2. Energy Leverage: U.S. Energy Autonomy and the Global Order

Energy, power, and strategic autonomy — a paired analysis.

This article is part of the “New G2 Global Order” series, which examines how energy, finance, technology, and governance are restructuring global power.

Key Thesis

The United States’ transition from energy dependence to energy abundance has reshaped global power, but abundance alone does not guarantee strategic insulation. Energy leverage now interacts with financial dominance, industrial capacity, and electricity infrastructure, creating new vulnerabilities alongside new strengths. Without sustained investment in grids, manufacturing, and supply chains, energy autonomy risks producing leverage without resilience — power that appears decisive but decays over time.

Preface

The United States has undergone a profound structural shift, moving from the world’s largest oil importer to one of its leading exporters. Enabled by the shale revolution and sustained bipartisan support for energy security, the U.S. now commands significant oil, gas, and nuclear capacity. This transformation has reshaped not only its domestic economy but also its strategic posture abroad. Energy abundance has become a pillar of national power — influencing trade balances, alliance structures, and geopolitical leverage — while subtly aligning aspects of U.S. statecraft with the characteristics of a modern petrostate. Unlike earlier financial-hegemonic phases, the United States now combines reserve-currency dominance with energy abundance. As a major oil and gas producer, it links monetary power to energy leverage—especially through stablecoin-based channels—deepening its resemblance to a petro-financial state and extending its geopolitical reach.

Although the energy sector represents a modest share of U.S. GDP, its systemic impact is disproportionate. Expanding exports, a persistently strong dollar, and capital inflows linked to energy and technology risk familiar structural distortions, including pressures on manufacturing competitiveness and regional imbalances reminiscent of “Dutch disease” dynamics. At the same time, the rapid expansion of energy-intensive sectors — artificial intelligence, hyperscale data centers, electrification, and advanced manufacturing — has tightened the link between energy abundance and industrial power. Yet this advantage rests on fragile foundations: the U.S. electricity grid remains outdated, with critical components of transmission, transformers, and power electronics still dependent on foreign supply chains. Energy autonomy at the resource level thus coexists with vulnerabilities at the industrial and infrastructural level.

As Europe’s confrontation with Russia has revealed the strategic costs of dependence without energy sovereignty, the American case illustrates a different but related constraint: abundance without fully aligned industrial and infrastructural depth. In both cases, power exists, but its durability is shaped — and limited — by material foundations rather than political intent alone.

Globally, America’s new energy position has altered its strategic geography. Reduced dependence on Middle Eastern oil has shifted attention toward the Western Hemisphere, the Arctic, and the Indo-Pacific. This reorientation coincides with efforts to counter China’s Belt and Road Initiative and to secure access to critical minerals essential for energy systems, batteries, and digital infrastructure. A renewed, quasi–Monroe-Doctrine posture in the Americas risks friction with Latin American states increasingly integrated into Chinese-led investment networks and the broader BRICS framework. Energy and mineral security, once peripheral, now sit at the center of hemispheric politics.

At the monetary level, U.S. energy and financial power increasingly intersect. The expansion of dollar-denominated stablecoins offers Washington a new channel to project currency influence, particularly in emerging economies. While this may reinforce dollar primacy in the short term, it also risks deepening structural dependency in weaker monetary systems, eroding fiscal autonomy, and amplifying balance-of-payments fragility. In regions already constrained by dollar-denominated trade and debt — notably Latin America — digital dollarization may intensify political and economic backlash. Even advanced economies such as the European Union face long-term challenges to financial sovereignty, albeit mitigated by stronger institutions.

Paradoxically, the more aggressively the dollar’s digital extensions are weaponized, the more fragile their legitimacy may become. Financial leverage unsupported by durable industrial and productive capacity risks accelerating efforts by rival blocs to construct alternative settlement systems, commodity-linked trade mechanisms, and non-dollar financial infrastructures.

Finally, the U.S. model of fossil-fuel-backed digital and industrial expansion is creating a widening energy asymmetry with Europe. Energy abundance allows the United States to scale AI, defense production, and advanced manufacturing rapidly. By contrast, Europe’s higher energy costs and uneven decarbonization trajectory threaten industrial competitiveness unless matched by accelerated clean-energy deployment, secured supply chains, and genuine technological autonomy. Energy is no longer a background variable of geopolitics; it is the core constraint shaping industrial strategy, monetary power, and digital leadership. In this emerging order, energy autonomy does not guarantee strategic dominance — but without it, strategic ambition quickly collapses into dependence.

