Europe’s Decisive Decade

Energy Sovereignty, Industrial Renewal, and Strategic Autonomy in a G2 World

Europe’s decisive decade: energy sovereignty as the foundation of strategic autonomy and security, industrial renewal, and geopolitical relevance

A historic global realignment is unfolding—quietly, rapidly, and with consequences far beyond the familiar debates of climate, trade, or competition policy. The world is entering a new cold war, not ideological but technological, defined by the contest for supremacy in energy systems, artificial intelligence, supply chains, and the industrial architecture of the mid-21st century. Its battlegrounds are no longer the arsenals and alliances of old geopolitics, but rather power grids, data centres, semiconductor fabs, battery plants, and vast interconnected digital infrastructures. Its outcome will determine the world’s economic hierarchy for decades to come.

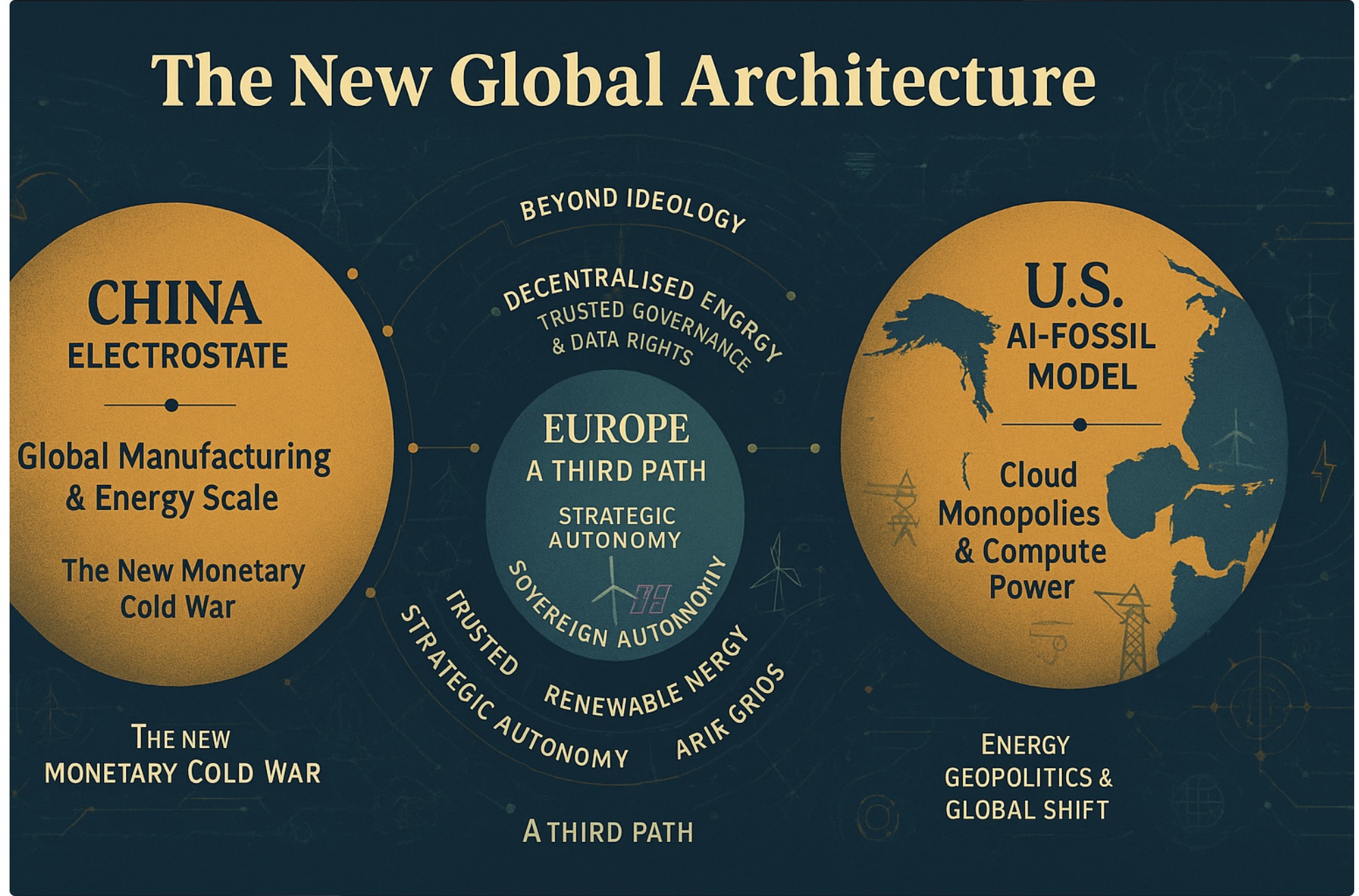

Amid this transformation, Europe finds itself at a strategic tipping point—at once exposed, constrained, and unexpectedly central. China has already crossed into a new industrial paradigm: a fully electrified, renewable-powered model delivering unprecedented speed, cost efficiency, and manufacturing scale. The United States, meanwhile, pursues an entirely different trajectory—an AI-led economy powered by hydrocarbons, cheap natural gas, and hyperscale cloud ecosystems. These two superpowers, China the electrostate and the U.S. the fossil-powered AI empire, are shaping the contours of global competition and carving out a bipolar technological order.

Europe stands in the middle of this G2 confrontation, yet without the energy foundation, digital sovereignty, or industrial cohesion needed to compete on equal terms. High energy prices, an aging grid, fragmented governance, and dependence on American cloud platforms and Chinese clean-tech supply chains threaten to erode Europe’s economic base. The continent that invented the modern industrial economy now risks becoming a technological consumer rather than a technological producer.

This report—the combined insights of six interconnected

articles—argues that Europe’s future prosperity, sovereignty, and

geopolitical relevance will be determined by one decisive factor:

whether it can decarbonise and electrify at a pace and scale

matching the new global reality.

Decarbonisation is no longer primarily an environmental commitment. It

has become Europe’s economic survival strategy.

1. China’s Electrostate Model: Industrial Power Through Electrification

