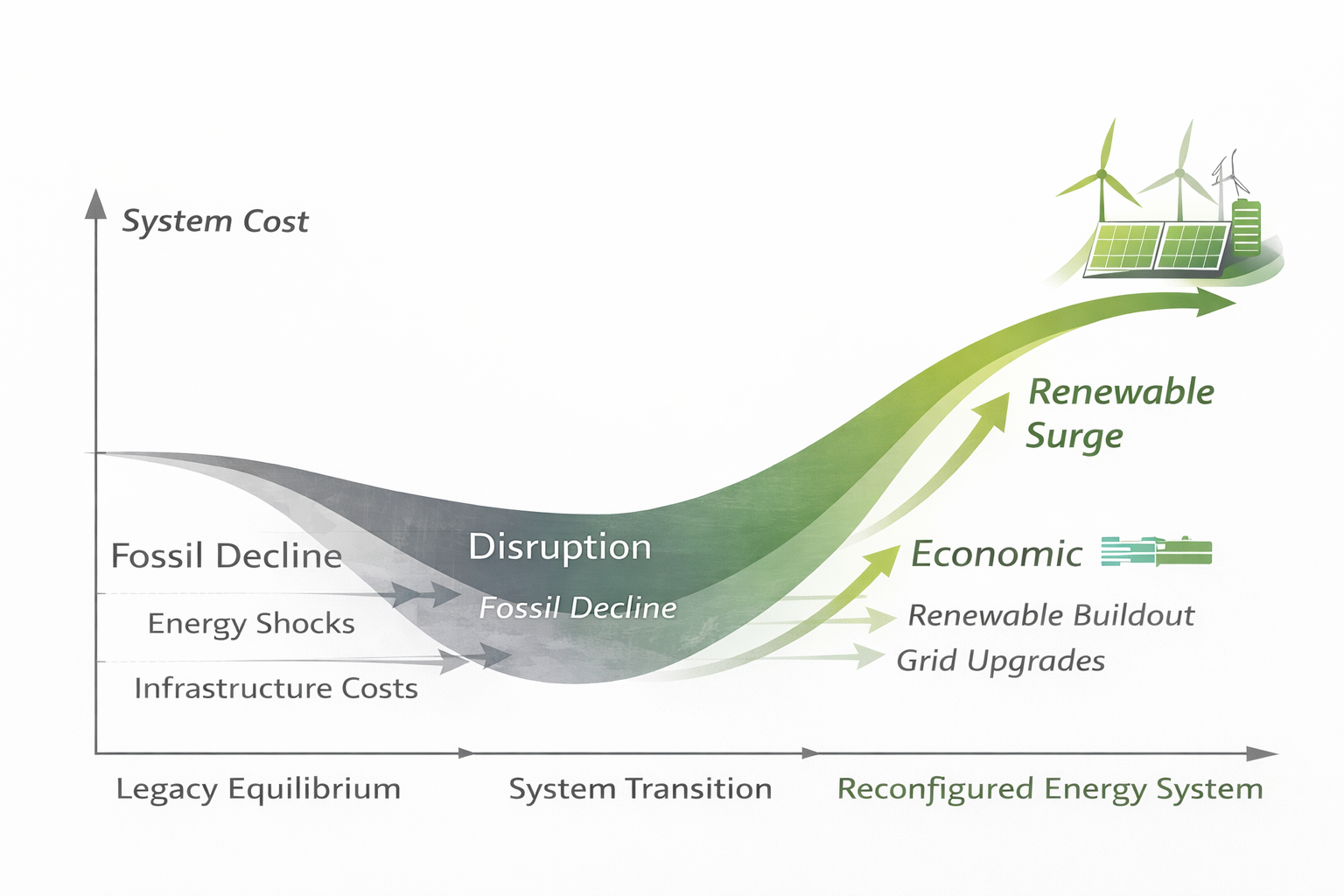

This distinction matters for how Europe interprets external pressure. Claims that trade imbalances result from unfair practices often ignore the structural reality that inflation and cost volatility are exported through energy and system architecture, not tariffs alone. For Europe, the strategic response is therefore not reactive trade measures, but reducing exposure by changing the cost base itself. This dynamic has particular relevance for Southern Europe, where energy import exposure and capital outflows compound adjustment pressures. Under electrification, system building at regional level alters that equation.

Decentralised energy and infrastructure investment do exactly this. By shifting expenditure from ongoing imports and price volatility to domestic, capital-based systems, Europe reduces :

- long-term operating costs

- exposure to external inflation shocks

- currency distortions transmitted through energy pricing

- capital leakage into external systems

(See Energy System Data Companion and Investor Reframing for empirical cost and capital flow analysis.)

This has direct implications for investors.

Europe’s private investors have historically assessed profitability through shorter time horizons and liquid market benchmarks, often favouring external markets with faster returns. In a system transition, this logic becomes self-defeating. What appears more profitable in the short term often compounds long-term cost exposure and structural dependency.

Strategic assets — whether decentralised energy systems, grids, storage, or critical materials such as rare earths — require long-cycle, system-level planning in partnership with the private sector. Their returns are not captured solely through price appreciation, but through cost reduction, system resilience, and internal value creation.

Under stress, asymmetry therefore clarifies Europe’s real

choice:

continue exporting capital and importing volatility — or redirect

private investment toward building the internal systems that stabilise

costs, strengthen SMEs, and deepen the internal market.

This is not primarily a political argument. It is a re-pricing of risk under structural constraint.

Asymmetry under stress does not demand ideology. It demands credible, European-scale system design that allows private capital to profit from building the foundations of competitiveness rather than arbitraging their erosion.