Executive Briefing

Monetary Sovereignty in an Energy-Bound Europe

Structural Implications for the Euro and EU Strategic Autonomy

I. Executive Summary

Europe’s monetary sovereignty is no longer determined primarily by institutional credibility or central bank independence. It is structurally conditioned by energy architecture and industrial depth.

In an Energy-Bound System, energy availability, marginal cost structure, and infrastructure integration act as the binding constraints on economic scale, inflation dynamics, fiscal stability, and currency valuation. Monetary systems transmit these constraints; they do not override them.

Europe faces a structural exposure:

Higher marginal energy costs relative to the United States

External LNG pricing architecture with embedded geopolitical risk premium

Slower industrial scaling and productivity growth

Fragmented capital markets

Relative shrinkage within the G7 hierarchy

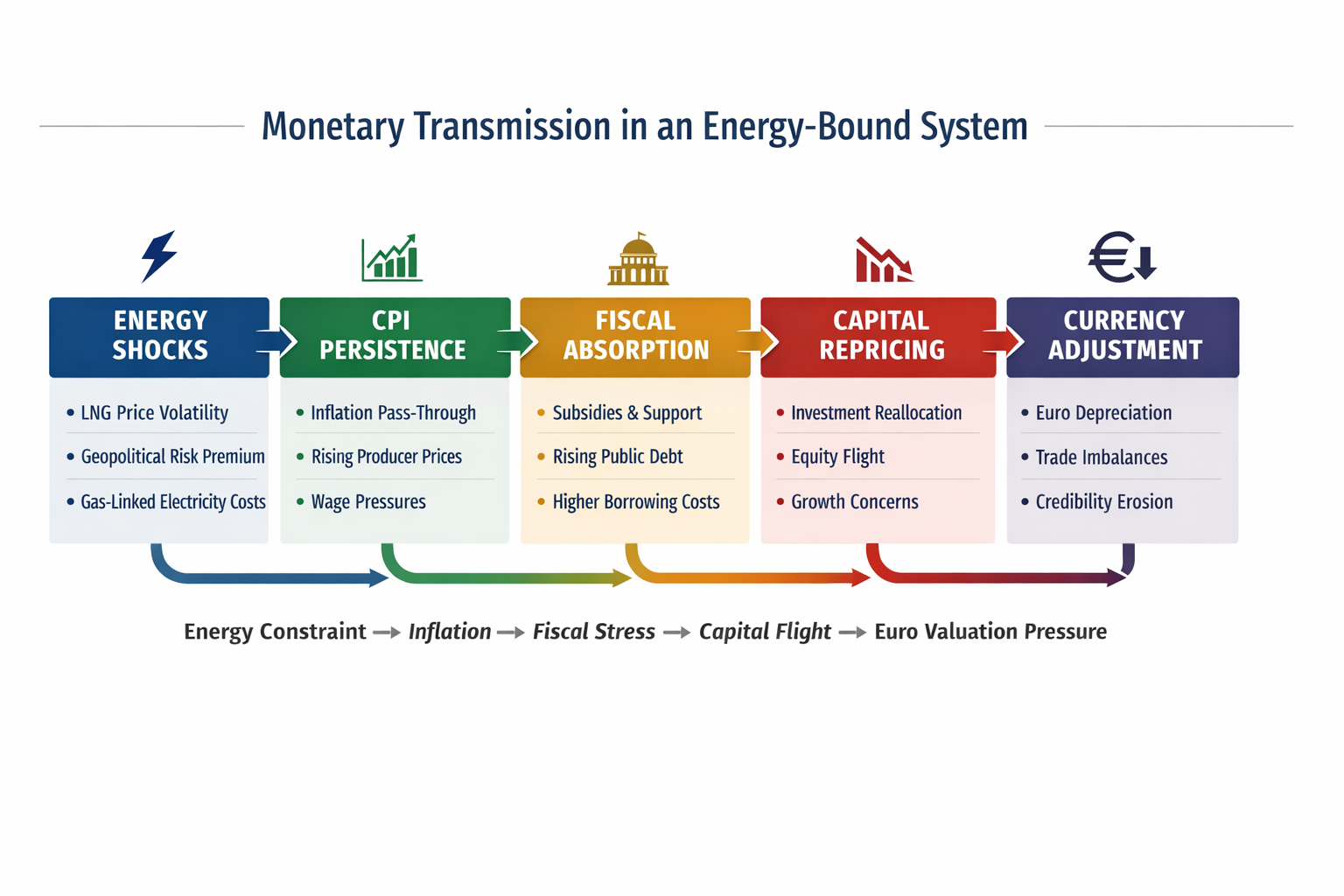

These conditions produce a cumulative transmission chain:

Energy Constraint

→ CPI Persistence

→ Fiscal Absorption

→ Capital Repricing

→ Euro Valuation Compression

This is not a crisis scenario. It is a structural compression dynamic.

Absent accelerated energy and industrial re-anchoring, the euro’s long-term credibility will narrow gradually through differential endurance rather than sudden dislocation.

Energy policy is now monetary policy by other means.

II. Structural Context: From Monetary Primacy to Material Conditioning

For three decades, advanced monetary systems operated under conditions of relative energy abundance. Inflation shocks were treated as cyclical. Monetary tools were assumed to operate with primacy over real-economy inputs.

That environment has ended.

In the current regime:

Energy is no longer elastic.

Marginal cost is geopolitically mediated.

Electricity demand is structurally rising due to digitalisation and AI scaling.

Industrial competitiveness is tightly coupled to energy architecture.

Under these conditions, monetary sovereignty must be redefined.

It is no longer:

Primarily a function of central bank independence;

Nor primarily a function of reserve status;

Nor primarily a function of financial depth.

It is the capacity to absorb energy and industrial shocks without losing macroeconomic control.

Monetary systems now follow material systems.

III. Europe’s Relative Position Within the G7

Europe’s share of relative output within the G7 has compressed over the past decade compared to the United States.

This divergence is structural:

United States:

Domestic energy abundance (gas, oil, electricity scale)

LNG export leverage

Deep, unified capital markets

AI–energy integration capacity

Dollar reserve dominance

European Union:

Structurally higher marginal electricity costs

External energy pricing exposure

Capital market fragmentation

Slower productivity expansion

Higher energy-induced fiscal absorption

Relative economic scale influences monetary hierarchy.

Currencies anchored in:

Energy abundance

Industrial depth

Capital market integration

Technology scale

tend to consolidate monetary authority.

Where these conditions are weaker, monetary leverage narrows.

The euro operates within a hierarchy increasingly shaped by energy advantage.

IV. Energy Geopolitics and the Monetary Transmission Mechanism

Europe’s energy architecture is structurally exposed to external pricing and geopolitical volatility.

Key features:

LNG constitutes a large and growing share of European gas supply.

Global LNG trade is concentrated among a small number of exporters.

Maritime chokepoints embed structural risk premiums.

Electricity markets remain partially gas-indexed.

This creates a direct macroeconomic transmission chain:

External Marginal Pricing

LNG and global gas benchmarks determine domestic electricity cost.CPI Sensitivity

Energy feeds directly into consumer price indices and producer costs.Fiscal Intervention

Governments deploy subsidies and industrial support to mitigate shock.Debt Exposure

Fiscal expansion interacts with tightening cycles and higher rates.Capital Repricing

Investors reassess long-term growth and duration.Currency Compression

External valuation adjusts gradually to structural differential.

Energy risk premium becomes monetary risk premium.

Monetary tightening cannot neutralise externally determined marginal cost structures.

V. Capital Allocation Dynamics: Structural Preference for US Markets

European capital outflows toward US equity markets reflect structural incentives rather than speculative sentiment.

Investors evaluate:

Energy cost stability

Electricity availability for AI scaling

Industrial expansion potential

Capital market liquidity

Policy coherence

The United States currently offers:

Lower structural electricity cost

Integrated energy–technology scaling

Concentrated high-growth sectors

Reserve currency liquidity

Europe presents:

Higher energy volatility

Fragmented equity markets

Lower expected growth trajectory

Higher fiscal exposure

Consequences:

Persistent portfolio preference for US stocks

Compression of European equity valuations

Lower domestic capital formation

Reduced industrial reinvestment

Capital allocates toward duration and resilience.

