External Limits of European Sovereignty

Energy Leverage and the Gulf System

This article applies the structural energy and system-constraint framework developed in the GLOBAL panel to Europe’s external exposure through the Gulf energy corridor.

Recent escalation in the Gulf should not be read as a distant regional crisis. It is a reminder of the external constraints on European sovereignty in a global system where energy, finance, and security have become tightly coupled instruments of power.

What matters is not escalation itself, but what it reveals about how power now operates — increasingly through control of systems rather than through multilateral rules or formal alliances.

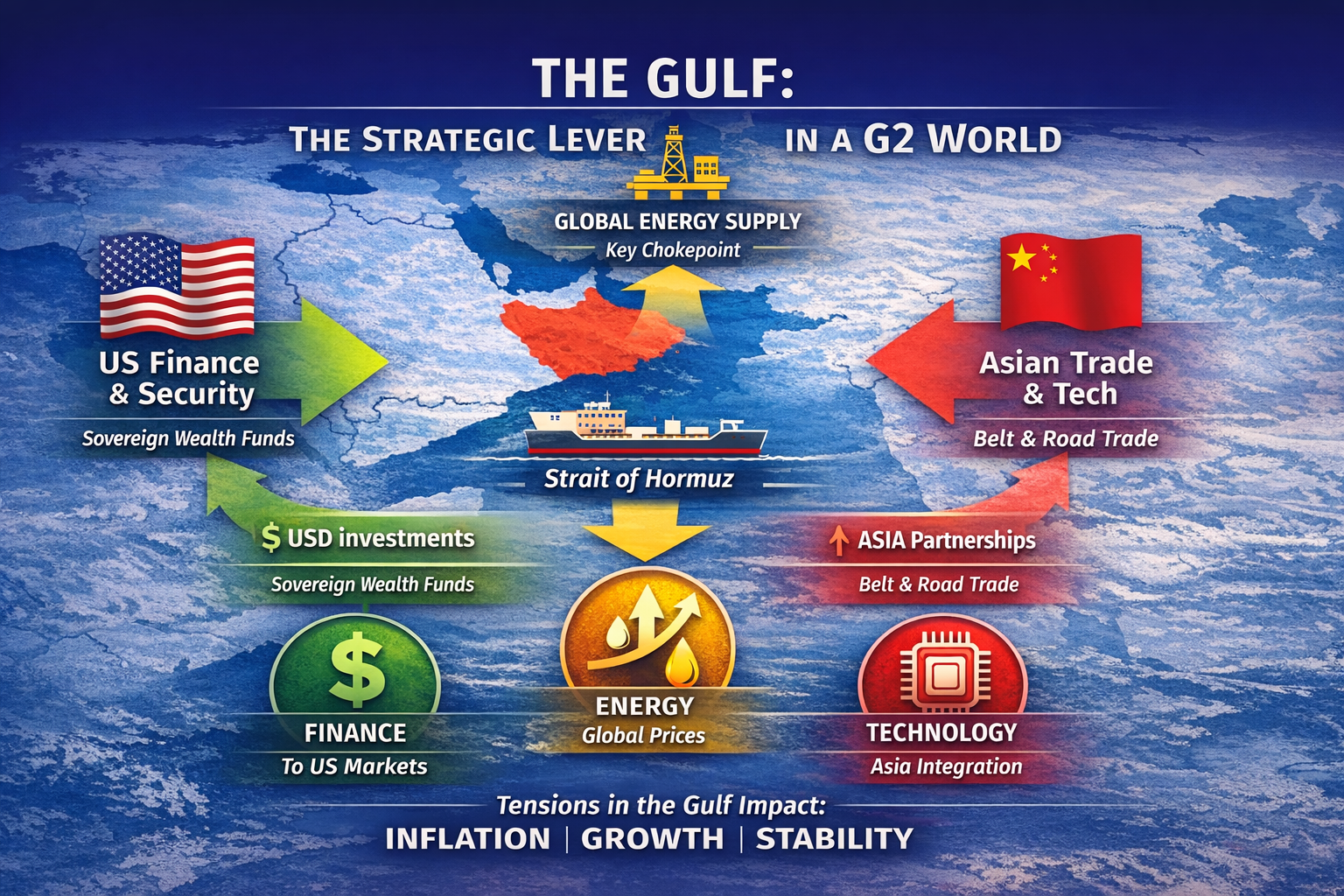

Three systems converge in the Gulf

The strategic importance of the Gulf lies in the convergence of three systems that increasingly define geopolitical leverage.

