Financing the Constraint — Inflation, Capital Structure, and Fiscal Risk in an Energy-Bound System

From Structural Inflation to Monetary Transmission

System Position

This article sits at the transmission layer between energy constraint, capital allocation, fiscal stress, and monetary stability.

It extends the logic developed in:

The transmission chain is:

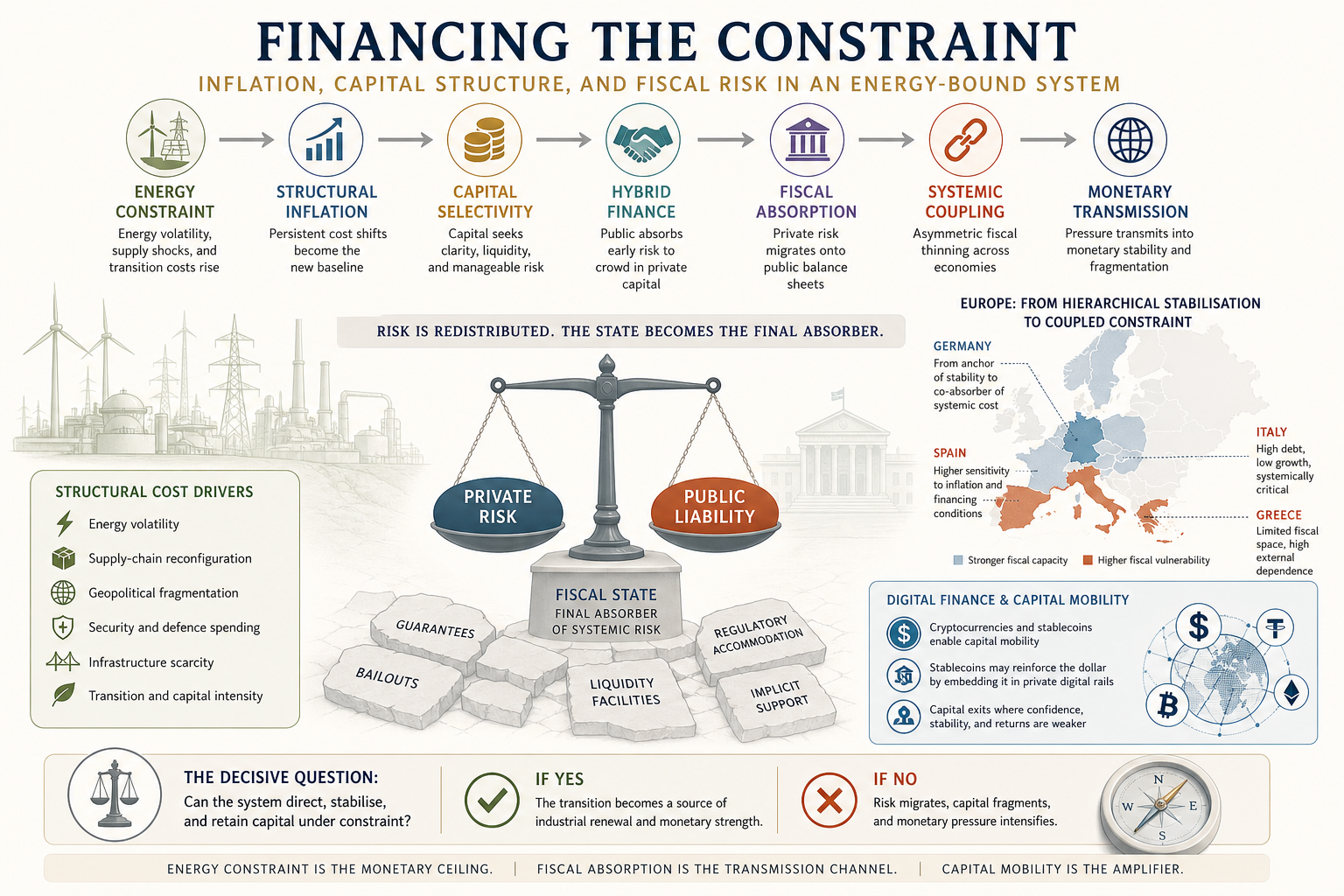

Energy constraint → structural inflation → capital selectivity → hybrid finance → fiscal absorption → systemic coupling → monetary transmission

Keynote

In an Energy-Bound System, inflation, capital allocation, fiscal stability, and monetary outcomes form a single transmission chain.