I. The Structural Shift: From Import Dependence to Export Capacity

For much of the post-war period, the United States was both a major energy producer and the world’s largest oil importer. Domestic output was substantial, but consumption consistently exceeded supply, embedding U.S. prosperity in the stability of global energy markets, maritime trade routes, and foreign production zones. Energy security was therefore inseparable from international cooperation, naval power, and sustained geopolitical engagement in key producing regions.

This structure changed decisively over the past fifteen years. Advances in hydraulic fracturing and horizontal drilling unlocked large volumes of previously uneconomic oil and gas reserves, reversing long-standing import dependence. By the late 2010s, the United States had become a net exporter of energy for the first time in more than six decades, with natural gas exports expanding rapidly and crude oil production reaching historic highs.

Energy policy subsequently evolved into a national security priority with broad bipartisan backing. Support for domestic production, reshoring of critical supply chains, and investment in strategic energy technologies came to be framed not only as an economic imperative but as a foundation of geopolitical autonomy. Energy independence became a symbol of restored national leverage.

Yet independence marked only the first stage. As exports expanded, energy shifted from a vulnerability into an instrument of power. This transition mirrors a broader structural pattern visible elsewhere: just as Europe’s confrontation with Russia exposed the costs of dependence, the American case reveals the limits of abundance once energy becomes embedded in global systems of finance, industry, and technology.

Energy leverage, however, is exercised less through ownership of resources than through control and exposure within global transit systems.

Global Maritime Oil Chokepoints and Shipping

Routes

Yellow circles indicate major maritime chokepoints through

which millions of barrels of oil and petroleum products transit daily by

sea. Red lines represent primary tanker shipping routes. These

chokepoints function as systemic points of energy leverage, where

disruption can rapidly transmit price and supply shocks across global

markets.

Source: U.S. Energy Information Administration (EIA).

II. Energy Power and Petrostate Dynamics

Energy power differs fundamentally from energy independence. Independence reduces exposure; power reshapes incentives, markets, and geopolitical behaviour. As U.S. energy exports grew, so too did their macroeconomic and strategic consequences.

Although the energy sector accounts for roughly 7 percent of U.S. GDP, its global footprint is far larger. Energy exports influence trade balances, capital flows, and currency valuation. Rising export revenues and associated financial inflows place upward pressure on the dollar, reinforcing financial dominance but also raising the risk of Dutch disease dynamics, in which currency appreciation undermines the competitiveness of manufacturing and other tradable sectors.

Historically, commodity-exporting states have faced this trade-off: resource wealth generates fiscal and geopolitical leverage but crowds out industrial diversification over time. The United States is not a traditional petrostate — it retains a diversified economy and deep capital markets — but it is not immune to these structural pressures. A persistently strong dollar supports financial power while weakening export competitiveness and exacerbating trade imbalances.

Here the American experience converges analytically with Europe and Russia, albeit from opposite directions. Europe’s vulnerability lies in dependence without leverage; Russia’s in leverage constrained by limited industrial and technological depth. The United States occupies a third position: leverage grounded in abundance, but increasingly mediated by financial channels rather than production.