Energy. Instability involving Iran and the vulnerability of critical chokepoints such as the Strait of Hormuz inject risk premiums into global energy markets even without physical disruption. These premiums transmit rapidly into inflation expectations worldwide.

Finance and security. Gulf balance sheets remain deeply embedded in US-centred financial markets, from Treasuries to dollar-denominated assets, while regional security architectures remain closely tied to US defence systems and guarantees. This anchoring provides stability, but also creates structural exposure to external decisions.

Trade and future growth. At the same time, Gulf trade and long-term economic strategy increasingly point east. China is now the largest trading partner for most Gulf economies and the dominant destination for energy exports. Gulf capital is flowing into Asian manufacturing, logistics, AI, and infrastructure linked to long-term Eurasian growth.

The Gulf dependency trap

This convergence creates a dependency trap.

The Gulf is not choosing between the United States and China. It is managing asymmetric dependence: financial stability and security anchored in the US system, while trade revenues and future growth increasingly depend on Asia.

Escalation tightens this trap by raising the cost of hedging between systems that are becoming less compatible. Energy risk premiums rise, financial exposure becomes more salient, and political room for manoeuvre narrows — both for the region and for those downstream.

Europe and the inflation constraint

Europe is one of those downstream actors.

Despite sustained efforts at diversification, Europe remains structurally dependent on imported energy. In this context, Gulf instability translates directly into higher prices, industrial costs, and inflationary pressure.

Inflation is the political choke point. Energy-driven price volatility erodes household purchasing power and destabilises governing coalitions. This matters precisely as Europe debates retaliatory tariffs, industrial subsidies, and regulatory measures aimed at asserting greater economic autonomy. Industrial policy, rearmament, electrification, and digital infrastructure are all energy-intensive. When energy prices rise, the cost of confrontation rises with them.

From inflation to deindustrialisation

The strategic consequence is not only inflation, but accelerating deindustrialisation risk.

Energy-intensive sectors — chemicals, steel, aluminium, fertilisers, cement, glass — are already under strain. Increasingly, so are industries framed as “strategic”: batteries, EV supply chains, semiconductors, data centres, and defence manufacturing. These sectors cannot scale or remain competitive under sustained energy volatility without relocating capital or cutting capacity.

This exposes a deeper paradox in Europe’s current trajectory.

Rearmament without autonomy

Rearmament is accelerating, yet much of it relies on external energy inputs and US-origin defence platforms, software, and sustainment systems. Capability may increase, but autonomy does not.

Without a resilient energy and industrial base, rearmament risks becoming an expensive exercise in dependence rather than a foundation for sovereignty.

Multilateralism under strain

The Gulf reveals how far multilateral governance has given way to leverage over systems — energy flows, financial liquidity, and security guarantees. As this logic hardens, the space for rules-based solutions narrows, and strategic autonomy becomes harder to sustain for energy-import-dependent economies.

European sovereignty today is not constrained by ambition or regulation alone. It is constrained by energy exposure and industrial fragility.

Understanding how instability in the Gulf shapes these constraints is not optional. It is central to any serious European strategy in a G2 world.

Further Reading

Corridors, Chokepoints, and the Geography of Leverage (GLOBAL)

EU Asymmetry Under Stress (EU Sovereignty)

Defense Addendum — Energy, Rearmament, and Strategic Autonomy** (EU Challenge)