The current phase of the global economy is not defined by a temporary inflation shock. It is defined by a structural shift in cost, investment requirements, and risk distribution.

The central question is therefore not simply how inflation is reduced in the short term.

It is how structural inflation is transmitted through capital markets, fiscal systems, and monetary architectures.

Executive Summary

The current inflationary environment cannot be explained primarily as a failure of fiscal discipline.

Fiscal behaviour matters, but it is no longer the only, or even the dominant, source of pressure.

Inflation increasingly reflects structural cost shifts: energy volatility, supply-chain reconfiguration, security spending, infrastructure scarcity, and the capital intensity of the transition.

This changes the operating environment for states and markets.

As structural costs rise, capital becomes more selective. It favours systems where energy costs, regulatory frameworks, and returns are clearer. Where investment risk remains uncertain, hybrid public–private finance becomes necessary.

But hybrid finance does not eliminate risk. It redistributes it.

Under stress, private financial exposure migrates onto public balance sheets through guarantees, backstops, regulatory accommodation, and crisis support. The fiscal state becomes the final absorber of risk generated elsewhere in the system.

In Europe, this mechanism is especially dangerous because the euro area combines monetary integration with fragmented fiscal capacity, uneven energy systems, and divergent industrial structures.

The result is a shift from hierarchical stabilisation, where a strong core absorbs peripheral pressure, toward coupled constraint, where several large economies face pressure simultaneously.

This is the fiscal-monetary transmission of energy constraint.

I. Inflation as Structural Condition

Inflation is still often interpreted as cyclical, excessive, or policy-induced.

That interpretation is increasingly incomplete.

A growing share of inflationary pressure now emerges from structural sources:

energy volatility

supply-chain reconfiguration

geopolitical fragmentation

defence and security spending

infrastructure scarcity

transition-related capital intensity

These are not temporary disturbances.

They are system-level adjustments.

This distinction matters because policy designed for cyclical inflation does not necessarily resolve structural inflation. Raising interest rates may suppress demand, but it does not build grids, reduce energy dependency, accelerate electrification, or increase industrial resilience.

In an energy-bound system, inflation is not only a price signal.

It becomes a constraint on system capacity.

Higher structural costs reduce monetary flexibility, increase financing requirements, and compress fiscal space. The problem is therefore not simply that prices rise. It is that the cost base of the system shifts upward before the productive architecture has been rebuilt.

This is where inflation becomes strategic.

II. Capital Under Structural Pressure

As costs rise and investment needs expand, the role of capital changes.

The transition requires large-scale investment in:

energy infrastructure

grids and storage

electrified industry

AI and compute infrastructure

supply-chain resilience

defence and security capacity

At the same time, capital continues to operate according to its own logic.

It seeks liquidity, flexibility, visible returns, and manageable risk.

This creates a structural mismatch.

The system needs capital to move into long-duration assets whose returns are delayed, regulated, politically exposed, or dependent on infrastructure that does not yet fully exist.

Private capital does not necessarily withdraw under these conditions. It becomes more selective.

It moves toward systems where the relationship between cost, return, regulation, and currency stability is easier to price.

This is why energy systems, industrial policy, and monetary stability can no longer be analysed separately. Capital allocation responds to the credibility of the whole system.

III. Hybrid Finance and the Reallocation of Risk

Public–private finance is often discussed as a policy preference.

That framing is too narrow.

In an energy-bound system, hybrid finance emerges because the risk profile of the transition exceeds what private capital can absorb alone.