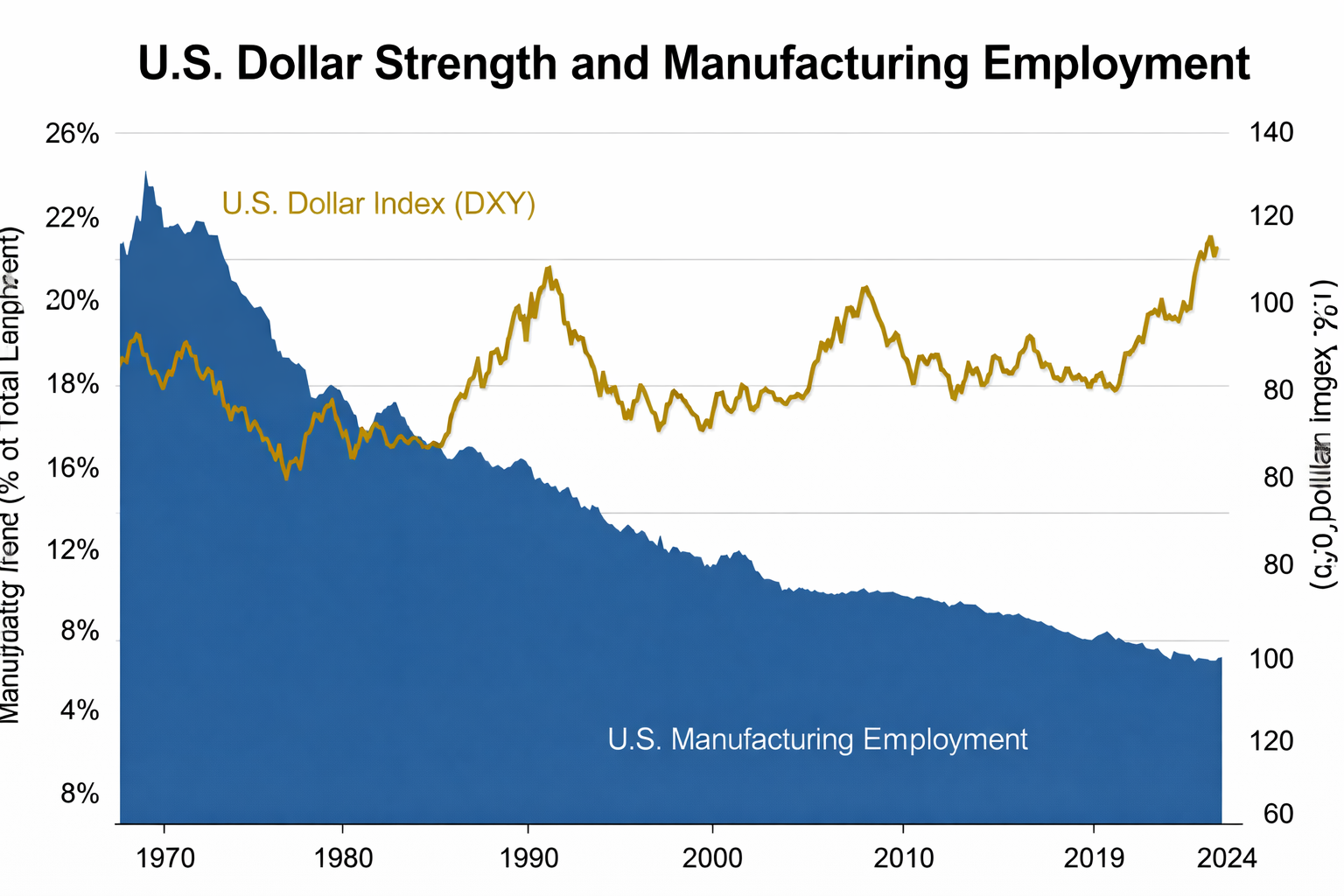

Long periods of dollar appreciation have coincided with structural decline in U.S. manufacturing employment, a pattern consistent with commodity-linked currency pressures observed in export-dependent economies.

Energy power thus strengthens U.S. leverage in the short term while introducing longer-term risks to industrial renewal and economic balance.

U.S. Dollar Strength and Manufacturing

Employment

Long-term periods of sustained dollar appreciation have coincided

with a structural decline in U.S. manufacturing employment. While

multiple factors shape industrial employment, this pattern is consistent

with Dutch disease dynamics observed in commodity-exporting economies,

where currency strength and capital inflows crowd out tradable

sectors.

III. The Energy–Electricity Nexus and the AI Economy

The strategic importance of energy now extends well beyond exports. The internal structure of the U.S. economy itself is becoming more energy-intensive, particularly with respect to electricity.

Electricity demand from data centres is projected to more than double by 2030, outpacing transport electrification and becoming a primary driver of U.S. power demand growth.

Artificial intelligence, cloud computing, data centres, and digital infrastructure are driving a surge in electricity demand. Electrification of heavy industry, transport, and heating further accelerates this trend. Electricity is no longer merely an input; it is a binding constraint on technological leadership, industrial competitiveness, and military capacity.

This shift introduces a paradox. The United States enjoys abundant primary energy resources, yet its ability to convert energy into reliable, affordable electricity is increasingly constrained. Electricity availability, grid capacity, and transmission speed — rather than energy reserves — now determine the ceiling of economic and technological expansion.

AI exposes this constraint more clearly than any other sector. It is not a virtual industry, but a material system whose growth depends on power generation, transmission infrastructure, cooling systems, semiconductors, and critical minerals. Energy abundance without electrical capacity is not power; it is latent potential constrained by infrastructure.