China has executed an industrial transformation unmatched in historical speed. Having met its 2030 renewable-energy targets years ahead of schedule, Beijing now controls the world’s solar, wind, EV, and battery production. Clean energy contributes roughly 9% of China’s GDP and underpins a national strategy that fuses energy security, industrial expansion, technological dominance, and geopolitical leverage.

China’s electrostate model is built on five reinforcing pillars:

- Massive, cheap renewable electricity deployed faster than any country in history

- Electrified manufacturing, reducing energy costs across value chains

- Dominance in critical clean-tech supply chains, from polysilicon to lithium refining

- Integrated industrial policy, aligning finance, regulation, and local government incentives

- Export of turnkey energy–industrial ecosystems to the Global South

The result is a form of industrial power that enables China to scale robotics, automation, AI deployment, and advanced manufacturing at far lower marginal cost than its competitors. With cheap electricity, China’s factories can absorb rising global demand for semiconductors, EVs, clean-tech equipment, and AI hardware with unparalleled agility.

China is not simply decarbonising; it is using decarbonisation to capture the commanding heights of the 21st-century economy.

2. The U.S. Path: Fossil-Fuelled AI Acceleration and Digital Dominance

The United States is taking a fundamentally different path—one powered by abundant fossil energy and driven by private-sector innovation. Its AI boom, cloud infrastructure expansion, chip leadership, and hyperscale compute capacities rely overwhelmingly on natural gas–powered electricity.

The U.S. model rests on:

- Low-cost hydrocarbons, enabling aggressive data-centre expansion

- A private-sector-led AI ecosystem, with frontier models built by corporate actors

- Digital platform concentration, reinforcing market dominance

- A global cloud footprint that shapes international data governance

- Industrial policy (IRA, CHIPS Act) aimed at reshoring manufacturing and reducing China dependence

This model produces innovation speed and global influence—but also creates a structure Europe cannot replicate. Europe does not possess cheap hydrocarbons, a unified capital market, or digital giants capable of competing with U.S. hyperscalers. If Europe attempts to copy the American “AI-first, fossil-powered” trajectory, it will face:

- critically high electricity prices

- worsening energy dependence

- increasing emissions

- industrial flight

- digital subordination to U.S. cloud companies

- irreversible competitive decline

The message is stark: if Europe imitates the U.S. model, Europe loses.