Frameworks associated with Ann Pettifor and wider Green New Deal finance arguments point toward an important structural reality: when the private sector cannot price or carry early-stage systemic risk, that risk must be redistributed.

Hybrid finance enables investment in:

energy transition

infrastructure

industrial transformation

strategic technologies

regional development platforms

This does not mean that the state replaces markets.

It means that public balance sheets, public banks, guarantees, and supranational institutions create the conditions under which private capital can participate.

The state absorbs part of the uncertainty so that private capital can enter later, once returns become more legible.

This is not exceptional. It is how major infrastructure systems have historically been built.

But it has consequences.

IV. Private Finance as Latent Public Liability

Hybrid finance is not neutral.

It transforms the balance sheet of the system.

Under stable conditions, public–private models appear efficient. Risk is distributed, capital flows, and projects are financed.

Under stress, the structure becomes clearer.

When financing conditions tighten, when infrastructure projects underperform, when refinancing costs rise, or when asset values fall, risk does not disappear.

It migrates.

Through guarantees, bailouts, liquidity facilities, regulatory flexibility, and implicit public support, private financial exposure becomes a latent public liability.

This is one of the central mechanisms of modern financial systems.

The fiscal state does not weaken only because it spends too much.

It weakens because it absorbs risk generated elsewhere in the system.

This is especially important in the energy transition. Many of the assets required are public in function but private or hybrid in financing structure. When they succeed, returns may be captured privately. When they fail, the system often requires public stabilisation.

This is not simply a moral criticism.

It is a structural fact.

V. Europe — From Hierarchical Stabilisation to Coupled Constraint

This mechanism operates globally, but Europe is particularly exposed because of the structure of the euro area.

The euro combines:

monetary integration

fragmented fiscal capacity

nationally managed energy systems

uneven industrial structures

different debt profiles

divergent exposure to external energy pricing

Under conditions of low inflation and abundant energy, this architecture was difficult but manageable.

Under structural inflation and energy constraint, it becomes more fragile.

The European system historically relied on a form of hierarchical stabilisation. Stronger economies, especially Germany, provided implicit credibility to the system. Peripheral stress could be contained through institutional intervention, fiscal adjustment, and monetary support.

But this structure is changing.

Germany remains a central stabilising node, but it is no longer insulated from the same pressures affecting the rest of Europe. Higher energy costs, industrial restructuring, defence commitments, demographic pressure, and transition investment needs are shifting Germany from a pure stabiliser into a co-absorber of systemic cost.

Italy represents a different category of risk. It is systemically critical, deeply integrated into the euro area, and constrained by high debt, low growth, and sensitivity to financing conditions.

Spain and Greece face different structural profiles, but the mechanism is similar: less fiscal space, higher sensitivity to external financing conditions, and greater exposure to the consequences of delayed investment.

The key point is not that all European economies face the same stress at the same time.

They do not.

The point is that they are exposed to the same transmission chain with different timing and intensity.

This produces asymmetric fiscal thinning.

Stronger states absorb pressure later.

Weaker states absorb pressure earlier.

But the underlying system constraint is shared.

VI. Austerity, Underinvestment, and Structural Weakening

When fiscal pressure intensifies, policy often shifts toward restraint.

This can stabilise public accounts in the short term, but it may weaken the system over the longer term.

A familiar cycle appears:

fiscal pressure increases

consolidation becomes politically necessary

investment is delayed or reduced

infrastructure gaps persist

growth weakens

fiscal capacity narrows further

In an energy-bound system, this cycle is especially damaging.

Energy infrastructure is not discretionary. It is the operating base for industrial competitiveness, compute capacity, capital formation, and monetary stability.

If fiscal restraint reduces investment in grids, storage, electrification, and industrial renewal, it may appear prudent in accounting terms while increasing the structural fragility of the system.

This is the austerity trap under energy constraint.

It protects the balance sheet while weakening the productive base that makes the balance sheet sustainable.

VII. Monetary Transmission and Fragmentation

The final stage of this process is monetary.