IV. Grid Fragility and Industrial Vulnerability

The condition of the U.S. electricity grid reveals a critical vulnerability at the heart of energy power. Large portions of transmission lines, substations, and transformers are well beyond their original design life. Grid expansion has lagged demand growth due to regulatory fragmentation, permitting delays, and decades of underinvestment.

Compounding this challenge is dependence on foreign suppliers for critical grid components, particularly large transformers and power electronics. Many are manufactured abroad with long lead times and limited redundancy. Disruptions — geopolitical, economic, or accidental — could leave entire regions, industrial facilities, or digital infrastructure without power for extended periods.

This vulnerability echoes Europe’s predicament in reverse. Where Europe’s energy dependence constrains strategic autonomy, the United States’ infrastructural dependence threatens to hollow out the advantages of energy abundance. Tariff-based reshoring alone cannot resolve this mismatch; without scale, coordination, and technological upgrading, it risks raising costs without restoring resilience.

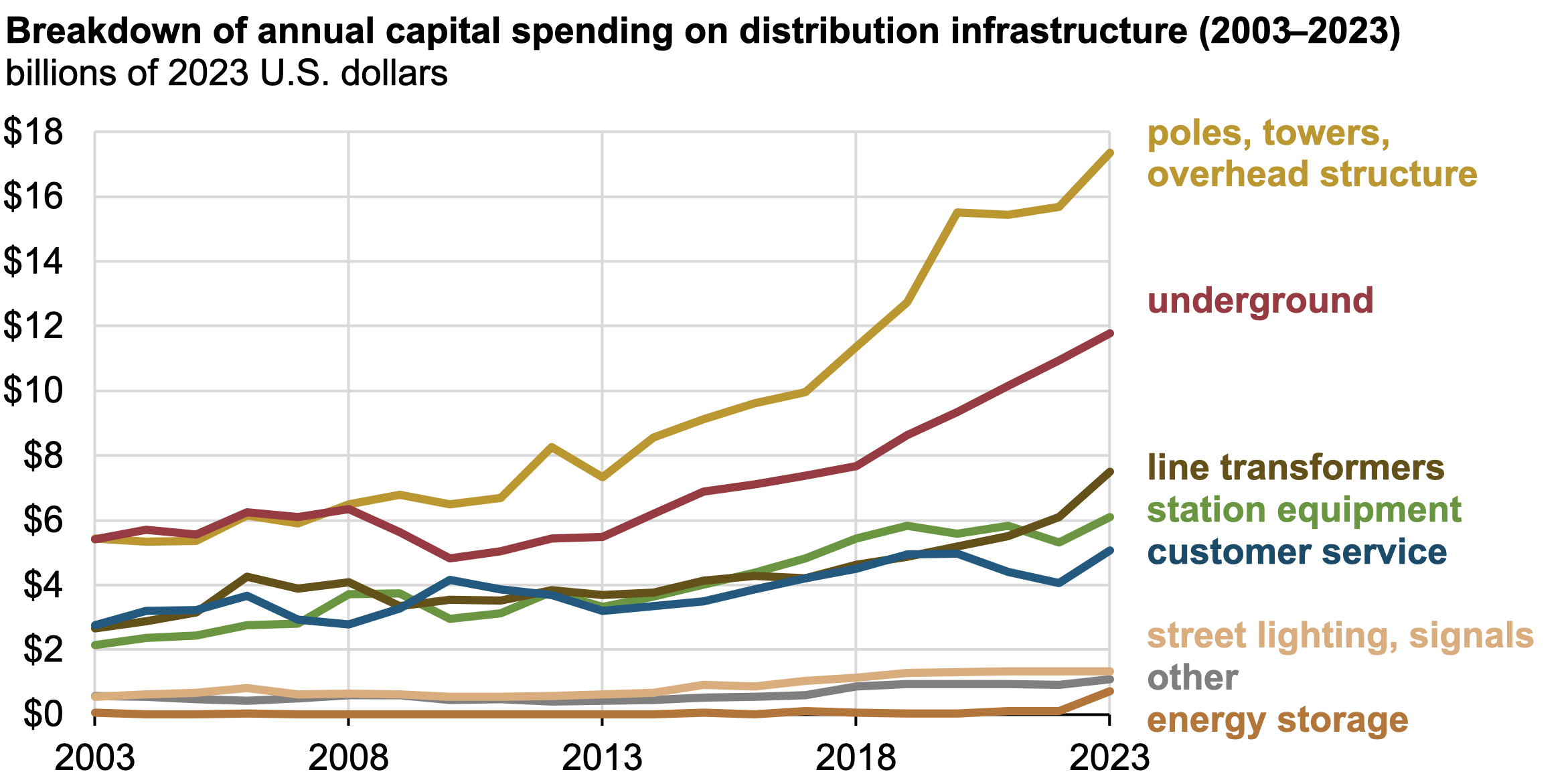

Investment patterns reinforce the problem.