3. Europe’s Dilemma: Competitor, Dependent, or Architect?

Europe is neither China nor the United States. It does not have China’s manufacturing scale or command economy. It does not have America’s low-cost fossil energy or hyperscale digital monopolies. But it does possess:

- institutional stability

- regulatory credibility

- leadership in sustainability

- advanced manufacturing expertise

- one of the world’s most skilled workforces

- a strong SME-driven industrial fabric (95% of EU firms, 30% of GDP)

- latent potential in decentralised energy

Europe’s problem is not capability—it is speed, coordination, and strategic clarity.

The risk is that Europe drifts into strategic dependency, relying on American AI models, Chinese industrial hardware, and imported fossil fuels to sustain its digital economy. High input costs would hollow out manufacturing, accelerating deindustrialisation and weakening Europe’s geopolitical voice.

But Europe also has a unique path—one that no other major power can pursue as effectively: a renewable, decentralised, digital-ethical model grounded in trust, rights, and resilience.

This is Europe’s competitive advantage—if it chooses to act.

4. The Energy–AI Nexus: Why Europe Cannot Lead in AI Without Leading in Electricity

AI is the most energy-hungry technology ever created. By 2030, European data-centre consumption will rival heavy industries such as chemicals and steel. The next wave of AI models will require enormous compute clusters, stable electricity supply, and high-quality grid infrastructure.

Europe’s energy system—fragmented, aging, underinvested—cannot support this future. Without:

- modernised cross-border grids

- mass renewable deployment

- sovereign compute clusters

- energy storage at scale

- digitally controlled distribution networks

Europe will be unable to sustain AI, automation, robotics, or

digitalisation.

There is no AI without energy.

There is no sovereignty without electricity.

5. Europe’s Secret Weapon: Decentralised Power Systems

Where China relies on centralisation and the U.S. relies on fossil energy, Europe has an underexploited structural advantage: distributed, community-based, SME-driven energy ecosystems.

Microgrids, rooftop solar, local energy markets, flexible loads, and regional storage networks can:

- reduce energy costs

- enhance resilience

- support SMEs and local industry

- reduce reliance on imports

- create exportable models for the Global South

Europe can lead the world in decentralised, democratic energy systems—if it invests now.

6. The Core Insight: Decarbonisation Is a Competitiveness Strategy

The common misconception is that decarbonisation is expensive, slow, or economically burdensome. In reality:

- renewable energy is the cheapest electricity in human history

- electrification can cut system-wide energy demand by 50–60%

- stable renewable-based electricity reduces industrial costs

- decentralisation reduces geopolitical vulnerability

- energy efficiency increases competitiveness

Countries that electrify fastest will:

- dominate global value chains

- set international standards

- attract investment

- secure technological sovereignty

- build resilient supply chains

- shape the emerging global economic order

Decarbonisation is no longer a moral or environmental goal.

It is Europe’s only viable route to long-term economic security.

7. A New Strategic Imperative for Europe

Europe must decide whether it becomes:

- A dependent technology consumer, shaped by American and Chinese decisions;

- A fragmented, declining industrial region, unable to compete on cost or scale; or

- A sovereign, competitive, electrified model, trusted globally and anchored in resilience, sustainability, and democratic governance.

The third path is Europe’s strength. But it requires unprecedented political will and a unifying industrial vision.

The next decade will decide whether Europe remains an architect of global rules—or becomes subject to them.

8. The Purpose of This Series

This six-article series explores the core strategic dimensions of Europe’s future:

- Energy Geopolitics & Global Power Shift

- AI, Smart Technologies, and the New Sovereignty Divide

- The Fourth Industrial Revolution & Decentralised Power

- The New Monetary Cold War & Digital Currency Systems

- Beyond Ideology: Structural Shifts Defining the New Order

- Europe’s Challenge: Competitiveness in a G2 World

Together, they form a blueprint for understanding the geopolitical, economic, and technological transformations reshaping the world—and what Europe must do to remain a global actor, not a spectator.

Final Message

The global race is underway.

Two giants have already chosen their models.

Europe must choose its own—fast.

Decarbonise at scale, modernise the grid, build sovereign digital capacity, and empower a decentralised industrial base—or risk irreversible decline.

Europe still has the assets to lead.

But only if it acts now.