Monetary stability depends not only on central bank policy. It depends on fiscal credibility, growth capacity, productive depth, and system coherence.

When structural costs rise, investment requirements expand, and fiscal space narrows, monetary systems become more sensitive to divergence.

This is how the transmission works:

Inflation → capital structure → fiscal absorption → monetary pressure → fragmentation

Capital reallocates toward systems that appear more coherent, more liquid, more energy-secure, or more capable of absorbing risk.

Sovereign spreads become more sensitive.

Currencies become more exposed to structural credibility.

The monetary system does not break suddenly.

It is repriced gradually.

This is why energy constraint becomes a monetary ceiling.

VIII. Digital Finance, Stablecoins, and Capital Mobility

A further layer now enters the system: digital finance.

Cryptocurrencies, stablecoins, tokenised assets, and private digital financial rails are often discussed as technological innovations. They are also responses to structural instability.

Where inflation is high, banking systems are weak, currencies are unstable, or capital controls are restrictive, digital assets offer an alternative channel for storing and moving value.

This is already visible in parts of the Global South, where cryptocurrencies and stablecoins are used for remittances, savings, and protection against domestic monetary instability.

This does not mean that cryptocurrencies solve the monetary problem.

They may deepen it.

They create channels through which capital can move outside national monetary architectures, reducing the ability of weaker states to tax, regulate, and retain domestic savings.

Stablecoins are particularly important because they do not necessarily weaken the dollar.

They may reinforce it.

Dollar-linked stablecoins can extend dollar exposure into digital systems, embedding the dollar more deeply into private financial infrastructure even as confidence in traditional monetary governance becomes more contested.

This creates a paradox.

States expand their balance sheets to stabilise the system, while capital gains more tools to move outside state-controlled channels.

That interaction may define the next phase of monetary fragmentation.

IX. The Limits of Network-State Ideology

Alongside digital finance, a wider ideological current has emerged around the reconfiguration of sovereignty.

The “network state” and related visions imagine digitally coordinated communities, private financial rails, crypto-based governance, and non-territorial forms of political organisation.

These ideas should not be dismissed simply because they appear eccentric or speculative.

Their importance lies in their proximity to capital, platforms, and sections of political power.

But in an energy-bound system, their limits are clear.

Digital coordination can move capital.

It can organise communities.

It can create financial instruments.

It cannot replace the physical foundations of sovereignty.

Energy systems, industrial capacity, compute infrastructure, taxation, logistics, defence, and crisis absorption remain territorial and capital-intensive. They require states, public authority, regulatory capacity, and long-duration infrastructure coordination.

The network-state vision expresses the demand side of the system: mobility, autonomy, exit, and private coordination.

It does not solve the supply side: energy, infrastructure, industry, and systemic risk.

In this sense, it is not an alternative to the state.

It is a symptom of stress within the state-based monetary and fiscal order.

X. Strategic Conclusion

The current global economy is not simply experiencing inflation.

It is experiencing a restructuring of the relationship between cost, capital, fiscal capacity, and monetary power.

The central transmission chain is clear:

Energy constraint → structural inflation → capital selectivity → hybrid finance → fiscal absorption → systemic coupling → monetary transmission

Hybrid finance does not eliminate risk.

It reallocates it.

Private capital does not disappear.

It becomes more selective and more mobile.

The state does not merely spend.

It absorbs systemic risk.

Europe’s vulnerability lies in the fact that this absorption occurs inside a fragmented fiscal architecture, a shared monetary system, and an uneven energy base.

The Mediterranean question belongs inside this logic. Its strategic value depends on whether energy flows, infrastructure, and capital can be converted into system power rather than remaining dispersed across fragmented national and financial channels.

The decisive question is therefore not whether capital exists.

It does.

The question is whether the system can direct, stabilise, and retain capital under constraint.

Where it can, the transition becomes a source of industrial renewal and monetary strength.

Where it cannot, risk migrates, capital fragments, and the monetary ceiling tightens.