Where energy architecture supports long-term growth, capital concentrates.

VI. Euro Valuation and Credibility

Currency credibility erodes gradually through relative divergence.

Persistent energy disadvantage produces:

Lower expected productivity growth

Reduced industrial return on investment

Narrower export competitiveness

Higher structural fiscal burden

Over time, this affects:

Current account balance

Bond market duration confidence

Long-term exchange rate equilibrium

Euro depreciation, when observed, reflects structural repricing rather than sudden institutional loss of credibility.

Institutional strength cannot permanently offset material asymmetry.

The euro’s long-term valuation increasingly mirrors Europe’s energy architecture.

VII. Macroeconomic Consequences

Structural energy exposure produces five macroeconomic pressures:

Investment Drag

Higher energy cost reduces expected return on European industrial projects.Productivity Slowdown

Industrial underinvestment weakens long-term output growth.Fiscal Socialisation of Energy Risk

Subsidies and industrial compensation increase public debt.Interest Rate Sensitivity

Energy-driven inflation forces tighter policy, raising debt servicing burden.Political Strain

Energy-induced real income compression intensifies redistribution pressure.

Monetary authorities are required to manage inflation rooted in energy cost while preserving growth in a structurally exposed system.

Trade-offs intensify because the constraint is structural, not cyclical.

VIII. Regulatory Architecture and Industrial Capacity

Europe’s prior deregulation model — emphasising exposure, efficiency, and lean-state doctrine — was developed under conditions of energy abundance.

In an Energy-Bound System, this architecture presents new risks.

Deregulation today:

Fragments capital allocation

Weakens SME shock absorption

Accelerates industrial relocation

Reduces coordinated scaling capacity

SMEs compete globally while facing structurally higher energy costs.

At the moment Europe must rebuild industrial depth and technological capacity, regulatory exposure can amplify vulnerability rather than resilience.

Industrial regeneration is now a monetary stabilisation strategy.

IX. Policy Implications

Monetary sovereignty in Europe now depends on coordinated action across four domains:

1. Energy Architecture

Accelerated renewable scaling

Grid integration and storage deployment

Reduced gas indexation

Corridor diversification

2. Industrial Regeneration

Strategic sector coordination

AI–energy alignment (compute locality)

SME resilience reinforcement

3. Capital Market Integration

Deeper equity market integration

Reduced fragmentation

Longer duration financing instruments

4. Fiscal–Monetary Alignment

Infrastructure investment framed as balance-sheet defence

Reduced reliance on short-term subsidy cycles

Energy policy is macroeconomic policy.

Industrial policy is monetary stabilisation.

Infrastructure investment is currency defence.

X. Strategic Conclusion

The euro’s durability will not be determined by central bank signalling alone.

It will be determined by:

Relative energy architecture resilience

Industrial regeneration capacity

Capital duration confidence

Cohesive policy coordination

Europe has already experienced relative shrinkage within the G7.

Absent structural re-anchoring in energy sovereignty, that divergence may deepen gradually.

The euro will not fail abruptly.

It will compress through differential endurance.

In an Energy-Bound System,

currency authority follows material capacity.

The future of European monetary sovereignty begins in its energy system.

Suggested Strategic Reading

The following materials provide additional context for the structural dynamics examined across this project, particularly the interaction between energy systems, industrial capacity, capital allocation, and technological infrastructure.

Core Essays on this Site

EU Energy Paradigm Shift Explains how Europe’s industrial competitiveness and monetary space are increasingly shaped by energy cost structure.

AI Sovereignty Stress Test Examines how energy volatility and compute localisation shape technological sovereignty and digital infrastructure risk.

Energy Constraint and the Monetary Ceiling Traces the transmission from energy systems to industrial margins, capital flows, and monetary policy space.

Strategic Context

These external works provide broader analytical perspectives on energy systems, industrial transformation, and technological competition.

Vaclav Smil — Energy and Civilization

A foundational history of how energy systems shape economic structures.Daniel Yergin — The New Map

Explores the geopolitical implications of the evolving global energy landscape.International Energy Agency (IEA)

Global energy investment and transition analysis.International Monetary Fund — Energy Price Pass-Through Studies

Research on how energy shocks transmit into inflation and industrial margins.