Capital spending has risen unevenly, with underinvestment in precisely the grid components most critical for managing concentrated, high-load electricity demand.

Higher spending has not translated into proportional increases in flexibility, resilience, or capacity where they are now most needed. Electricity, not fuel supply, has become the binding constraint on U.S. industrial and digital expansion.

U.S. Electricity Distribution Infrastructure Capital Spending

(2003–2023)

Capital spending on U.S. electricity distribution

infrastructure has increased unevenly over the past two decades. The

largest gains have been concentrated in poles, towers, and overhead

structures, while investment in critical components such as

transformers, station equipment, and underground infrastructure has

grown more slowly. This imbalance helps explain why rising electricity

demand — particularly from data centres and electrification —

increasingly collides with structural grid constraints despite higher

overall investment.

Source: U.S. utility distribution capital expenditure data

(inflation-adjusted to 2023 USD).

V. Energy Autonomy Does Not Mean Insulation

A persistent misconception of energy independence is the belief that domestic production insulates the economy from global shocks. In reality, oil and gas prices are set in global markets. Supply disruptions, geopolitical conflict, or demand surges abroad transmit directly into domestic prices, inflation, and political stability.

As a major exporter, the United States is now more exposed — not less — to global price volatility. High prices benefit producers and exporters but impose costs on consumers and energy-intensive industries. Low prices reverse the equation. Energy power thus introduces cyclical vulnerability rather than eliminating risk.

This mirrors Europe’s experience from the opposite direction: autonomy changes the form of exposure, not its existence. Interdependence remains structural.

VI. Strategic Reorientation and Comparative Constraints

Reduced dependence on Middle Eastern energy has reshaped U.S. geopolitical priorities toward the Western Hemisphere, the Arctic, and the Indo-Pacific — regions central to future energy flows, mineral supply chains, and technological competition.

In this system, Russia occupies an increasingly constrained position. It remains a major energy producer, but sanctions, demographic pressure, and limited access to advanced manufacturing restrict its ability to convert resource wealth into sustained industrial and technological power. This has deepened asymmetry in its relationship with China, which has pursued a more integrated model linking energy planning, industrial policy, and technological sovereignty.

Europe faces a different constraint. The European Union combines institutional coherence with persistent energy and industrial fragmentation, risking long-term dependency in both digital and strategic domains.

The United States, by contrast, holds advantages across energy, finance, and AI — but, as Europe’s dependence and Russia’s constraint both demonstrate, advantage without structural alignment produces the illusion of choice rather than durable autonomy.

Conclusion: Energy Power with Structural Limits

The United States has successfully transformed energy dependence into energy power. This transition has reshaped global positioning and underpinned industrial and technological ambition. Yet energy power is not self-sustaining.

Currency pressures, industrial imbalances, infrastructural fragility, and continued exposure to global volatility constrain its durability. Energy abundance without resilient grids, industrial depth, and supply-chain control risks becoming a source of instability rather than enduring strength.

Taken together with Europe’s exposure through dependence and Russia’s exposure through constraint, the American case illustrates a third condition of the emerging global order: power that exists, but can decay if its material foundations are assumed rather than built.

In the end, autonomy cannot be declared through markets, platforms, or finance alone. Like sovereignty itself, it must be constructed — in grids, factories, supply chains, and energy systems capable of sustaining the age of AI.

Energy abundance underpins digital expansion, but monetary channels ultimately determine how power is distributed and enforced globally—a dynamic examined in Monetary Power.

References

https://www.climateandcapitalmedia.com/petrostate-versus-electrostate

US’s Petrostate versus China’s Electrostate

The Future of the Northern Sea Route - A “Golden Waterway” or a Niche Trade route

The Economic Benefits of Unleashing American Energy

Why US Energy Independence Won’t Mean Greater US Energy Autonomy

#PETROSTATES #ELECTROSTATES #US_HEGEMONY #US_DOLLAR #RESERVE_CURRENCY #US_INFLUENCE_GLOBAL_SOUTH #US_ENERGY #GLOBAL_ORDER #ENERGY_AUTONOMY